Download

1 / 56

560 likes | 591 Views

Learn about short selling, credit default swap, risks, intermediary roles, and reasons for short selling in financial markets. Discover key events and regulations in this area.

E N D

Short selling and credit default swap Financial Market Law and Regulation Paola Lucantoni

Short selling • borrow (or not) a stock, • sell the stock • buythe stock back to returnit to the lender (ifborrowed; or to settle the position when the short seller sellswithoutborrowing).

aim • Short sellers makemoney by bettingthat the stock they sell willdrop in price. • Ifthe stock drops, the short seller buysit back at a lowerprice and returnsit to the lender.

Example • an investorthinksXYZ isovervaluedat $25 and isgoing to drop in price, • The investormayborrow the stock and sell it for $25. • Ifthe stock goes down to $20, the investor, afterbuyingit back and returningit, wouldmake $5 per share. • However, if the stock goes up to $30, the investorwouldlose $5 per share.

Risks are amplified • Long position: • whenyoubuy a stock (or long position: the buying of a security suchas a stock, commodity or currency, with the expectationthat the assetwill rise in value) you can loseonly the moneythatyou'veinvested. • So, ifyouboughtoneXYZ share at $25, the maximum youcouldloseis $25 because the stock cannotdrop to lessthan $0. • Short position: • whenyou short sell, you can theoreticallylose an infinite amount of money, because a stock'sprice can keeprisingforever. • So, for example, ifyouhad a short position position in XYZ (or short soldit) and XYZ ended up risingpast $60 beforeyouexitedyour position, youwouldlose $35 per share ($60-$25) - even more than the stock'soriginalprice

Intermediary • whenthe investorshort sellsa stock, a broker willlendit to the investor. • The stock will come from the brokerage'sowninventory, from anotherone of the firm'scustomers, or from another brokerage firm. • The shares are sold and the proceeds are credited to the investor’saccount. • Sooneror later, the investormust "close" the short by buying back the samenumber of shares and returningthem to the broker. • Ifthe pricedrops, the investorcan buy back the stock at the lowerprice and make a profit on the difference. • If the price of the stock rises, the investorhaveto buyit back at the higherprice, and losemoney.

Why short selling? • Speculate • watchingfor fluctuations in the market in order to quicklymake a big profit of a high-riskinvestment. • a high lossifthey use the wrongstrategiesat the wrong time, • butthey can alsosee high rewards. • Probablythe mostfamousexample of thiswaswhenSoros"broke the Bank of England" in 1992. He risked $10 billionthat the Britishpoundwouldfall and he was right. The following night, Soros made $1 billion from the trade. His profit eventuallyreachedalmost $2 billion. • Hedge • veryfew sophisticated moneymanagers short as an activeinvestingstrategy (unlikeSoros).

Working in progress • 14.06.2010 – Commissionserviceslaunch public consultation on short selling • 15.09.2010 – Commissionadoptsproposal for a Regulation on short selling and certainaspects of Credit Default Swaps • 24.11.2011 – Request for ESMA technicaladvice on possibledelegatedactsconcerning the Regulation on short selling and certainaspects of Credit Default Swaps • 24.03.2012 – Regulation (EU) No 236/2012 of the EuropeanParliament and the Council of 14 March 2012 on short selling and certainaspects of Credit Default Swaps (OJ L 86/1) • 29.06.2012 – Commissionadoptstechnicalstandards on short selling • 05.07.2012 – Commissionadoptsdelegatedact and regulatorytechnicalstandards on short selling • 13.12.2013 – Commissionadopts the Report on the evaluation of the Regulation (EU) No 236/2012 on short selling and certainaspects of credit default swaps

14.06.2010 – Commissionserviceslaunch public consultation on short selling • The Commissionserviceshavelaunched a public consultation on short selling. Itspurposeis to consult market participants, governments, regulators and otherstakeholders on possibleprovisions to be considered in a forthcomingCommissionproposal for stand alone legislationdealing with potentialrisksarising from short selling.

