Download

1 / 8

80 likes | 98 Views

Explore how the specialty contractors industry was impacted by the consolidation frenzy in the late 90s and the evolution of M&A strategies. Gain insights into market trends and growth opportunities for construction and engineering companies.

E N D

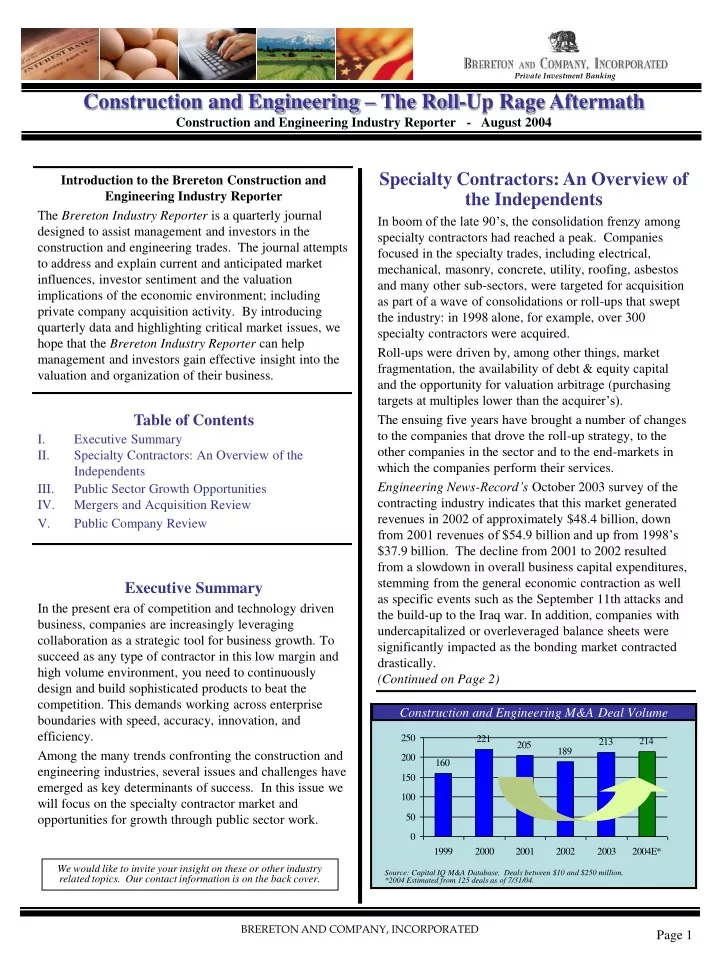

Private Investment Banking Construction and Engineering – The Roll-Up Rage AftermathConstruction and Engineering Industry Reporter - August 2004 Specialty Contractors: An Overview of the Independents In boom of the late 90’s, the consolidation frenzy among specialty contractors had reached a peak. Companies focused in the specialty trades, including electrical, mechanical, masonry, concrete, utility, roofing, asbestos and many other sub-sectors, were targeted for acquisition as part of a wave of consolidations or roll-ups that swept the industry: in 1998 alone, for example, over 300 specialty contractors were acquired. Roll-ups were driven by, among other things, market fragmentation, the availability of debt & equity capital and the opportunity for valuation arbitrage (purchasing targets at multiples lower than the acquirer’s). The ensuing five years have brought a number of changes to the companies that drove the roll-up strategy, to the other companies in the sector and to the end-markets in which the companies perform their services. Engineering News-Record’s October 2003 survey of the contracting industry indicates that this market generated revenues in 2002 of approximately $48.4 billion, down from 2001 revenues of $54.9 billion and up from 1998’s $37.9 billion. The decline from 2001 to 2002 resulted from a slowdown in overall business capital expenditures, stemming from the general economic contraction as well as specific events such as the September 11th attacks and the build-up to the Iraq war. In addition, companies with undercapitalized or overleveraged balance sheets were significantly impacted as the bonding market contracted drastically.(Continued on Page 2) Introduction to the Brereton Construction and Engineering Industry Reporter The Brereton Industry Reporter is a quarterly journal designed to assist management and investors in the construction and engineering trades. The journal attempts to address and explain current and anticipated market influences, investor sentiment and the valuation implications of the economic environment; including private company acquisition activity. By introducing quarterly data and highlighting critical market issues, we hope that the Brereton Industry Reporter can help management and investors gain effective insight into the valuation and organization of their business. Table of Contents I. Executive SummaryII. Specialty Contractors: An Overview of the Independents III. Public Sector Growth OpportunitiesIV. Mergers and Acquisition ReviewV. Public Company Review Executive Summary In the present era of competition and technology driven business, companies are increasingly leveraging collaboration as a strategic tool for business growth. To succeed as any type of contractor in this low margin and high volume environment, you need to continuously design and build sophisticated products to beat the competition. This demands working across enterprise boundaries with speed, accuracy, innovation, and efficiency. Among the many trends confronting the construction and engineering industries, several issues and challenges have emerged as key determinants of success. In this issue we will focus on the specialty contractor market and opportunities for growth through public sector work. Construction and Engineering M&A Deal Volume We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. Source: Capital IQ M&A Database. Deals between $10 and $250 million.*2004 Estimated from 125 deals as of 7/31/04. BRERETON AND COMPANY, INCORPORATED Page 1

