Download

1 / 5

50 likes | 207 Views

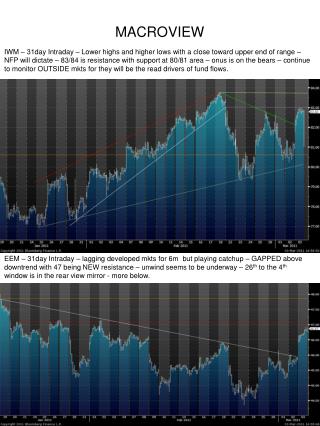

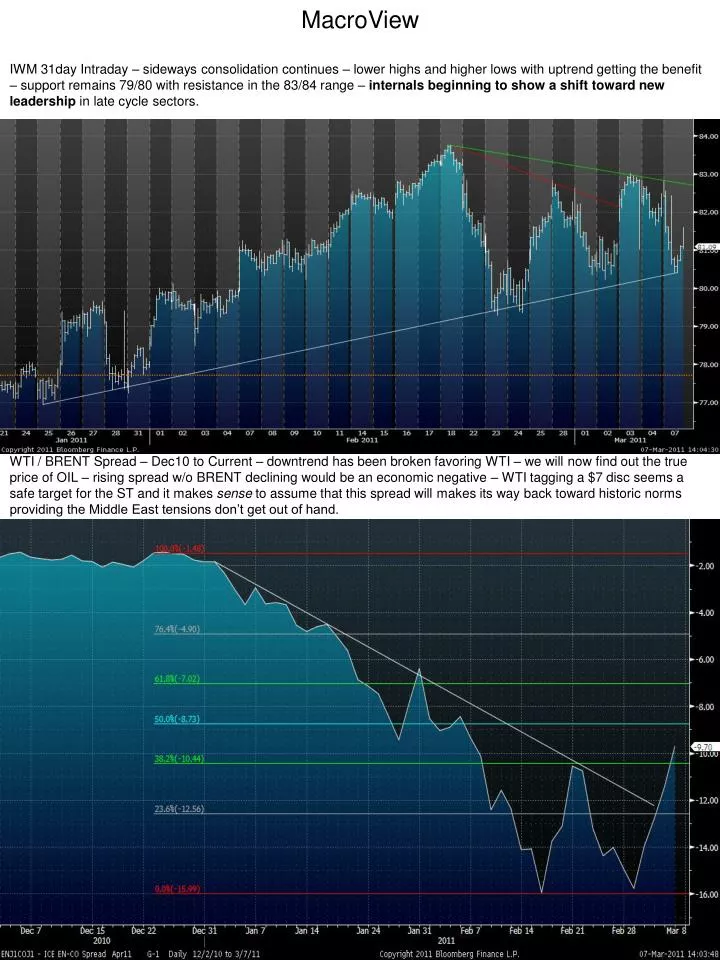

MacroView. IWM 31day Intraday – sideways consolidation continues – lower highs and higher lows with uptrend getting the benefit – support remains 79/80 with resistance in the 83/84 range – internals beginning to show a shift toward new leadership in late cycle sectors.

E N D

MacroView IWM 31day Intraday – sideways consolidation continues – lower highs and higher lows with uptrend getting the benefit – support remains 79/80 with resistance in the 83/84 range – internals beginning to show a shift toward new leadership in late cycle sectors. WTI / BRENT Spread – Dec10 to Current – downtrend has been broken favoring WTI – we will now find out the true price of OIL – rising spread w/o BRENT declining would be an economic negative – WTI tagging a $7 disc seems a safe target for the ST and it makes sense to assume that this spread will makes its way back toward historic norms providing the Middle East tensions don’t get out of hand.

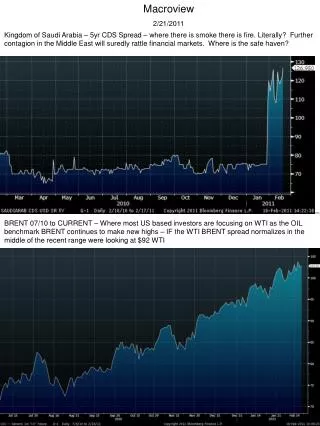

DXY – 06 to Current – weekly view shows the deterioration in the value of USD – sitting ON PRIMARY support with SECONDARY support at 75 followed by 72 – further breakdown will possibly have an impact on UST and further impact on CRB – MKTS are questioning the FEDs idea of monetary policy. TYX – US 30yr YLD – 06 to Current – notice recent USD dn US YLD up beginning at the start of 2011 – simultaneous breakdown in DXY and breakout in YLD will be “end game” mkt action.

EARLY CYCLE SECTORS – 07/10 To Current – YTD unwind of EARLY cycle leadership signals upcoming economic weakness should this rotation continue – monitor key support levels and individual stock relative strengths. XLK XLF XLY

Late Cycle Sectors – 07/10 to Current - rotation from EARLY to LATE clearly evident – whether this is quarter end positioning, rotations ahead of the ending of QE2, or upcoming economic weakness – RELATIVE valuations possibly beginning to favor the laggards. XLU XLV XLP

CRB vs SPX 07/10 to Current – most likely some backing and filling to alleviated overbought condition – bull mkt remains intact but expect unwind ahead of QUARTER END. MOO vs SPX 07/10 to Current – uptrend remains intact – recent LOWER HIGH is a possible YELLOW FLAG – elevated physical AG will most likely encounter profit taking as new crop takes hold.