Download

1 / 34

390 likes | 542 Views

Learn about the accounting cycle, from recording transactions to posting in the general ledger. Understand the importance of journalizing and how to analyze business transactions efficiently. Improve your accounting skills with practical examples and tips.

E N D

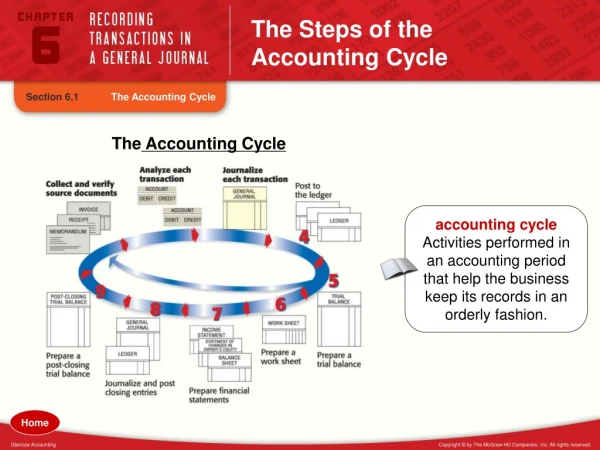

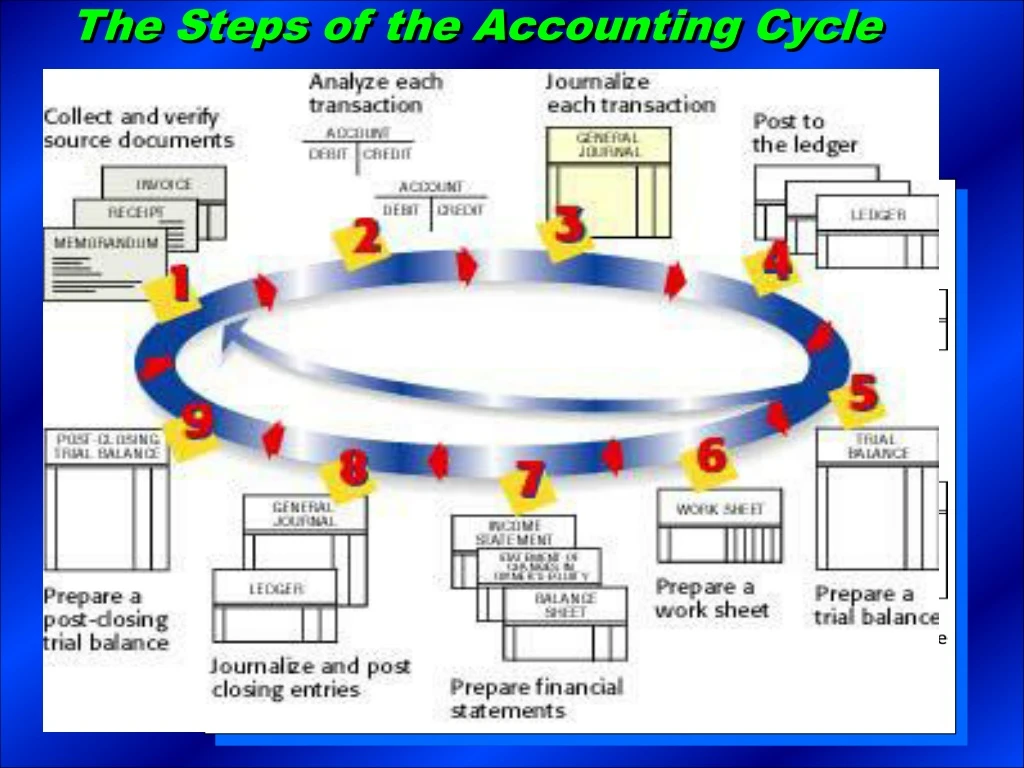

The Accounting Period • Accounting records are summarized for a certain period of time, called an accounting period or fiscal period. • An accounting/fiscal period can be: • Monthly, Quarterly, Yearly • If yearly, it can cover a • Calendar year • January 1 - December 31 • Any period of twelve months • Example: July 1 – June 30 $ $ $ $

