Download

1 / 13

130 likes | 241 Views

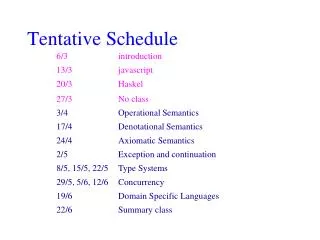

Tentative Agenda. GISC Update Mood of Industry, H.M.G. and Consumer Bodies Evolution and Change S trengths and Weaknesses of the System Conclusion. GISC Update:. Origins, Objectives and Launch Feedback to Consultation Rules Frequently Asked Questions Membership Statistics

E N D

Tentative Agenda • GISC Update • Mood of Industry, H.M.G. and Consumer Bodies • Evolution and Change • Strengths and Weaknesses of the System • Conclusion

GISC Update: • Origins, Objectives and Launch • Feedback to Consultation • Rules • Frequently Asked Questions • Membership Statistics • OFT and Rule 42

OFT and Rule 42 • First Consultation • Necessary Glue for the System • Members May Only Deal with GISC Intermediaries • Anti Competitive • OFT Clearance Required • Implementation of Rule 42

Mood of Industry, H.M.G. and Consumer Bodies: • Generally Supportive But Cautious About Change • H.M.G. Totally Supportive – IBRA Repeal 30 April • Board Commitment to be Sensible/ Pragmatic • Monitoring • Discipline • Consumer Groups Supportive But Expect More Public Interest Representation • Expectation for Rules to be Evolutionary

Evolution and Change - Political: • An Independent Regulator • Effective Engagement with Consumers • Relationship with the FSA • What is GISC’s Political Future? • Constitution

Constitutional Change: • Debate Commenced • Respect for Modern Corporate Governance • Members to be Enfranchised • Sectorial Representation • Increase of Public Interest Representation on Board • Consultation

Evolution and Change - Regulatory: • Responding to Industry • Comment on the Rules • Changing Market Practice • Specifics - Training and Competence - Approach to Discipline

A voluntary regime Self Regulation Itself Compromise Inability to Intervene Lack of Immunity for Directors Willingness to take on the Big Boys Not all Insurers Members Weaknesses of the System:

Strengths of the System: • There is a System • Coherent and Single • Well Supported • H.M.G. want it • Reflects Good Business Practice

Regime Good for Competition: • Promotes a Single Coherent System • Is Administered by an Independent Regulatory Body • Recognises the Different Circumstances of Firms • Does Not Inhibit Product Choice • Facilitates Opening of Lloyd’s

Regime Good for Consumers: • Direct Regulation • Customer Codes • Complaints Handling • Monitoring of Compliance • Financial Requirements for Intermediaries • Competence and Training of Individuals

Conclusion • The Messages are: • Regulation is Not an Option • Grasp the Opportunity to Make it Work • Regulation should Not be seen as a Burden provided it: • Reflects Good Business Practice • Is Appropriate and Proportionate • Peer and Customer Pressure is Coming • Consumer Education is on the Agenda