Download

1 / 29

290 likes | 474 Views

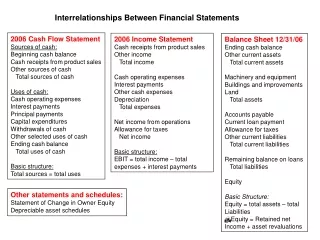

P-1: Enter cash receipts close to originating source. Ensure effectiveness of operations:

E N D

P-1: Enter cash receipts close to originating source Ensure effectiveness of operations: As reflected by the entries in goal columns A and B under process effectiveness, this application strategy results in processing cash receipts events on a timely basis based on input received directly from insurance agents. Ensure efficient employment of resources: In addition, the direct entry of input data by the bank operator provides for a more efficient employment of resources because this arrangement eliminates the need for a separate data entry function and the cost associated therewith. Agents’ customer initiated payments input accuracy: Because the bank operator is familiar with the type of event being entered and is entering the data while the agent is still on the phone, any input errors can be corrected “on the spot,” thereby improving input accuracy.

M-1: Reconcile bank account regularly. Agents’ customer initiated payments input validity and accuracy: By regularly reconciling its bank accounts, an organization confirms the validity and accuracy of the recorded cash receipts because the bank statements will reflect actual cash deposits. Ideally, the reconciliation should be performed by a person who is independent of those who handle and record cash receipts and disbursements. Accounts receivable general ledger update accuracy: Reconciliations also ensure that accounts have been accurately updated.

P-1: Independent billing authorization Completed slips input validity: The proof totals from the point-of-sale register are compared to the credit card slips before preparation of the NCC settlement sheets and the cash out report. The cash out report is later compared to the PCC slips before input of the PCC slips to update the customer accounts. These steps increase the validity of the credit card slips by verifying that the credit card input is supported by a sale entered at the register.

M-1: Confirm customer accounts regularly. Completed slips input validity and input accuracy: The customer can be utilized as a means of controlling the billing process. By sending regular customer statements, we use the customer to check that invoices were valid and were accurately entered. Accounts receivable update accuracy: Customer statements for review also help assure the accuracy of updates.

M-2: Check for authorized prices, terms, freight, and discounts. • Completed slips input validity: Note that the operative word, “authorized,” speaks to the control goal of input validity. • Completed slips input validity: Having these items independently checked by a second person helps to ensure input accuracy.

M-3: Edit the shipping notification for accuracy. • Completed slips input accuracy: We can greatly increase the accuracy of entering sales events by utilizing the computer to edit the data input (i.e., programmed edits). • Accounts receivable update accuracy: Additional edits could be performed during the update process.

M-4: Computer agreement of batch totals. • Completed slips input validity, completeness, and accuracy: By calculating and then reconciling (agreeing) batch control totals, we can ensure the control goals of input completeness (all source documents are processed), input validity, and input accuracy (data elements appearing on the source documents are processed correctly). • Ensure security of resources: Calculating and reconciling batch control totals also enhance resource security (only valid source documents comprise the batch that is processed). • Ensure efficient employment of resources: Since the totals are reconciled by the computer, there will be a more efficient use of personnel resources. • Accounts receivable update completeness and accuracy: Since totals could be reconciled after master data update, we have made entries in the columns for UC and UA.

M-5: Key verification • Completed slips input accuracy: To reduce the possibility that one person will misread or miskey data, documents are keyed by one individual and rekeyed by a second individual using a machine that checks the second keystroking against the results of the first keystroking. Key verification, of course, addresses the information process goal of ensuring input accuracy.

P-3: Procedures for rejected input. • Completed slips input validity, completeness and accuracy: At two places in the process, batch totals are reconciled. Presumably there would be error routines to process rejected events. These routines should improve the likelihood that events will be completely and accurately input in a timely manner. • Ensure efficient employment of resources: The error correction process should lead to more timely billing and a more efficient use of clerical time. • Ensure security of resources: The error correction associated with the cash out report should protect the cash resource. • Ensure effectiveness of operations: The error correction process helps ensure that customers are fully and accurately billed.

