Download

1 / 22

220 likes | 234 Views

Learn about review services for unaudited financial statements, distinguishing reviews from audits, procedures involved in review engagements, and reporting standards. Gain insight into the limited objective of reviews, the scope, and key elements of a review engagement report.

E N D

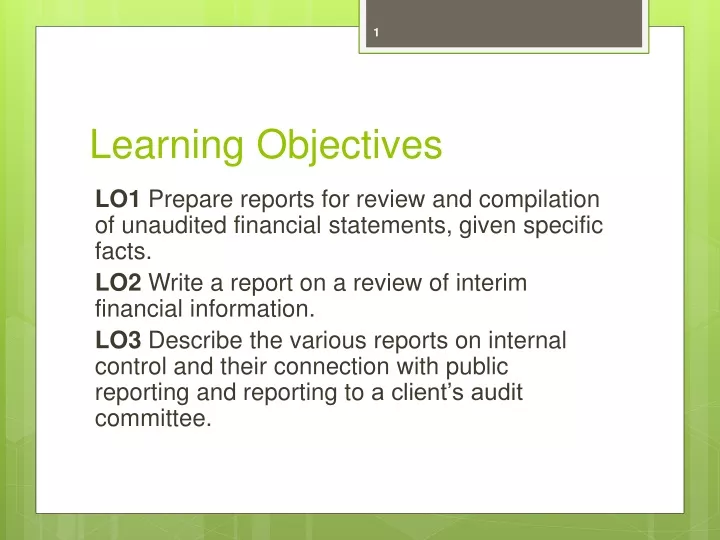

Learning Objectives LO1 Prepare reports for review and compilation of unaudited financial statements, given specific facts. LO2 Write a report on a review of interim financial information. LO3 Describe the various reports on internal control and their connection with public reporting and reporting to a client’s audit committee.

Unaudited Financial Statements Small business wants some level of assurance but without full GAAS and high cost. • “Big GAAS-Little GAAS” • Small clients want to receive some level of assurance even though a GAAS audit is not performed. • Review engagements. • Compilation engagements. LO1

Review Services Review services apply specifically to accountant’s work on unaudited financial statements. • Reviews are distinguishable from audits in that the scope of a review is less than that of an audit and therefore the level of assurance provided is lower. LO1

Review Services A review consists primarily of: • enquiry, analytical procedures, and discussion, • related to information supplied by the enterprise, and • with the limited objective of assessing whether the information being reported on is plausible. • “Plausible” is used in the sense of appearing to be worthy of belief. LO1

Review Engagement Standards General standard: • The review should be performed and the review engagement report prepared by a person or persons having adequate technical training and proficiency in conducting reviews, with due care and with an objective state of mind. LO1

Review Engagement Standards Review standards • The work should be adequately planned and properly executed. If assistants are employed, they should be properly supervised. • The public accountant should possess or acquire sufficient knowledge of the business carried on by the enterprise so that intelligent enquiry and assessment of information obtained can be made. LO1

Review Engagement Standards • The public accountant should perform a review with the limited objective of assessing whether the information being reported on is plausible in the circumstances within the framework of appropriate criteria. Such a review should consist of the following: • enquiry, analytical procedures, and discussion; and • additional or more extensive procedures when the public accountant's knowledge of the business carried on by the enterprise and the results of the enquiry, and analytical procedures and discussion cause him or her to doubt the plausibility of such information. LO1

Review Engagement Reporting Standards • The review engagement report should indicate the scope of the review. The nature of the review engagement should be made evident and be clearly distinguished from an audit. LO1

Review Engagement Reporting Standards • The report should indicate, based on the review: • whether anything has come to the public accountant's attention that causes him or her to believe that the information being reported on is not, in all material respects, in accordance with appropriate criteria; or • that no assurance can be provided. The report should provide an explanation of the nature of any reservations contained therein and, if readily determinable, their effect. LO1

Review Engagements: Procedures Review work is primarily consisting of enquiry and analytical procedures. • Read financial statements for indications they are in accordance with GAAP. • Obtain reports from other accountants who audit or review significant components. • Enquire of officers and directors regarding: • conformity to GAAP, consistency of accounting principles, and changes in client business. LO1

Review Engagements: Procedures Review work is primarily consisting of enquiry and analytical procedures: • Perform other procedures, prepare written papers, and obtain management representation letter. Firms may do additional procedures, although there are no formal requirements to do so. LO1

Report: Review Review does not provide a basis for expressing an opinion on the financial statements. • Each page of the financial statements should be conspicuously marked “unaudited.” • It should provide negative assurance, and no expression of an opinion is made. LO1

Report: Review Review report includes the following statements: • Scope of the review • Review consists primarily of enquiries and analytical procedures applied to financial data. • Review does not constitute an audit. • Accountant is not aware of any material modifications that should be made or disclosure of departures from GAAP (negative assurance). LO1

Review Engagement Report REVIEW ENGAGEMENT REPORT To (person engaging the public accountant) I have reviewed the balance sheet of Client Limited as at ......, 20... and the statements of income, retained earnings, and changes in financial position for the year then ended. My review was made in accordance with generally accepted standards for review engagements and accordingly consisted primarily of enquiry, analytical procedures and discussion related to information supplied to me by the company. LO1

Review Engagement Report A review does not constitute an audit and consequently I do not express an audit opinion on these financial statements. Based on my review, nothing has come to my attention that causes me to believe that these financial statements are not, in all material respects, in accordance with Canadian generally accepted accounting principles. City (signed) ................. Date CHARTERED ACCOUNTANT LO1

Compilation Services A compilation engagement is one in which a public accountant receives information from a client and arranges it into the form of a financial statement. • The public accountant is concerned that the assembly of information is arithmetically correct; however, the public accountant does not attempt to verify the accuracy or completeness of the information provided. LO1

Compilation Services Unlike an audit or a review engagement, no expression of assurance is contemplated in a compilation engagement. Compilation is a synonym for the older term “write-up” work. LO1

Compilation Services No assurance credibility is provided • This limits the public accountant for action to be taken. • Accountant has a responsibility not to be associated with misleading statements. • May withdraw from the engagement. • Each page of the statement should be marked “Unaudited – See Notice to Reader.” LO1

Notice to Reader I have compiled the balance sheet of Client Limited as at December 31, 20X1, and the statements of income, retained earnings, and cash flows for the (period) then ended from information provided by management (the proprietor). I have not audited, reviewed, or otherwise attempted to verify the accuracy or completeness of such information. Readers are cautioned that these statements may not be appropriate for their purposes. I am not independent with respect to Client Limited. City (printed or signed)……………… Date CHARTERED ACCOUNTANT LO1

Other Review and Compilation Topics Prescribed forms • Industry trade associations, banks, government agencies, and regulatory agencies often use prescribed forms (standard reprinted documents) to specify the content and measurement of accounting information required for special purposes. • Such forms may not request disclosure required by GAAP or may specify measurements that do not conform to GAAP. • The notice to reader control contains the caution that the financial statements may not be appropriate for the purposes of the reader. LO1

Other Review and Compilation Topics Personal Financial Plans: • Personal financial planning has become a big source of business for PA firms. • Ordinarily, an accountant associated with such statements would need to give the standard compilation report (disclaimer). LO1

Other Review and Compilation Topics A note on GAAP departures and review engagement reports: • An accountant’s report of known GAAP departures must be treated carefully in review reports. • As in audit reports, the accountant can and should add an explanatory paragraph pointing out known departures from GAAP, including omitted disclosures. LO1