Download

1 / 15

150 likes | 344 Views

Chapter 8 The Gain From Portfolio Diversification. Level of Risk. Determine. Optimal Portfolio. Expected Return. Investment Weights. Affect the Portfolio’s Variance Minimize Portfolio’s Risk Determine the Investor’s Risk Exposure 1 Strategy of Weights Will Yield a Portfolio with No Risk.

E N D

Level of Risk Determine Optimal Portfolio Expected Return

Investment Weights • Affect the Portfolio’s Variance • Minimize Portfolio’s Risk • Determine the Investor’s Risk Exposure • 1 Strategy of Weights Will Yield a Portfolio with No Risk

Weights For The 2 Asset Portfolio WA + WB = 1 WB = 1 - WA WA + (1 - WA) = 1 or 100% only need to solve for one variable

Gains From Diversification • Lower Correlation • Smaller Portfolio Variance • Larger Gains From Diversification • For a Given Set of Weights

Minimize Portfolio’s Risk • Selecting Assets With Low Correlation • Balancing the Investment Weights • Degree of Correlation • Influences the portfolio’s level of risk • Lower the correlation, the larger the gain from diversification

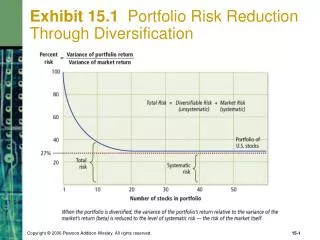

How Many Stocks Are Required For Adequate Diversification? • The More Stocks, the Better • Increasing Transaction Costs • 10-15 Stocks Sufficient • 90% of Maximum Benefit with 12-18 • Most Benefits Achieved with 10 • Diminishing Benefits with Additional Stocks

“A Little Diversification Goes A Long Way” As the Number of Assets Increases the Incremental Contribution to Variance Reduction Becomes Smaller and Smaller

Mutual Funds • Diminishing Benefits of More Stocks are Still Positive • There is some gain • Low Cost of Data • Large Funds Have to Invest in Many Stocks • Avoid buying and selling affects • Regulation M • Own 5% of any company’s stock

MVP • Minimum Variance Portfolio • Portfolio With the Smallest Variance From the Mean-Variance Frontier • Mean-Variance Frontier • Efficient frontier • Dominate portfolio • Inefficient frontier

What Is The Implication Of Diversification For Portfolio Management? • Not All Diversification Strategies are Desirable • Some Strategies are Inefficient • No Investor Would Select Portfolios From the Segment Below Point MVP see next slide

E(R) • Efficient Frontier MVP Inefficient Frontier Standard Deviation

Two Assets With Different Correlations • The Higher the Correlation, the Smaller the Gain From Diversification • As Correlation Declines, Risk Reduction Increases • Implies larger risk reduction because of diversification

Complicated Portfolio Choices • More Than Two Assets to Choose From • Assets do not Have the Same Mean or Variance • Nonzero correlations prevail • Must Find the Mean-Variance Frontier • Identify the Efficient and Inefficient Sets

Unrelated Industries • Significant Risk Reduction • Achieved by diversifying across different industries • Stocks From Same Industry • Highly positively correlated • Stocks From Different Industries • Negative correlation