Private Investment Banking Specialty Contractors: An Overview of the Independents (Continued) Again, using ENR Magazines’ classifications, building represents the bulk of activity, while the specialty markets are evenly distributed. Market Analysis Specialties While all of the trades have been impacted by the U.S. economic contraction, some end-markets declined more precipitously than others. M&A in the Specialty Contractor Market Today, buyers and sellers of specialty contractors approach M&A differently than they did five years ago. In particular: • Few, if any, companies believe that a quick “roll-up to go-public” strategy is feasible • While 12 E&C companies went public from 1997 to 2000, no E&C company has gone public since 2000 • Private equity funds investing in the sector appear to be purchasing companies with reasonable amounts of leverage and pursuing a more patient “buy and hold” strategy once they’ve acquired the companies • Buyers are focused on expanding into particular geographies or end-markets, not just acquiring loosely related companies for the sake of growth. Particularly favored sub-sectors include: • Advanced technology; Education; Healthcare; Homeland security: Water/wastewater expertise • Few companies in today’s market are taking on significant amounts of leverage • In many industries, lenders are increasingly raising the multiples at which they are willing to lend against EBITDA • In the contracting space, however, the lack of a significant asset base and the uncertainty of the percent of completion method of accounting cause many lenders to avoid the space or to cap the amount of leverage any company can carry • The median leverage of the specialty contractor tracked in this article is 2.2x Debt/EBITDA, which conforms favorably with the overall market • Companies are acquiring larger, fewer targets rather than a large volume of small companies • The transaction costs of accomplishing multiple acquisitions (including the time and expense involved in finding targets, conducting due diligence, executing the transaction documents and paying the professional fees) and the difficulties of the “blocking and tackling” of integration and establishing a cohesive management structure raise significant hurdles to acquiring many companies as part of one transaction Conclusion Companies throughout the contracting sector always struggle with finding the means to grow consistently through organic growth alone. For these companies, mergers & acquisitions have provided an alternative, faster means of achieving their revenue and value growth strategies but these transactions almost always involve a higher level of risk. M&A in the specialty contractor sector, in particular, has been associated since the late 1990s with roll-ups, leverage, difficult end-markets and unfulfilled promise. However, in 2004, improving economic conditions, smarter acquisition strategies and stronger balance sheets indicate that M&A in the specialty contractor service is worth considering. Construction and Engineering Industry Reporter - August 2004 We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED Page 2

