Download

1 / 5

50 likes | 208 Views

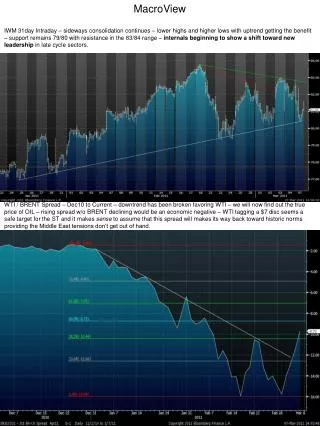

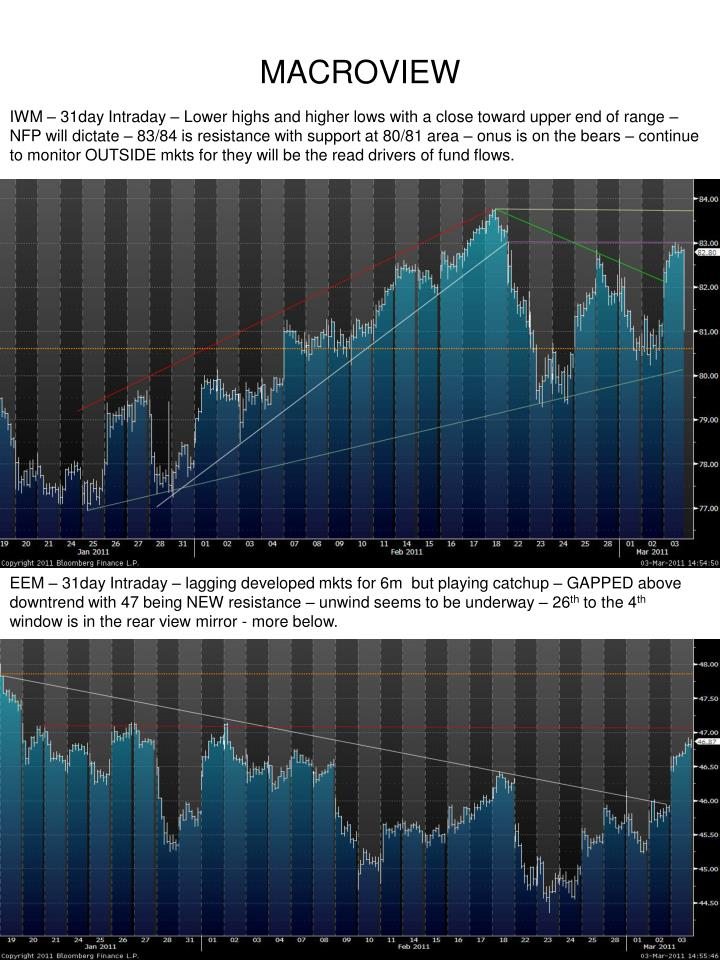

MACROVIEW. IWM – 31day Intraday – Lower highs and higher lows with a close toward upper end of range – NFP will dictate – 83/84 is resistance with support at 80/81 area – onus is on the bears – continue to monitor OUTSIDE mkts for they will be the read drivers of fund flows.

E N D

MACROVIEW IWM – 31day Intraday – Lower highs and higher lows with a close toward upper end of range – NFP will dictate – 83/84 is resistance with support at 80/81 area – onus is on the bears – continue to monitor OUTSIDE mkts for they will be the read drivers of fund flows. EEM – 31day Intraday – lagging developed mkts for 6m but playing catchup – GAPPED above downtrend with 47 being NEW resistance – unwind seems to be underway – 26th to the 4th window is in the rear view mirror - more below.

EEM vs IWM – 2003 to Current – secondary support was tested and were getting a technical bounce – most likely more backing and filling with the secular view favoring Emerging – inflationary headwinds remain but recent underperformance clearly discounted recent events. EWZ vs IWM – spread seems to have found support in the “buy zone” - EWZ weightings in PBR could be responsible for overshoot to the downside (massive underperformer) – EWZ on absolute basis closed slightly ABOVE 75 resistance.

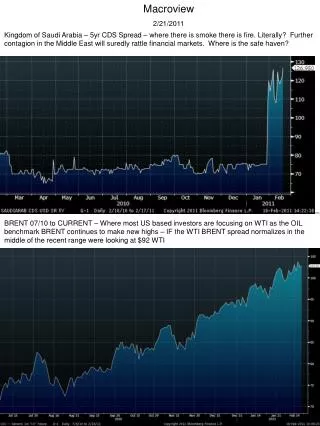

EWZ vs EEM – 2003 to Current – uptrend favoring EWZ continues with the spread finding support on the secular uptrend in place since 2003 – providing these lows HOLD it would seem that the secular bull mkt for Brazil will continue – secular meaning LONG TERM – cyclical headwinds remain. TYX – US 30yr YLD - 1993 to Current – SECULAR downtrend in bond yld rally being tested and most likely will break to the upside – QE2 stimulus will be removed by July and who will buy (see Pimco Gross notes) – monitor 4.75%-5.00% and the action of the USD – more below.

EURO – KING OF G3? EUR vs JPY – 2005 to Current – downtrend has been broken and possibly bottoming in favor of EUR – Weakness in JPY vs remainder of G3 COULD POSSIBLY CAUSE NIKKEI TO BEGIN TO OUTPERFORM other equity mkts. EUR vs CHF – 2007 to Current Downtrend remains intact but recent acceleration during 2010 could have possibly been signs of exhaustion – SNB recently announced a 21B loss on intervention – break ABOVE ST downtrend could bring additional EUR support. EUR vs USD – G3 remains under REAL pressure as a store of value - break ABOVE 1.40eur would be yet another sign of sentiment shift AWAY from USD as a reserve currency

GOLD priced in EUR – 2005 to Current – testing 1040-1075 ALL time highs – Strengthening EUR clearly a headwind – GOLD mkt seems to be watching FX, OIL, and AG as it fights for investor dollars – Bull mkt remains intact and rotation within the inflationary view will continue. GOLD in CHF – 2005 to Current – trend remains up with recent gains being consolidated in a wide band – lower highs and higher lows clearly evident – GOLDs volatility will only increase in the months and quarters ahead