Download

1 / 7

100 likes | 275 Views

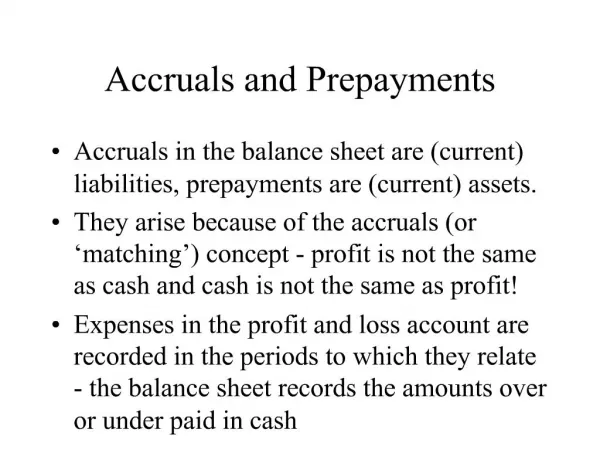

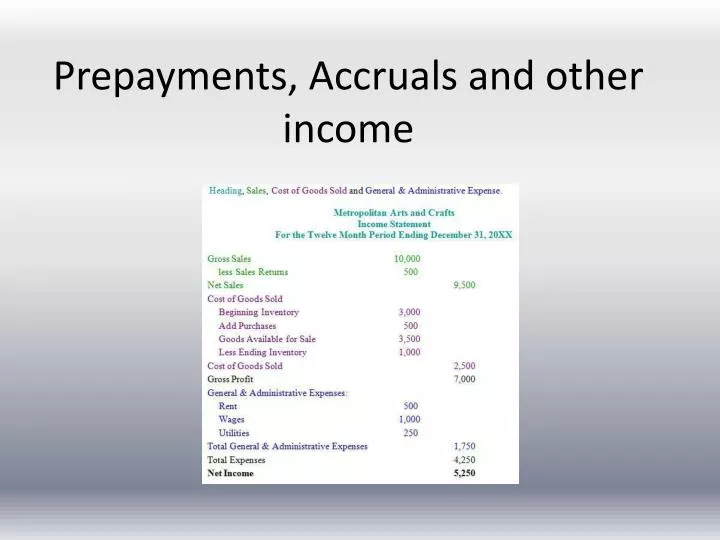

Prepayments, Accruals and other income. P repayments. Prepayments must be deducted from expenses in the income statement. This is because they should be in the income statement that’s produced for next year. For example rent paid in advance.

E N D

Prepayments • Prepayments must be deducted from expenses in the income statement. This is because they should be in the income statement that’s produced for next year. For example rent paid in advance. • Prepayments must be added to the current assets section of the balance sheet.

Example • Rent is £1200 at 6 March 2011. Four months have been paid in advance. • General expenses of £500 have been paid in advance. • Take off the prepaid amount off the original amount and add it into current assets.

Accruals • They are not paid till next year even though they have been used this year e.g electricity. • They must be added to expenses in the income statement, i.e they belong to this years accounts. • They must be added to the current liabilities section in the balance sheet.

Example • Rent unpaid at 18 February 2009 amounted to £700. • General expenses of £500 are unpaid. • Add on the accrued amount onto the original amount and add it into current liabilities.

Other income • This is money that is owed to the business and has been paid. • For example; rent receivable, bad debts recovered and commission receivable.

All 3 sections have to be included in the income statement and the balance sheet otherwise it will not balance at the end.