Download

1 / 17

180 likes | 373 Views

Accruals and 9130 Reporting . Quarterly Expenditures and Program Income must be reported to ETA on the accrual basis of accounting (WIA regulations 20 CFR 667.300). Overview. Cash v.s. Accrual Accounting. ETA-9130 Report Form. Common Problems to Avoid.

E N D

Accruals and 9130 Reporting Quarterly Expenditures and Program Income must be reported to ETA on the accrual basis of accounting (WIA regulations 20 CFR 667.300)

Overview Cash v.s. Accrual Accounting ETA-9130 Report Form Common Problems to Avoid

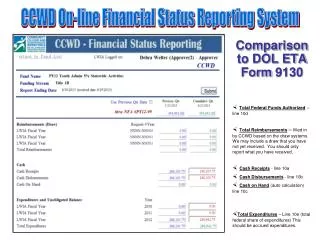

PAYMENT MANAGEMENT SYSTEM – DISBURSEMENT ACTION It’s a matter of timing! Accrued Expenditure Line 10e Cash Account Ledger Report Record Purchase Goods And Services Bank Account Income Rec’d Purchase Paid Bill Disbursement Difference between Accrual and Cash Accounting

Examples of Common Accruals • Wages, salary and fringe benefit costs for work performed or leave taken in a given period for which employees have not yet been paid. • Training – Participants attending classes – no invoice received from the training institution. • Purchases – Equipment ordered and delivered but not yet paid for • Sub-grant - Activity occurred with no invoice or report received.

REPORTS ARE DUE 45 DAYS FROM THE END OF THE QUARTER NOW … WHAT???

Review online tutorials and other resources on ETA-9130 reporting available at etareporting.workforce3one.org. Introduction to Financial Reporting Basic 9130 Reporting

Review key guidance and resource documents at http://doleta.gov/grants/financial_reporting.cfm. Forms and Instructions

Share information with others supporting the grant.

END Questions???