Download

1 / 10

100 likes | 400 Views

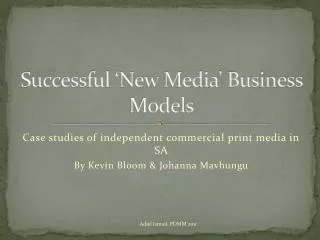

Enabling new business models. Ahmed Guetari CTO, Service Providers EMEA. Juniper Networks Barcelona, Nov 22 nd 2010. 5. customer economic business model. Worldwide internet traffic, 1990-2020 PB/month. # of Connections. Machine To Machine?. 180,000 160,000 140,000 120,000

E N D

Enabling new business models Ahmed Guetari CTO, Service Providers EMEA. Juniper Networks Barcelona, Nov 22nd 2010

5 customer economic business model Worldwide internet traffic, 1990-2020 PB/month # of Connections Machine ToMachine? 180,000 160,000 140,000 120,000 100,000 80,000 60,000 40,000 20,000 Forecast Model +27% 2008-2020CAGR 17x Growth2008-2020 +32% Video WWW is born Digital decade +20% Non-video 1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2021 Source: Juniper, Cisco, MINTS

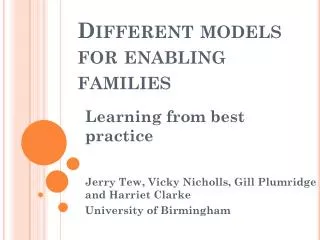

Working together on customer economic business Worldwide service provider revenue vs. investments with innovation, 2003-2009 $ in USD Billion Worldwide service provider revenue vs. investments with innovation, 2003-2020 $ in USD Billion $1,500 Forecast Model $500 $1,250 $400 $1,000 Revenue $750 $300 $500 Investment $200 $250 $100 2003 2003 2005 2004 2007 2005 2009 2011 2006 2013 2007 2015 2008 2017 2009 2019 Historical Revenue from Internet Historical Investment in Internet Forecasted Revenue from Internet Forecasted Investment in Internet Source: Juniper, Cisco, MINTS, Infonetics

WHAT’S AT STAKE:Service Provider Relevance to Customer • New Services: • Home networking • Video streamingand download • Targeted onlinead revenue • CDN • Managed telepresence • Cloud computing, PaaS, SaaS • Mobile advertising • Network outsourcing • Mobile BB access Service Transformation ~ $1T

WHAT’S AT STAKE:Service Provider Relevance to Customer • New Services: • Home networking • Video streamingand download • Targeted onlinead revenue • CDN • Managed telepresence • Cloud computing, PaaS, SaaS • Mobile advertising • Network outsourcing • Mobile BB access Service Transformation ~ $1T

WHAT’S AT STAKE:Service Provider Relevance to Customer Today’s Legacy Networks Today’s Legacy Networks Wireline Voice Wireline Voice Fixed BB Fixed BB Business Data Business Data Existing Mobile Data Services Existing Mobile Data Services Digital TV Digital TV Mobile Voice Mobile Voice

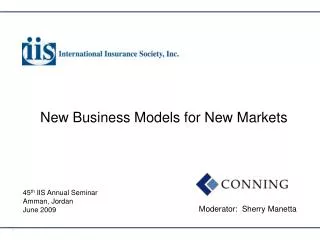

WHAT’S AT STAKE:Service Provider Relevance to Customer NetworkTransformation Discrete Nets to Unified IP Net Service & Software Ecosystem Today’s Legacy Networks Today’s Legacy Networks Developer Community Content/Apps Devices Wireline Voice Wireline Voice Fixed BB Fixed BB Business Data Business Data Existing Mobile Data Services Existing Mobile Data Services Digital TV Digital TV Mobile Voice Mobile Voice “The New Network” Subscriber Management Policy & Security Access/Transport Fabric

… While potentially reducing network service provider incentives and increasing consumer costs Implications for service providers Impact Rationale • Reduced incentive for network providers to invest in their networks beyond a maintenance level • Before network providers reach the point that they decide about the future of offering non-transport services, they may simply dramatically reduce network investment down to maintenance levels as retaliation to Regulator’s non discrimination rule • However, network providers may not be able to stop investing due to competitive dynamics Investment incentive • Network providers may exit non-transport services market • If the regulator does not impose structural or operational separation but does implement the non-discrimination rule, network providers will be forced to ask themselves whether they want to compete in the non-transport services market if they cannot gain competitive advantages over their competition Business model Implications for consumers • Shift of costs from content/application/service providers to consumers • In the spirit of ensuring a level-playing field between content, application , and service providers, Regulator is proposing that costs be shifted from content, application and service providers to consumers, whenever enhanced capabilities, such as guaranteed bandwidth and quality, are required to support a service • This is to prevent a large content company entering into private arrangements with network providers that leads to a barrier to entry that cannot be overcome by potential smaller content competitors Costs • More information about network management practices from providers • The Regulator believes that consumers would be empowered to make better decisions if they had more information about how network providers are managing services Information Source: Juniper Network Neutrality White Paper

Specific recommendations Content, application, and device discrimination Quality of experience discrimination Service information Service tiers