Section 1 The Accounting Cycle (cont'd.) Chapter 6 $ The Second Step in the Accounting Cycle: Analyzing Business Transactions $ $ • Analyzing business transactions to determine • the accounts effected • the account(s) to debit and the amount • the account(s) to credit and the amount $

BUSINESS TRANSACTION ANALYSIS ANALYSISIdentify 1. Identify the accounts affected. Classify 2. Classify the accounts affected. + / – 3. Determine the amount of the increase or decrease for each account affected. 4. Which account is debited? For what amount? 5. Which account is credited? For what amount? 6. What is the complete entry in T- account form? 7. What is the complete entry in general journal form?

The Third Step in the Accounting Cycle: Recording Business Transactions in a Journal $ • What do you record? • the debit and credit parts of each business transaction in a journal. • A journal is • a chronological record of all of the transactions of a business – the book of original entry. • Journalizing is • the process of recording business transactions in a journal is called journalizing. $ $ $

What is a General Journal ? It is an all purpose journal in which all the transactions of a business may be recorded.

The parts of the general journal entry Not written in until entry is posted. It will contain the general ledger account # the entry is posted to. Name of the account debited Year & Month - At the top of each page and when the month changes Day – for each and every transaction Page # Amount of the debit Name of the account credited Source document reference or an explanation Amount of the credit

Recording a General Journal Entry • The debit part of the entry is at the left margin in the description column • The credit part of the entry is indented approximately ½” • The explanation is indented an additional ½” • This allows for easier reading of the journal.

Business Transaction 1 Maria Sanchez, Cash in Bank Capital Debit 25,000 Credit – Debit – Credit + 25,000 Recording a General Journal Entry On October 1, Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service, Memorandum 1.

Business Transaction 2 Delivery Accounts Payable— Equipment North Shore Auto Credit – Debit – Debit + 12,000 Credit + 12,000 Recording a General Journal Entry On October 9, Roadrunner bought a used truck on account from North Shore Auto for $12,000, Invoice 200.

Correcting Errors in General Journal Entries $ • An error should never be erased. • To correct an error in your general journal • Draw a horizontal line through the entire incorrect item and write the correct information above the crossed-out error. $ $ $

The Fourth Step in the Accounting Cycle: Posting • Posting is transferring the information from the journal to the proper accounts in the general ledger • Provide a clear picture of how each account is affected by a business transaction. • Posting brings the records of the business up-to-date • Posting leaves an audit trail to easily trace a transaction to its original book of entry!! Page 3

General Journal Asset Accounts Expense Accounts Owner Equity Accounts LiabilityAccounts Revenue Accounts General Ledger What is the General Ledger? a book or file that contains the accounts used by a business on separate pages or cards. Page 3

Chapter 7 $ The Four-Column Ledger Account Form $ $ $

Chapter 7 $ Opening an Account with a Zero Balance (1) Write the account name at the top of the ledger account form. $ • Write the account number on the ledger account form. • Write nothing else. $ 2 1 $

Chapter 7 $ Opening an Account with a Balance (1) Write the account name at the top of the ledger account form. $ (2) Write the account number on the ledger account form. $ $

Chapter 7 $ $ (3) Enter the complete date (year, month, and day) in the date column. (4) Write the word “Balance” in the Description column. $ $

Chapter 7 $ (5) Place a check mark () in the Posting Reference column to show the amount entered on this line is not being posted from a journal. $ $ (6) Enter the balance in the appropriate balance column of the ledger account form. $

Posting entries in the general ledger from the general journal. Left blank unless a correcting, closing or adjusting entry. The debit amount of the journal entry The new balance in the account; always on the normal balance side The date of the journal entry The journal and journal page number posting from $