Private Investment Banking Public Sector Growth Opportunities Many engineering and construction companies have actively diversified into less cyclical businesses to decrease exposure to under performing industries and create more even revenue streams. Many markets once rife with activity, such as industrial, commercial and power, have recently stalled for various reasons. Construction firms have instead begun to favor more stable sources of growth, namely the federal services market and work associated with federal regulatory changes. Growth drivers for public sector projects include growing populations, aging infrastructure, increased public funding, environmental regulations, privatization of infrastructure and homeland security. In this section we will provide an overview of the federal services market and reasons for its growing prominence in the revenue mix of contractor companies. The Federal Services Market Despite the widely known federal budget deficit issues, the federal services market, consisting of projects for the federal government and agencies and state & local governments, is one of the most robust sectors today for the construction industry. The annual budget for public sector work is about $200 billion, 25% of the $800 billion domestic construction industry. In 2003 and 2004, increased federal spending on defense and homeland security has generated the most revenue growth. Forecasts indicate that these budgets will continue to grow over the next few years. The public sector has historically been one of the most stable clients, but recent increases in the spending of these departments have led to the rapidly growing government portion of construction companies' businesses. The Department of Defense ("DoD") and the Department of Homeland Security ("DHS") are expected to continue spending at record levels fueled by residual effects from the Iraq war, opportunities to outsource federal jobs to civilians, and continued concerns about homeland safety. The Department of Energy ("DoE") will also be a significant contributor of funds to the industry. Agency WorkDoD contracts include the building of missile sites, outsourcing of base operations, maintenance of space facilities and building nuclear and biological detection and protection systems. The DoD's forecasted 2004 budget is about $380 billion. DHS contracts include the review of transportation infrastructure, review of emergency response centers, building facilities for natural disasters, and FEMA work for disaster recovery. The DHS 2003 budget was $33.4 billion, with an additional $6.7 billion in supplemental funding recently approved. The department's 2004 spending levels are forecasted to increase to approximately $41 billion. DoE contracts include remediation work, air and water quality and pollution prevention, as well as hazardous and nuclear waste cleanup and site closure. Federal OutsourcingAs the federal government looks to save money through cost-cutting measures and as more of the federal workforce becomes eligible for retirement, federal outsourcing represents a strong opportunity for the industry. Examples include: • DoD currently outsources more than 700,000 jobs. Construction and Engineering Industry Reporter - August 2004 We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED Page 3

Private Investment Banking Public Sector Growth Opportunities (Continued) Federal Outsourcing (Continued) • The Federal Activities Inventory Reform Act (FAIR) of 1998 states government intention to outsource an additional 125,000 non-DoD and DoD civil service jobs by end of 2004 and a total of 850,000 over the next 8-10 years. • The proposed Defense Transformation Act for the 21st Century of 2003, authorizing the use of civilians for non-combat military jobs, could convert another 320,000 military positions. The Environment Regulatory provisions also generate significant opportunities in the environmental and water sectors: • The Environmental Protection Agency ("EPA") has mandated the compliance of sulfur levels in diesel by mid-2006, with more stringent standards to come by 2010. • Sulfer compliance represents a $17 billion market opportunity for C&E companies, according to estimates from the National Petroleum Council. • Although the latest information is not yet available, ConocoPhillips and ExxonMobil, the two largest U.S. refiners, expected their clean fuels capital expenditures to more than double in 2003 over 2002. Their total clean fuels investment is projected to reach $4.5 billion in total. • New Maximum Achievable Control Technology ("MACT") standards set the emissions levels for specific sources of pollution, such as oil refineries, chemical plants and steel mills. • The EPA has issued more than 50 MACT standards over the past 13 years. In August 2003, 13 new MACT standards were issued for iron and steel foundries, combustion turbines, metal parts and products, and coating companies. • Estimated annual costs (excluding initial capital costs) are $350 million. These EPA estimates tend to be much lower than reality. Transportation • Transportation Equity Act for the 21st Century ("TEA-21") authorizes the federal surface transportation programs for highways, highway safety and transit. • This infrastructure project will provide $218 billion of funding. • Between 1998 and 2003, $170 billon of these funds were utilized for highway and transit state matching funds. Public Sector M&A OpportunitiesBecause entering a new industry segment through organic growth takes time and may lead to unanticipated results, Construction and Engineering firms have been using acquisitions as a means of expanding their presence in or accessing the public sector and other public sector activity. Because of the continued difference in margins (as illustrated below), publicly held government service (“GS”) companies have typically traded at higher multiples than their open market (“OM”) counterparts. In 2003, the median margin for OM firms was around 3.6%, while the median margin for GS firms was closer to 9.4%. From a transaction multiples perspective, in 2003, the median EV/EBITDA multiple for GS firms has increased to 8.9x and the multiple for OM firms has decreased to 7.4x. Conclusions Although there is a risk that a new administration might cut federal spending or slow the projected government outsourcing trends, public sector contracts remain a critical driver for current and future revenue growth in the C&E industry. C&E firms have been pursuing growth strategies with an aim toward diversification in their mix of end markets, client base and geography. Getting new, or greater, exposure to the public sector is a critical driver of this initiative. Given their healthy balance sheets and favorable valuations, many C&E firms could continue their proactive diversification efforts by seeking to acquire assets with exposure to federal services revenue streams, or to merge with government services-related firms. Construction and Engineering Industry Reporter - August 2004 Note: GS companies include Affiliated Comp Services, American Management Systems, Anteon International, Bearingpoint CACI International, CDI Corp., Computer, Sciences Corp., DigitalNet Holdings, Dynamics Research, Electronic Data Systems, GTSI Corp., Halifax Corp., Keane Inc., ManTech International, Maximus Inc., MTC Technologies, PEC Solutions, Perot Systems, SI International, SRA International, Tier Technologies, Titan Corp., Tyler Technologies and VSE Corp. We would like to invite your insight on these or other industry related topics. Our contact information is on the back cover. BRERETON AND COMPANY, INCORPORATED Page 3