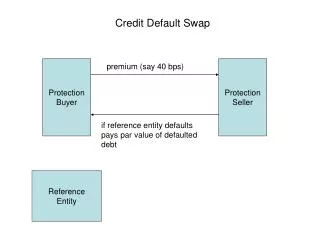

Definition of short selling of financialinstruments: • a personsells a security (typically a share) he doesnotown with the intention of buying back an identical security at a laterpoint in time, is an established and common practice in mostfinancialmarkets. • 1."Covered" short sellingiswhere the seller hasborrowed the securities, or made arrangements to ensurethey can be borrowed, before the short sale. • 2."Naked" or "uncovered" short sellingiswhere the seller hasnotborrowed the securitiesat the time of the short sale, or ensuredthey can be borrowed. • A Credit Default Swap (CDS) is a derivative whichissometimesregardedas a form of insuranceagainst the risk of credit default of a corporate or government (or sovereign) bond. In return for an annual premium, the buyer of a CDS isprotectedagainst the risk of default of the referenceentity (stated in the contract) by the seller. If the referenceentitydefaults, the protection seller compensates the buyer for the cost of default. • In addition to short selling on cash markets, a net short position can also be achieved by the use of derivatives, including Credit Default Swaps (CDS). For example, if an investorbuys a CDS withoutbeingexposed to the credit risk of the underlying bond issuer (a so-called "naked CDS"), he isexpecting, and potentiallygaining from, rising credit risk. Thisisequivalent to short selling the underlying bond.

Risks • itcan be used in an abusive fashion to drive down the price of financialinstruments • It can contribute to disorderlymarkets and, especially in extreme market conditions, can amplifypricefalls and have an adverseeffect on financialstability. • Itcan alsoresult in information asymmetries. In the case of uncovered short sales theremay be an increasedrisk of settlementfailures and pricevolatility.

Role in fm • Moststudies conclude that short sellingcontributes to the efficiency of markets. Itincreases market liquidity (as the short seller sellssecurities and thenlaterpurchases the identicalsecurities to cover the short sale). • Also, by allowinginvestors to actwhentheybelieve a security isovervalueditleads to more efficientpricing of securities, helps to mitigate pricebubbles and can actas an earlyindicator of underlyingproblemsrelating to an issuer. • Itisalso an importanttoolthatisused for hedging and otherrisk management activities and market making.

Fragmentedapproachwith short sellingduringfinancialcrisis • During the financialcrisis and more recently in the context of market volatility in Euro denominatedsovereign bonds, MemberStateshavereacteddifferently to short sellingissues, with a variety of measuresbeing put in placeusingdifferingpowers. • A fragmentedapproach can create additionalcosts and difficulties, lead to regulatoryarbitrage and limit the effectiveness of measuresimposed.

April 2009 • In April 2009 the Commissionaskedquestions in itsreview of the Market Abuse Directive about the possibility of a new European short selling regime. The responsesgave some support for a new regime. Manyrespondentsarguedhoweverthatanyproposalsshouldnot be in the Market Abuse Directive but in separate stand alone legislation. Thiswas on the basisthatitwasgenerallyconsideredthatmost short sellingisnot market abuse and raisesdifferentissues and risks.

2010 • In March 2010 the Committee of European Securities Regulators (CESR) published a report recommending a Pan-European model for the disclosure of short positions in EU shares. • In the CommissionCommunication of 2 June 2010 on "Regulating Financial Services for SustainableGrowth" the Commissionindicatedthatitwould propose appropriate measuresrelating to short selling and credit default swaps (CDS). • The Communicationalsohighlightedotherinitiatives, suchas new legislation on market infrastructure, the review of the Markets in Financial Instruments Directive and the review of the Market Abuse Directive, whichwillalsoaffect the regulatoryframeworkapplicable to derivatives and credit default swaps.

The Commissionbelievesthatworkingtowards a more harmonised regime for short sellingissueswillincrease the resilience and stability of financialmarkets in the European Union. • The purpose of this public documentwasto consult market participants, regulators and otherstakeholders on possibleprovisions to be consideredas part of the finalisation of the forthcomingproposal for stand alone legislationdealing with potentialrisksarising from short selling.