P-4: Enter data close to its originating source. • Ensure effectiveness of operations. As reflected by the entries under process effectiveness, this application strategy places users in a position to input sales events immediately and to get the credit card bills sent out promptly. • Ensure efficient employment of resources: In addition, the direct entry of input data by sales personnel provides for a more efficient employment of resources because this arrangement eliminates the need for a separate data entry function and the cost associated therewith. • Completed slips input completeness and accuracy. There would be less chance for the customer orders to be lost, thus improving input completeness. Further, because operations personnel are familiar with the type of event being entered and can correct any input errors “on the spot,” input accuracy should be improved. • Accounts receivable update completeness: Operations personnel monitoring of events should improve update completeness.

P-1: Requisition audit data Purchase requisition input completeness: While not an electronic file, the files of pending and completed purchase requisitions can be used to ensure the complete input of the purchase requisition. Should the supplies manager not receive a confirmation copy of the purchase order, or should he not receive a copy of the receiving report, he can follow up to determine the cause. The follow up will ensure the complete input of the purchase requisition.

M-1: Authorized vendor data. • Ensure effectiveness of operations: • Buyers in the purchasing department should start the vendor selection process by first consulting a vendor data, which contains only those vendors with whom the company is authorized to do business. The screening of vendors that preceded their being added to the “authorized” data should help ensure the first operations process goal: to select a vendor who will provide the best quality at the lowest price by the promised delivery date. • Purchase requisition input validity: • The blanket approval accorded to vendors who are placed on the authorizedvendor data also helps ensure the validity of purchase orders issued. • Ensure efficient employment of resources: • People resources (buyers’ time) are used efficiently because time is not wasted in searching for vendors that might not even supply the required goods or services.

P-2: Requisition confirmation to originating department. • Purchase requisition input completeness. Once the purchase order has been signed and released by the purchasing manager, a confirmation of the requisition should be sent to the requisitioner. Confirming the requisition helps to achieve the information control goal of input completeness.

M-2: Approve vendor selection. • Ensure effectiveness of operations: After the purchase order is checked against the requisition details, it should be approved—by adding an authorized approval to the purchase order. The approval includes the vendor chosen by the buyer. This control plan helps to improve the effectiveness of the purchasing operation by achieving the process goal of selecting the best vendor. • Purchase requisition input validity: The approval process also helps to ensure validity of the purchase order.

P-3: Written approvals. • Purchase requisition input validity: Written approvals help ensure the validity of events by determining that the event has been authorized. Approvals are entered by the production manager and checked in the purchasing department. • Ensure efficient employment of resources:Without such authorizations, inventory might be purchased and not be necessary or be purchased from an inappropriate vendor. • Ensure effectiveness of operations:Purchases of inventory from inappropriate vendors would also impact effectiveness.

M-3: Tickler file • Purchase requisition input completeness: • In general terms, a tickler file is a file of documents that is reviewed on a regular basis for the purpose of taking action to clear the items from that file. In the purchasing process, tickler files might be used in two places: • If the supplies manager was to check the open items in the file of open purchase requisitions, he could ensure that the purchase requisitions had been received in purchasing and had been “input” to create a purchase order. • If the file of open orders in the purchasing department was reviewed periodically, we could ensure that the vendor packing slip was input at the receiving department. • Vendor packing slip input completeness: • The receiving department should periodically check the file of purchase orders to determine the absence of vending packing slips.

P-4: Independent authorization to make payment. • Payment voucher input validity: A copy of the purchase order is sent to the accounts payable department and is used to authorize creation of a disbursement voucher. • Vendor invoice input validity: The validity of the vendor invoice and the payment voucher is thereby ensured. • Ensure security of resources: Because cash cannot be expended in the absence of a validated vendor invoice, the security of the cash is ensured.

P-5: Independent validation of vendor invoice • Vendor invoice input validity: The accounts payable manager reviews and approves the disbursement voucher and thereby provides independent assurance of the validity of the vendor invoice. • Payment voucher input validity: Review and approval of the disbursement voucher, of course, also provides independent assurance of the validity of the disbursement voucher.

P-6: Vendor invoice mathematical accuracy check • Vendor invoice input accuracy: The accounts payable function should match invoice items, quantities, prices, and terms to comparable data on the purchase order and receiving report to address the goal of vendor invoice accuracy (IA).

