Download

1 / 2

20 likes | 45 Views

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

E N D

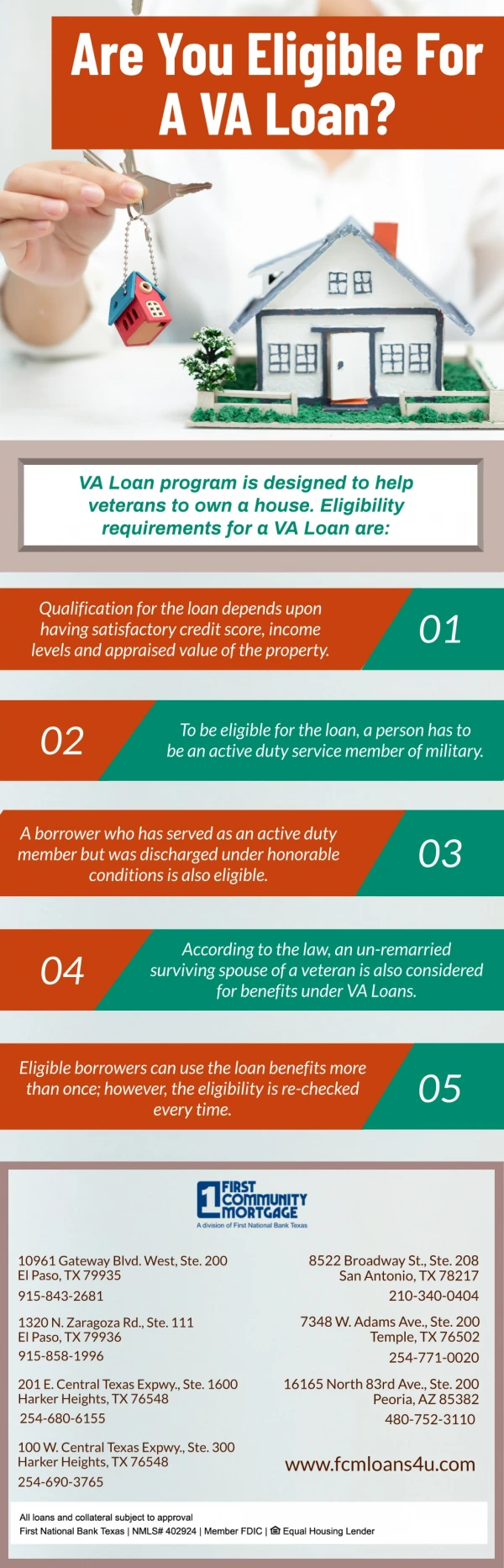

Am I Eligible for a VA Loan? Being eligible for a VA loan is a great possibility if you have served in the armed forces, but being a vet is only the first test. Veterans appreciate gestures of gratitude for service rendered to their country. These can take the form of verbal acknowledgement or show up as a financial donation to aid wounded warriors. The government also provides benefits that demonstrate the high value placed on military service. Most well-known are medical services yet there is another form of assistance of equal significance. The United States Department of Veterans Affairs (VA) guarantees home mortgage loans for qualified borrowers. How Do VA Loans Work? Vets apply for mortgage loans like everyone else: through a private bank or finance company. Important to remember is the fact that the government is guaranteeing the loan, i.e. agreeing to pay the lender in the event the borrower defaults, not advancing the money itself. For starters, the bank will require a VA Certificate of Eligibility (COE) before considering an applicant eligible for a VA loan. COEs are issued based on years and character of military service, and are obtained through the lender, a local VA office or the VA website. Subsequently, the lender will collect documentation to verify the information on the loan application. The difference between the VA loan and a conventional mortgage is that underwriters will apply VA standards in approving or denying the application.

Do I Need Good Credit? Yes, but it’s all relative. Whereas a conventional mortgage will require a strict minimum credit score of 620, applications with a VA guarantee are likely to receive more latitude since the bank knows it will be paid back one way or the other. Overseas deployments and frequent relocations can take a toll on a veteran’s finances, so the VA requires banks to look at the whole borrower profile before rejecting an application based on credit scores. How Much Do I Need to Earn to Be Eligible? A borrower’s revenues will rise and fall on how much money is sought. When underwriting mortgage loans, lending institutions rely on an index called the debt-to-income ratio. This means that they will tabulate all the monthly obligations—in other words, the bills—and add the proposed monthly mortgage payment. If this sum is less than 41 percent of the veteran’s total income, the bank is then confident that the borrower makes enough money to manage the loan payments. Do I Need Money in the Bank? It is not unusual for a finance company or bank to desire a financial cushion to carry the mortgagor through hard times. However, VA loans require only sufficient funds on hand for the down payment, closing costs and any additional equity not covered by the down payment. Are There Any Restrictions on the Property? The veteran might meet all the criteria and is eligible for a VA loan, but the loan can fall through if the house does not show clear ownership title for the seller or current owner. Unlike conventional loans, the bank can loan up to 100 percent of the property value when processing a VA application. As a VA Loan Specialist, I can help you navigate through the VA loan process. Contact me or click the big red Apply Now button and let’s get started.