Application • The approachwouldapply to allpersonswhoengage in short sellingwhetherregulated or unregulated and acrossall market sectors. • The requirementswill in mostcasesapply to the personwhoentersinto the short sale or has a net short position ratherthan an intermediaryexecuting a transaction for thatperson.

Aims • The policy options can be groupedintothreetypes: • Rules to increasetransparencyrelated to short sales. • Rules to reduce risks of uncovered short selling. • Emergency powers for CompetentAuthorities to impose temporary short sellingrestrictions (subject to coordination by ESMA).

Intention • The intentionisthat the new measures on short sellingshould: • harmoniserulesacross the EU relating to short selling; • harmonisetoolsthatMemberStatesmay use in an emergency situation; • facilitate co-ordinationbetweenMemberStates and by ESMA in emergencysituations.

high leveloptions and questionsrelating to the scope of the proposal1/3 • The consultationdocument sets out twodifferentoptions for greatertransparency of short positions held by investors. • The first option would be to apply the transparency regime to alltypes of financialinstrumentsthat are admitted to trading on a trading venue in the EU. • The second option would be to apply the regime only to EU shares and to EU sovereign bonds. • Bothoptionswould include notonly short positions obtained by short selling the financialinstrumentitselfbutalso positions obtainedthrough the use of derivativesrelating to the financialinstrument.

high leveloptions and questionsrelating to the scope of the proposal2/3 • The policy optionsrelating to transparency are largelybased on the twotier model for EU shares recommended by CESR (the Committee of European Securities Regulators) in its report in March 2010. • The CESR model providesthat • ata lowerthresholdnotification of a short position should be made only to the regulator • and at a higherthreshold short positions should be disclosed to the market. Notification to regulatorswouldenablethem to monitor and, ifnecessary, investigate short sellingthatmay pose systemicrisks or be abusive. Publicationof information to the market wouldprovideuseful information to other market users.

high leveloptions and questionsrelating to the scope of the proposal3/3 • policy options to restrict "naked" or uncovered short selling • The first option would be to placeconditions on uncovered short selling so thatat the time of the sale the seller must eitherhaveborrowed the share, haveenteredinto an agreement to borrow the share or haveevidence of otherarrangementswhichensurethatitwill be able to borrow the shares at the time of settlement • The second option would be to require trading venues to have in placemeasures for the buying in of shares in certainsituationsif a short sale results in a settlementfailure.

emergencypowersfor competentauthorities • The options in the consultationdocumentwouldprovide for competentauthorities to be givenpowers to impose temporaryrestrictions on short selling and CDS transactions in an emergency. • The optionsattempt to harmonise the conditions under whichemergencyactionmay be taken, the procedures for takingaction and the scope of powersthemselves (whilestillallowingflexibility in emergencysituations). • the new European Securities Market Authority (ESMA) couldperform a keycoordination and facilitationrole.

"nakedCDS” 1/2 • A "naked CDS" refers to the situation where the CDS isused by the buyer not to hedge a riskbut to take a position (take risk). • The seller of the CDS would gain if the credit riskdidnotmaterialise; whereas the buyer of the CDS would gain if the price of the CDS subsequentlyincreases due to a perception by the market of an increasedrisk of default of the issuer.

"naked CDS” 1/2 • Greater transparency so thatpersons with significant net short positions in sovereign bonds wouldhave to notifyregulators of their positions. Thiswould include such positions obtainedthrough the use of CDS. Thiswouldenableregulators to monitor whethersuch positions are creatingdisorderlymarkets or systemicrisks or beingused for abusive purposes. • Powers for regulators to obtain information in individualcasesabout CDS transactions. • Powers in an emergency for a competent authority to temporarilyprohibit or restrict the use of CDS. Suchemergencymeasureswould be temporary in nature and subject to coordination by ESMA.

exemptionsdiscussed • Limited exemptions are discussed in the consultationdocument, notably for market making, whichisimportant to the efficiency of markets and where the requirementscouldseverelyinhibittheirability to provideliquidity to Europeanmarkets.