Posting entries in the general ledger from the general journal. • Posting is done from left to right. • The general ledger account number is then recorded in the general journal post reference column • Then repeat the posting process for the credit part of the entry in the general journal. Page 3

Business Transaction 1 after posted to general ledger 101 301

Computing a New Account Balance • Accounts with normal debit balances use the debit balance columns: • Debit amounts are added to debit balances • Credit amounts are subtracted from debit balances • Accounts with normal credit balances use the credit balance columns: • Credit amounts are added to credit balances • Debit amounts are subtracted from credit balances. • The new balance (calculated after each posting) should be recorded on the normal balance side. • If the new balance is zero, a line should be drawn across the center of the balance column on the side of the normal balance.

PostingDate rules when posting to the general ledger: • Year & Month • At the top of each account • And when the month changes • Day – for each and every transaction posted • The frequency of posting depends on: • The size of the business • The number of transactions being processed • If a manual or computer system is being used • Most business post DAILY Page 3

Section 3 Preparing a Trial Balance Chapter 7 $ The Fifth Step in the Accounting Cycle: The Trial Balance • A formal way to prove that debits equal credits is to prepare a trial balance. • Prepared on two-column accounting stationery. • Three line heading: • Who – the name of the business • What – the name of the accounting form • When – the fiscal period covered. • Prepared • Normally at the end of the fiscal period • Can be prepared at any time during the fiscal period • Accounts included • All accounts - even zero balance accounts $ $ $

Chapter 7 Finding Trial Balance Errors • Add the debit and credit columns again. • Determine the amount you are out of balance • If the difference is 10, 100, 1000, possibly an addition error – Re-add columns again • If the difference is evenly divisible by 9, you may have a • transposition error – two numbers have been accidentally reversed. Check balances against general ledger • slide error – decimal point moved. Check balances against general ledger • Check general ledger for a balance that matches the difference; one account may have been omitted • If the difference is divisible by 2, possibly one of the balances has been recorded in the wrong column. Check balance types against general ledger. • Recompute the balances in the general ledger. • Check postings from general journal to general ledger. Page 3

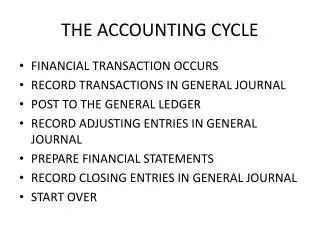

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents $ • The accounting cycle starts by • collecting and verifying the accuracy of source documents. • A source document is • a paper prepared as evidence of a transaction. • Examples: • Invoice • Receipt • Memorandum • Check Stub $ $ $

Chapter 6 $ Source Documents - Invoice $ $ Invoice (2 kinds – Buy and Selling): Invoices for items your business is buying are issued by your creditors. Invoices you issue for services/items your business is selling are issued to your customers. The invoice lists the date of the transaction, the terms, along with the quantity, description, and cost of each item. $

Chapter 6 $ Source Documents - Receipt $ $ Receipt: A record of cash received by a business. It indicates the date the payment was received, the name of the person or business from whom the payment was received, and the amount of the payment. $

Chapter 6 $ Source Documents - Memorandum $ $ $ Memorandum: A brief written message that describes a transaction that takes place within a business. Often used if no other source document exists for the business transaction.

Chapter 6 $ Source Documents - Check Stub $ $ Check Stub: The check stub lists the same information that appears on a check: the date written, the person or business to whom the check was written, and the amount of the check. The check stub also shows the balance in the checking account before and after each check is written. $

Chapter 7 Correcting errors • Error in a journal entry that is not posted • Correction: Draw a single line through the incorrect item in the journal and write the correction directly above. • Error in posting to the ledger when the journal entry is correct • Correction: Draw a single line through the incorrect item in the ledger and write the correction directly above • Error in a journal entry that is posted. • Correction: Make a correcting entry in the journal and post to the ledger • When posting to the ledger, include the words “Correcting Entry” in the description column Page 3