Download

1 / 14

140 likes | 350 Views

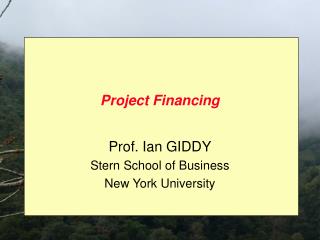

Major Intercreditor Issues in Multi-tranche Project Financing Transactions. John D. Taylor June 9, 2005. Indenture/Note Purchase Agreement. Capital Markets Lenders. Loan Agreement. National Development Lender. Common Agreement. Collateral Agency/ Trust Agreement. Collateral

E N D

Major Intercreditor Issues inMulti-tranche Project FinancingTransactions John D. Taylor June 9, 2005

Indenture/Note Purchase Agreement Capital Markets Lenders Loan Agreement National Development Lender Common Agreement Collateral Agency/ Trust Agreement Collateral Agent/ Trustee Project Company Borrower Loan Agreement Multilateral Financial Institution Loan Agreement Lead Commercial Banks as Agents/Underwriters Political Risk Guarantee Syndicate of Commercial Banks Export Credit Agency Security Agreements: Cash Collateral Agreement Pledge Agreement Assignment Agreement Mortgage Sample Financing Structure

Elements of Intercreditor Agreement • Appointment of Intercreditor Agent • Sharing Provisions • Voting/Decision-making • Default/Remedial Action

Sharing Provisions • General Rule: Pro Rata Sharing • Payments • Security • Some Exceptions • Separate Security (pledge of additional security, additional reserve account, etc.) • Political Risk Insurance Proceeds • “Preferred Creditor” Status

Voting/Decision-Making I → Who Decides? • Allocating Voting Power • Purely Proportional • Consensus • 800-pound Gorilla • Lender Goals • Efficiency • Minimize Hold-out Risk • Protect Key Interests

Voting/Decision-Making II → How Are Decisions Made? • Role of Agent • Unilateral Action: Agent as decision-maker • Group Action: Agent as decision-facilitator • Voting Mechanics

TriggeringEvent/BorrowerRequest VotingDeadline LenderDecision Agent Solicitation Consultation/Voting Period Lender Decision-making Timeline

Lender Voting Group Unanimous Lenders Supermajority Lenders Majority Lenders Single Lender (Veto Right) Single Lender (“Interested” Lender) Lender Voting Group Unanimous Lenders Supermajority Lenders Majority Lenders Single Lender (Veto Right) Single Lender (“Interested” Lender) Lender Voting Group Unanimous Lenders Supermajority Lenders Majority Lenders Single Lender (Veto Right) Single Lender (“Interested” Lender) Lender Voting Group Unanimous Lenders Supermajority Lenders Majority Lenders Single Lender (Veto Right) Single Lender (“Interested” Lender) Lender Voting Group Unanimous Lenders Supermajority Lenders Majority Lenders Single Lender (Veto Right) Single Lender (“Interested” Lender) Description/Comment Fundamental matters for which each lender must consent/approve Fundamental matters for which lenders seek a “heightened” voting threshold A common “baseline” for decision-making relies on majority rule Matters for which a lender requires a veto right due to its heightened sensitivity to matter Matters that are only of interest to individual lender Description/Comment Fundamental matters for which each lender must consent/approve Fundamental matters for which lenders seek a “heightened” voting threshold A common “baseline” for decision-making relies on majority rule Matters for which a lender requires a veto right due to its heightened sensitivity to matter Matters that are only of interest to individual lender Description/Comment Fundamental matters for which each lender must consent/approve Fundamental matters for which lenders seek a “heightened” voting threshold A common “baseline” for decision-making relies on majority rule Matters for which a lender requires a veto right due to its heightened sensitivity to matter Matters that are only of interest to individual lender Description/Comment Fundamental matters for which each lender must consent/approve Fundamental matters for which lenders seek a “heightened” voting threshold A common “baseline” for decision-making relies on majority rule Matters for which a lender requires a veto right due to its heightened sensitivity to matter Matters that are only of interest to individual lender Description/Comment Fundamental matters for which each lender must consent/approve Fundamental matters for which lenders seek a “heightened” voting threshold A common “baseline” for decision-making relies on majority rule Matters for which a lender requires a veto right due to its heightened sensitivity to matter Matters that are only of interest to individual lender Examples Tenor/pricing of loans; release of collateral Incurrence by Borrower of additional debt; amendments to security documents Approval of budget; approval of insurance arrangements Environmental matters; potentially matters identified in Credit Committee approval Non-material changes to a lender’s facility agreement Examples Tenor/pricing of loans; release of collateral Incurrence by Borrower of additional debt; amendments to security documents Approval of budget; approval of insurance arrangements Environmental matters; potentially matters identified in Credit Committee approval Non-material changes to a lender’s facility agreement Examples Tenor/pricing of loans; release of collateral Incurrence by Borrower of additional debt; amendments to security documents Approval of budget; approval of insurance arrangements Environmental matters; potentially matters identified in Credit Committee approval Non-material changes to a lender’s facility agreement Examples Tenor/pricing of loans; release of collateral Incurrence by Borrower of additional debt; amendments to security documents Approval of budget; approval of insurance arrangements Environmental matters; potentially matters identified in Credit Committee approval Non-material changes to a lender’s facility agreement Examples Tenor/pricing of loans; release of collateral Incurrence by Borrower of additional debt; amendments to security documents Approval of budget; approval of insurance arrangements Environmental matters; potentially matters identified in Credit Committee approval Non-material changes to a lender’s facility agreement “Required” Lenders

Default/Remedial Action • Goals - Requirements vs. Reality • Procedures - Notice of Default/Consultation Period/Waiver or Exercise of Remedial Action

If Necessary Lenders agree to waive WAIVER If Necessary Lenders elect to enforce remedies Remedial Action If Necessary Lenders subsequently agree to waive WAIVER Remedial Action – Decision-making Agent Notice to Lenders/ Request for Instruction Default If No Lender Decision/ Commencement of WAITING PERIOD No Remedial Action until requested by Required Lenders – STEP DOWN–MECHANIC

Non-Fundamental Default Fundamental Default 100 % of Lenders 66⅔ 51 90 Days 120 Days 30 Days 60 Days Time Remedial Action – “Step Down”

Swap Provider Issues • Risks and Benefits of Swap Involvement • Nature of Swap • Coordination and Integration of Swaps • Swap Voting Rights • Swap Termination Rights • Swap Termination Payments

Equity-related Intercreditor Issues • Role of Borrower • Borrower Interest in Intercreditor Matters • Spectrum of Structures • Sponsor Debt