15.09.2010 – Commissionadoptsproposal for a Regulation on short selling and certainaspects of Credit Default Swaps • Short selling of financialinstrumentsbeingusedas part of an abusive strategy, for example the use of short sales in connection with the spreading of false rumours to drive down the price of a security, isalreadyprohibited under the Market Abuse Directive 2003/6/EC

volume of short selling • Itisdifficult to obtainreliable data on the extent of short selling of shares in Europe in the absence of marking of transactions, or of disclosure of short sellingtransactions. Mostregulatorsconsulted by the Commissionwereunable to providereliable data on the volume of short sellingtransactions in theirjurisdictions. However, the level of securitieslending can be usedas a proxy and according to this data, short selling in Europe could be estimated to representbetween 1 and 3% of market capitalisation. • Using the data on disclosures of net short positions available from some MemberStates (e.g. UK and Spain) itcould be estimated to be lessthan 1% of the total share capital of the issuer. • Accordingto data obtained from Greece, whichhas a system of flagging in place, the volume of short sellingis in a range of 0 to 3.33%of the total volume of shares traded.

Whotrades in CDS and why? • There are fourmaingroups of market participants in the CDS market: dealers, non-dealer banks, hedge funds and assetmanagers. • CDS can be used for the followingpurposes: • hedging: CDS can be used to neutralise or reduce a risk to which the CDS buyer isexposed from another position. An example of such an "insurableinterest" would be a bondholder'sexposure to the credit risk of the issuer of the bond; by buying a CDS he can reduce thatrisk by passingit on to the CDS seller; • arbitrage: The typicalarbitrageoperationthatinvolves CDS is the combination of buying a CDS and enteringinto an asset swap where the fixed coupon payments of a bond are swappedagainst a stream of variablepayments; or • speculation: CDS can also be used to take a position in order to exploit pricechanges by trading in and out. For example, a CDS seller hastaken on risk (in exchange for the regular payments he receives from the CDS buyer); he will gain from the contractif the credit riskdoesnotmaterialiseduring the contract'sterm or if the compensationreceivedwillexceed a potentialpayout.

volume of CDS transactions • At the end of May 2010, the grossnotionalamount of the total CDS market wasestimatedat USD 14.5 trillion, with about 2.1 millioncontractsoutstanding. • The sovereign CDS market, whichincludesbothsovereignindices and sovereign single names, reached USD 2.2 trillion, with about 0.2 millioncontractsoutstanding. • The outstandinggrossnotionalamount of the ItraxxSovereign Index Western Europe was USD 140 billion (and USD 10 billion in net terms).

aims • Whilereducing the scope for regulatoryarbitrage and compliancecostsarising from a fragmentedregulatoryframework, the threemainrisks of short sellingwhich the Commissionisseeking to address in theseproposals are: • transparencydeficiencies: the currentlack of transparency in relation to short sellingpreventsregulators from beingable to detectat an early stage the development of short positions whichmay cause risks to financialstability or market integrity. Greater transparency to the market on short sellingwoulddeter aggressive short selling and giveuseful information to the market abouthow short sellers view the performance and prospects of companies. • the risk of negative pricespirals: manyregulatorshaveexpressedconcernsabout the risks of short sellingamplifyingpricefalls in distressedmarkets, and thatthiscouldlead to systemicrisks. Itwas due to theseconcernsthat a number of MemberStatesintroducedemergencymeasures to restrict or ban short selling in some or all shares in autumn 2008. Concernshavealsobeenexpressed by some MemberStatesthat short positions through CDS transactionscould in some circumstancescontribute to a decline of sovereign bond prices. • the risks of settlementfailureassociated with naked short selling: when a short seller sells a financialinstrument short without first borrowing the instrument, enteringinto an agreement to borrowit, or locating the instrument so thatitisreserved for borrowingprior to settlement ("naked short selling"), thereis a risk of settlementfailure. Some regulatorsconsiderthatthiscouldendanger the stability of the financialsystem, as in principle a naked short seller can sell an unlimitednumber of shares in a very short space of time.