M-4: Tickler file. • Vendor invoice input completeness: In general terms, a tickler file is a file of documents that is reviewed on a regular basis for the purpose of taking action to clear the items from that file. In the accounts payable process, tickler files might be used by the purchasing department to review the open orders file to ensure receipt and input of the vendor invoice. • Payment voucher input completeness: The tickler file should also be used by the accounts payable department to periodically review their file of purchase orders to ensure receipt of the vendor invoice from purchasing.

M-2: Cumulative sequence check. • Purchase requisition and vendor packing slip input validity and input completeness: Although the process automatically assigns consecutive numbers to purchase requisitions, there appears to be no procedure for assuring that all such numbers are recorded by the process. A cumulative sequence check (see discussion in Chapter 9) could provide such assurance. In the case of receiving reports, there is no indication that they are prenumbered. If they were, the organization easily could account for all such numbers by employing a cumulative sequence check at a subsequent point in the processing.

P-2: Manual agreement of batch totals: • Completed slips input validity, completeness, and accuracy. The batch totals accumulated on the point-of-sale proof totals data and on the sales data are reconciled by the cashier and by the cash receipts clerks. These reconciliations ensure that the credit card slip inputs do not differ from the events entered at the point-of-sale register and are therefore valid, accurate, and complete. • Ensure security of resources: The use of batch totals helps ensure protection of the organization’s assets.

M-1: Immediately endorse incoming checks • Ensure security of resources: To protect the checks from being fraudulently appropriated, the checks • should be restrictively endorsed as soon as possible following their receipt in the organization. However, the NCC receipts go directly to the bank and this provides protection for the cash.

P-1: Deposit slip data. • Ensure security of resources: By maintaining completed deposit slip data, the cash receipts sections provides an audit trail to support each deposit, thereby protecting deposits from misappropriation.

M-2: Immediately separate checks and remittance advices. • Ensure security of resources: The checks should be separated from the remittance advices and the checks deposited as quickly as possible. The faster the checks are deposited, the less chance that the cash can be diverted. • Ensure effectiveness of operations. Quick deposit of checks and cash also allows for faster investment of cash (process goal A). At a minimum, cash should be deposited once a day.

P-3: Turnaround documents. • Ensure efficient employment of resources: Turnaround documents are an example of prerecorded data. A document, printed by the computer, is used to capture and input a subsequent event. This is more efficient than having someone rekey the data. • Remittance advice input accuracy: By reducing keying we also improve input accuracy.

One-for-one checking of goods, picking ticket, and sales order notification. • Ensure security of resources: • By requiring that data on the sales order notification be compared with that on the picking ticket and then that these data sets be compared to the actual goods being shipped, this plan ascertains that inventory shipments have been authorized. It also ensures that shipping notice inputs are represented by an actual shipment of goods. • Sales order notification input validity and input accuracy: • By ensuring that shipping notice inputs are represented by an actual shipment of goods, the goal of shipping notice input validity is addressed. The data that might be checked includes item numbers, quantities, and customer identification. Checking these details also operates to ensure that shipping events are accurate.

M-5: One-for-one checking of the invoices and the checks. • Payment voucher input validity and accuracy. • The cash disbursement manager should compare the output checks to the invoices and thus ensure that the disbursement voucher (the accounts payable record) is correct. • Accounts payable master data update accuracy: • The checking of invoices also ensures the correctness of the update to the accounts payable master data. • Ensure security of resources: • Ensuring the accuracy of the disbursement voucher helps protect excess payments of the cash resource.

One-for-one checking of the receiving report and the invoice — This would prevent paying for goods that were not received. • One-for-one checking of the receiving report and the purchase order — This prevents accepting goods that were not ordered. • One-for-one checking of the purchase order and the vendor invoice — This prevents paying other than negotiated price. • File completed receiving report in receiving — This will provide an audit trail to document goods received and forwarded to the storeroom. • Authorize payments independently — Accounts payable should be provided with a copy of the purchase order, and should not authorize a payment without a PO. If they do that, the second or duplicate invoice would have been discovered because there would not have been a purchase order to match to the invoice. • Periodically confirm open payables — The balances in the accounts payable accounts should be reconciled with the vendors and then agreed to the general ledger. This will detect any discrepancies.