Download

1 / 9

90 likes | 283 Views

Macroview. German Dax – 31day intraday - ST uptrend has been broken. Closing in on 15 days lows. Possibly strong EUR about to impact exports? Collapsing PIIGS about to find themselves on Germany’s balance sheet? Leader of EUR possibly rolling over.

E N D

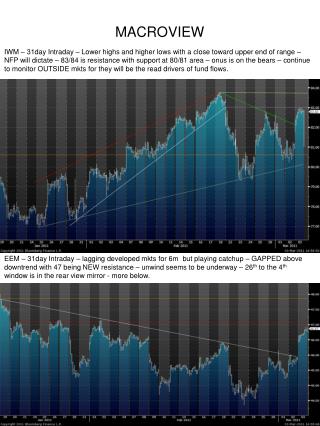

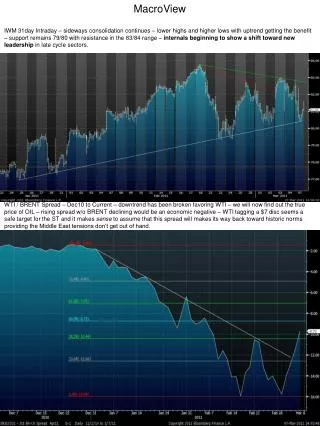

German Dax – 31day intraday - ST uptrend has been broken. Closing in on 15 days lows. Possibly strong EUR about to impact exports? Collapsing PIIGS about to find themselves on Germany’s balance sheet? Leader of EUR possibly rolling over. IWM – 08/10 to Current – uptrend remains intact but QE2 uptrend could be in jeopardy. Today’s lows will be PRIMARY support with 77 followed by 75 which would be NEW Lows for the year.

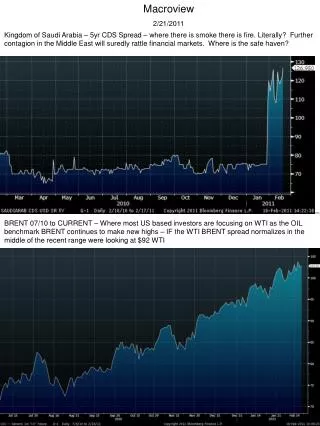

WTI BRENT Spread – normal bounce completed. Downtrend in favor of BRENT continues. This blowout has little or no connection with OIL flow and ALL to do with geopolitical events. WTI – Dec10 to Current – $88 to 100 in 4 days. Further rise will jeopardize already fragile recovery. No denying inflation now – margins will be squeezed as will the consumer.

GOLD vs OIL – 1983 to Current – LT downtrend remains intact. GOLD for preservation and OIL to keep the machines rolling. Barring financial wipeout (GOLD price explosion), we expect this to trend lower favoring OIL over months and quarters. GOLD vs AG – YOY – 26th to the 4th marked yet another turning point for a rotation, this time in favor of GOLD over AG. Calendar continues to dominate. Continue to own each of the CRB groups and use these rotations to generate alpha. When OIL rips AG is viewed as cheaper and GOLD is clearly being viewed as a currency KNOWING that any consumer based inflation will be met with monetary ease. $100 today might not buy $100 worth of goods (today’s prices) tomorrow. Markets are clearly trading CRB for CRB while depleting FX reserves. Can’t prove it, but market actions sure seems to be playing out that way.

MOO vs SPY – YOY – nearing “buy” zone on a RELATIVE basis. Wednesday action in MOO (absolute) was most likely a ST if not LT bottom. NEEDS vs WANTs will remain FRONT AND CENTER going forward. Softs might have a correction, but MOO names are in the midst of a secular bull market. GOVTs will hopefully not allow food shortages to continue; the need for fertilizer and other supplies will only increase. MOO vs EWZ (Brazil ETF) – YOY – nearing ST “buy” zone on a relative basis. Same story as above – call it double confirmation on a relative basis (EWZ is 10% Petrobras so clearly not the best comparison).

MOO vs XLE – 2004 to Current – Commodities remain in a SECULAR bull. Recent ME uprising has allowed for a RELATIVE correction in values. Uptrend should remain intact barring a further hoarding mentality taking place in Energy. FOOD remains the basic global need. MOO vs XRT – 2003 to Current – excluding the ethanol fueled boom in MOO leading up to the ‘08 collapse, the trend remains up. Expect consumer inflation to begin to weigh on the retail names going forward. If not food then energy or both – retail could possibly have peaked – we’ve most likely reached a “tipping point” of sorts.

10/30 Spread – YOY – after taking out 20yr highs above 100bps in 4Q10, the spread has corrected but remains ABOVE historical highs. Further widening will most likely be FX and INFLATION related, neither of which bode well for the ABSOLUTE levels of US DEBT or the risk free rate to equity yield comparisons. New Financial World Order coming our way? 2/10 SPREAD – YOY – as the 10/30 widens the 2/10 narrows. Break of 260bs will most likely signal a slowing economy and consumer deflation fears. This will most likely be met by stimulus, which is why the 2/10 and 10/30 will possibly move in opposite directions for a bit.

US 10YR YLD – YOY – 3.75% to 4.25% remains SECULAR RESISTANCE. Rally in UST seems rational seeing the recent geopolitical tensions. That rationality, however, has been lost on the USD (read no rally). At this point bonds are a gauge of stress rather then something to bet on. If rates go lower there are better ways to capitalize; if rates go higher…well, that’s end game stuff. Soaring CRB, worsening demographics trends in western world, and a 3.6% absolute yield will NOT produce REAL returns in this environment. US 30YR YLD – YOY – 4.5% is SECULAR resistance. While we are monitoring ABSOLUTE levels, RELATIVE values are becoming more interesting – BUNDS vs UST remain in a trading range – For the time being….thats a good thing.

OIL vs FOOD (Shares) – 1989 to Current – like OIL/GOLD (Pg 4 Chart 1) OIL IS the global need. Energy security is the primary goal of GOVTs. Markets look poised to possibly have another upward shift toward this space. GEOPOLITICAL will drive spreads. OIL vs FOOD (Physical) – 1991 to Current – like the chart above we have the same story. OIL is in a BULL market vs ALL other Commodities. Are we entering another uptick in energy dominance of CRB bull market?