the transparency of short selling 1/2 • - for shares: • For EU shares the proposals to enhancetransparency are largelybased on the twotier model recommended by CESR (the Committee of European Securities Regulators) in its report in March 2010. At a lowerthreshold (0.2% of the issued share capital) notification of a short position would be made only to the regulator and at a higherthreshold (0.5%) short positions would be disclosed to the market. Notification to regulatorswouldenablethem to monitor and, ifnecessary, investigate short sellingthatmay pose systemicrisks or be abusive. Publication of information to the market wouldprovideuseful information to other market users and actas a disincentive to aggressive short sellingstrategies. • The disclosure regime for shares iscomplemented by a system of flagging: all share orders on trading venueswould be markedas 'short' by personsexecutingordersifthey involve a short sale, so thatregulators can obtainadditional information about short selling

the transparency of short selling 1/2 • A specific regime for notification to regulatorsonly of significant net short positions in EU sovereign bonds isproposed. Thiswouldalso include notification of significant credit default swap positions relating to sovereigndebtissuers. Disclosure to regulators of significant net short positions relating to EU sovereign bonds couldprovideimportant information to assist regulators to monitor whethersuch positions are creatingdisorderlymarkets or systemicrisks or are beingused for abusive purposes. The proposals on sovereign bonds provides for information to be disclosedonly to regulatorsratherthan to the market as public disclosurecouldhave negative consequences for the operation of sovereign bond markets, notably in terms of liquidity. The evidence from the short sellingdisclosureregimes for shares atnationallevelisthatthesehavenothad an undue impact on the liquidity of share markets. • In order to avoidanycircumvention of the short sellingdisclosurerulesthrough off-exchange derivative transactions, the transparencyregimes for EU shares and EU sovereign bonds also cover the use of derivatives to obtain a net short position relating to the shares or bonds. The proposalsalsorequirethat short positions should be subtracted (or 'netted off') from long positions, asnotification of a net short position provides more meaningful information to regulators and/or the market.

powers are proposed for regulators in exceptionalsituations • In distressedmarketswhen short selling can amplify a downwardpricespiral, transparency alone maynot be enough. The proposalprovidesthat in exceptionalsituations, competentauthorities (i.e. financialregulators) shouldhavepowers to impose temporarymeasuressuchas to requirefurthertransparency or to restrict short selling and credit default swap transactions. Thesepowersextend to a wide range of instruments. The proposalseeks to harmonise the powers and define the conditions and proceduresthat must be complied with if the powers are to be exercised. Currently, some MemberStateshavepowers to act on short selling in exceptionalsituations and haveusedthesepowers, whereasothers do not. • ESMA isgiven a centralrole in coordinatingaction in exceptionalsituations and ensuringthatpowers are onlyexercisedwherenecessary

roleisproposed for ESMA to ensurecoordination in exceptionalsituations • ESMA isgiven an importantrole in coordinatingaction in exceptionalsituations. • Competentauthorities must notify ESMA of the measuresthey propose to take (or renew) in such a situation, notlessthan 24 hours before the entry into force of the measures (thisperiodmay be shorter in exceptionalcircumstances). • ESMA shallconsider the information received and issue an opinion (within 24 hours) on whether the measure or proposedmeasureis appropriate and proportionate to address the threat, and whethermeasures by othercompetentauthorities are necessary. • Wherea competent authority takesactioncontrary to ESMA's opinion itshallpublish a noticegivingitsreasons for doing so.

ESMA isgiven an importantrole in coordinatingaction in exceptionalsituations. • Competentauthorities must notify ESMA of the measuresthey propose to take (or renew) in such a situation, notlessthan 24 hours before the entry into force of the measures (thisperiodmay be shorter in exceptionalcircumstances). • ESMA shallconsider the information received and issue an opinion (within 24 hours) on whether the measure or proposedmeasureis appropriate and proportionate to address the threat, and whethermeasures by othercompetentauthorities are necessary. Where a competent authority takesactioncontrary to ESMA's opinion itshallpublish a noticegivingitsreasons for doing so.

Regulation (EU) No 236/2012 of the EuropeanParliament and the Council of 14 March 2012 on short selling and certainaspects of Credit Default Swaps • Accordingto Regulation (EU) No 236/2012, short selling of shares can onlyhappenif sellers eitherhaveborrowed the shares, have a bindingagreement to borrow the shares, or have an arrangement with a third party thatmeansthey can reasonablyexpect to deliver the shares they are selling. • The technicalstandardsadoptedtoday set out the technicaldetails of howthisRegulationwillapply in practice, notably the types of agreements, arrangements and measuresthatadequatelyensurethat the shares sold short are available for settlement. Theywillapply from 1 November 2012.

Restrictionsprovidedfor in the Short SellingRegulation on naked short selling • For shares: In order to enter a short sale, an investor must haveborrowed the instrumentsconcerned, enteredinto an agreement to borrowthem, or have an arrangement with a third party under whichthatthird party hasconfirmedthat the share hasbeenlocated and hastakenmeasures vis-à-vis third parties necessary for the investor to havereasonableexpectationthatsettlement can be effectedwhenitis due. Thisisknownas a 'locate rule'. ESMA shalldevelop a draftimplementingtechnicalstandards to determine the types of agreements, arrangements and measuresthatadequatelyensurethat the share will be available for settlement. In determiningwhatmeasures are necessary to ensure a reasonableexpectationthatsettlement can be effectedwhenitis due, ESMA shall take into account amongothersintraday trading and the liquidity of the shares. To detersettlementfailures, trading venues must alsoensurethatthere are adequatearrangements in place for the buy-in of shares wherethereis a settlementfailure, aswellas for fines.

For sovereigndebt: In order to enter a short sale an investor must haveborrowed the instrumentsconcerned, enteredinto an agreement to borrowthem, or have an arrangement with a third party under whichthatthird party hasconfirmedthat the share hasbeenlocated or hasotherwisereasonableexpectationthatsettlement can be effectedwhenitis due. The restrictions do notapplyif the transactionserves to hedge a long position in debtinstruments of an issuer, the pricing of whichhas a high correlation with the pricing of the givensovereigndebt. In addition, the competent authority maytemporarily (for 6 months, renewable) suspendtheserestrictionswhere the liquidity of the sovereigndebtfallsbelow a pre-determinedthreshold, to be set by the Commission in a delegatedact. ESMA shalldevelop a draftimplementingtechnicalstandards to determine the types of agreements, arrangements and measuresthatadequatelyensurethat the sovereigndebtwill be available for settlement.

PracticalEffect • The new Regulationmeansthat in relation to the short selling of shares and of sovereigndebtinstruments and the taking of sovereign credit default swaps positions the followingrequirementsapply: • Allthoseenteringinto short sales of shares must be covered by eitherhavingborrowed the instrumentsconcerned, havearranged to borrowthem; or have an arrangement with a third party whohasconfirmedthat the share hasbeenlocated i.e. naked short selling in shares isnowbanned; • Allthoseenteringinto short sales of sovereigndebtinstruments must haveborrowed the instrumentsconcerned, have an agreement to borrowthem, or have an arrangement with a third party whohasconfirmedthat the share hasbeenlocated or expectsthat the trade can be settledwhen due i.e. naked short selling in sovereigndebtisnowbanned • Allthoseenteringinto credit default swaps positions related to a sovereignissuer must have an underlyingexposure to the risk of default of thatsovereignissuer or of a decline in the value of the sovereigndebt of thatissuer i.e. nakedsovereign CDS are nowbanned. • Central counterpartiesproviding clearing services must ensurethatthere are adequatearrangements in place for buy-in of shares aswellasfineswherethereis a settlementfailure

Mandatorytransparency of net short positions: • significant net short positions in shares must be • reported to the relevantcompetentauthoritieswhentheyatleastequal to 0.2% of company issued share capital and every 0.1% abovethat; • disclosed to the publichwhentheyatleastequal to 0.5% of company issued share capital and every 0.1% abovethat. • significant net short positions in sovereigndebtshould be reported to the relevantcompetentauthoritieswhenreaching or crossingone of the thresholdspublished by ESMA for sovereignissuers– notificationthresholds, • Exemptions are available for market makingactivities and authorisedprimary dealers;

According to the provisions of the Regulation, ESMA willhave to provide for public access to certaintypes of information: • Significant net short position notificationthresholds for eachsovereignissuer (Article 7(2)); • Links to centralwebsitesoperated or supervised by competentauthoritieswhere the public disclosure of net short positions isposted (Article 9(4)); • The list of shares for which the principal trading venueislocated in the third country (Article 16(2)); • A list of market makers and authorisedprimary dealers (Article 17(3)); • A list of existingpenalties and administrativemeasuresapplicable in MemberStates (Article 41).

ESMA’scoordinationrole in exceptionalcircumstances • ESMA hasbeengiven the role of coordinating the scope and implementation of anyproposedemergencymeasures by nationalcompetentauthorities (NCA). The systemwillfunctionasfollows: • The NCA notifies ESMA of itsintention to take emergencymeasures, setting out the reasons for the action and the type of measures to be taken; • ESMA has 24 hours in which to issue an opinion on whetheritconsiders the measure appropriate and proportionate to address the threat and alsoif the time durationisjustified; • The opinion shall be published on ESMA’s website; • If a NCA takesmeasuresdespite a negative ESMA opinion it must thenpublish, within 24 hours, of the ESMA decision an explanation for doing so; • ESMA willregularlyreviewemergencymeasurestaken under the Regulation, atleastevery 3 months.

29.06.2012 – Commissionadoptstechnicalstandards on short selling • The technicalstandardsadoptedlayout in detail: • the differenttypes of agreements, arrangements and measuresthatadequatelyensurethat the shares sold short are available for settlement; • the functioning of the "locate rule" for shares and sovereigndebt; • the mechanisms of information disclosure, to increasetransparency in short selling; • requirements on the types of third parties that can be involved in short selling; and • the method for determiningwhich shares have a principal trading venueoutside the EU and are thereforeoutside the scope of the Short SellingRegulation.

What are the differentkinds of agreementsthatadequatelyensuresettlement for short selling of shares and sovereigndebt? • The types of agreements are: • futures and swaps; • options; • repurchaseagreements; • standing agreements or rollingfacilities; • agreementsrelating to subscriptionrights; and • otherclaims or agreementsthatlead to the delivery of shares or sovereigndebt for the purposes of short selling.

"locate rule" • The "locate rule" is a termused to describe the arrangementwhereby a broker confirms to a short seller thattheyhavelocated the shares which the short seller needs to borrow to cover their short sale, takinginto account the amountrequired and market conditions. Itisthanks to thisarrangement and the subsequentmeasures to be taken vis-à-vis third parties that the short seller isable to have the reasonableexpectationthat he can deliver the shares he is short selling. The locate ruleis an essential part of EU law on short selling: without location of the shares to be sold short, and the subsequentmeasures vis-à-vis third parties, short selling of shares isnotpermissible. • There are threedifferent ways that the locate rule can work which are detailed in the technicalstandards: • The broker confirms he haslocated the shares to be sold, and he atleastputsthem on hold. Thisis the standard functioning of the locate rule. • In the case of short sellingthatis to take placewithin the sameday, knownasintraday short-selling, the short seller needs first to inform the broker thatthisishisintention. The broker thenconfirms he haslocated the shares to be sold. The broker thenhas to eitherconfirmthat the share is easy to borrow or purchase, or ifnotthat he hasatleast put the requiredamount of shares on hold. The short seller must monitor the market, and if he finds he risksnotbeingable to deliver, he must thengive an instruction to the broker to buy the shares needed to cover his short sale. • In the case of liquid shares, the broker confirms he haslocated the shares to be sold, and thateither the shares are easy to borrow or purchase in the requiredamount, or that he hasatleast put them on hold. The short seller gives the broker a commitmentthat he willgivehim an instruction to buy or borrow the shares needed to cover his short sale ifittranspiresthat he isnotable to buythem in the market.

uncovered short selling of sovereigndebt • The requirements for uncovered short selling of sovereigndebt in the Short SellingRegulation are differentthanthose for shares, to reflect the specificities of the sovereigndebtmarkets. The keydifferenceisthatunlike for shares, for sovereigndebtthereis no requirement on the third party to put the sovereigndebt on hold. According to the technicalstandards, for short sales of sovereigndebtthere are fourdifferentkinds of arrangementsthatmake short sellingpermissible: • A third party (broker) must confirmthat the sovereigndebthasbeenlocated, thatis to saythatitconsidersthatit can make the sovereigndebtavailable for settlement in due time; • In the case of intra-day short selling of sovereigndebt, the short seller has to confirm to the broker thatthisishisintention; the third party (broker) thenconfirms to the short seller thatithas a reasonableexpectationthat the sovereigndebt can be purchased in the relevantquantity, takinginto account the market conditions and other information available to it. • The short seller goesthrough a third party whichparticipates in a structuredarrangement, suchasoneorganised by a centralbank, thatgivesitunconditionalaccess to the sovereigndebt to be sold short in the amountrequired for settlement, and can thereforeconfirmthatithas a reasonableexpectationthatsettlementwill take placewhen due. • A third party (broker) confirmsthat the sovereigndebtbeingsold short is easy to purchase in the relevantquantitytakinginto account market conditions.

the detailedtechnicalrules on information disclosure • In order to improvetransparency of short selling, the Short SellingRegulationrequires information on significant short sales of shares and sovereigndebt to be notified to the regulator, once a reporting thresholdhasbeencrossed. For shares, the thresholdrepresents a short position of 0.2% or more of thatcompany's share capital. For sovereigndebt, the thresholds are to be set by the Commission in the delegatedact to be adoptedshortly. For shares only, if the short position represents 0.5% or more of the issued share capital, information on the sale needs to be disclosed to the public.

05.07.2012 – Commissionadoptsdelegatedact and regulatorytechnicalstandards on short selling • The Commissionisempowered by the Short Selling Regulation1 to adoptdelegatedacts by 31 March 2012 (which can be extended by 6 months) specifyingcertaintechnicalelements of the Regulation, to ensureitsconsistentapplication and to facilitate itsenforcement. The technicalissues to be addressed in thesedelegatedacts are set out in the Regulation and are explainedfurtherbelow.

procedure for adoptingthisDelegatedRegulation • The DelegatedRegulationis a delegatedact of the EuropeanCommission. Thisis an autonomousact of the Commissionwhichisdrafted and adopted by the Commission. While the Commissionhasrequested and takeninto account the technicaladvice of the European Securities and Markets Authority (ESMA) on the technicalissuescovered by thisdelegatedact, the Commissionisnotbound in any way by thisadvice. Prior to issuingitsfinaltechnicaladvice, ESMA consultedstakeholders on drafttechnicaladvice. The Commissionhasalsoprepared an impact assessmentaccompanying the DelegatedRegulationwhichconsiders the impacts of the differentoptions, aswellas the technicaladvice of ESMA and the views of stakeholders. In itspreparatory work the Commissionhasalsoconsulted the expertgroup of the European Securities Committee, the EuropeanParliament, and the European Central Bank. Followingadoption by the Commission, thisDelegatedRegulationissubject to a threemonthobjectionperiodduringwhicheither the EuropeanParliament or the Council can object to the DelegatedRegulation; thisperiod can be extended by a furtherthreemonths. Ifneither of the co-legislatorsobjectsduringthisperiod, the DelegatedRegulationispublished in the Official Journal and entersinto force. Providedthat the co-legislators do notexercisetheir right to object, the DelegatedRegulationisthereforeexpected to be published in the Official Journal by mid-October and to enterinto force on 1 November 2012, the date of application of the Short SellingRegulation.