Private Investment Banking Merger and Acquisitions Review The worldwide construction and engineering market rebounded in 2003 and early 2004, as the general economy experienced a broad-based recovery. As seen on page one, 2003 and the first half of 2004 has been a very active time for construction and engineering firms in terms of mergers and acquisitions (“M&A”) activity. However, it should be noted that while there are more deals getting done, they are generally smaller transactions. Factors Affecting Activity There are several factors that may assist in the resurgence of deal activity within the sector. Some of these factors include: Rebounding Credit Market The credit markets remain tight, but they appear to have bottomed out, as average total debt/EBITDA leverage ratios in transactions rose to 4.0x in 2003. Acquisition financing continues to be predominantly through asset-backed loans as a majority of the debt component, however recently lenders are showing increasing support for cash flow lending, which should help stimulate deal activity. Increased Activity from Private Equity Groups Despite a decline in fundraising in 2003, analysts confirm that there is no shortage of capital in the hands of private equity groups, who still have an estimated $100 billion, raised during the golden fundraising years of 1998–2001, to invest. In fact, the abundance of uncommitted capital has become an issue for private equity firms, many of which are behind their forecast investment pace. As a result, they are scrambling to make investments in quality companies. Private Equity Groups are actively looking for attractive construction and engineering companies with stable cash flows to invest in. This is exemplified by the recent barrage of deal activity. Increase in Offer Multiples Not only have the number of middle-market deals increased, but offer multiples have risen as well. In 2003, the International Mergers and Acquisition Partners (IMAP) reported a jump of over 20% in EBIT multiples. Construction and Engineering Industry Reporter - August 2004 • Multiples of Earnings Before Interest and Taxes (EBIT) were used in the comparisons above. EBIT was calculated using trailing 12 months earnings before interest and taxes, adjusted for non-recurring expenses and discretionary owner distributions including compensation in excess of market rates. Seller notes, etc., were discounted present values. Source: Loan Pricing Corporation (A Reuters Company)Transaction >$100 millionBorrower Revenues >$500 million BRERETON AND COMPANY, INCORPORATED Page 5

Private Investment Banking Merger and Acquisitions Review (Continued) Recent activity reflects the strong interest from both strategic and financial buyers. It should be noted that in the last twelve months, publicly traded construction and engineering firms have seen an approximate 20% increase in valuation, providing a more effective acquisition currency. Construction and Engineering Industry Reporter - August 2004 BRERETON AND COMPANY, INCORPORATED Page 6

Private Investment Banking Public Company Review While public company performance does not always translate perfectly into private company, middle-market trends, we have found it to be a useful reference for general trends. This page used the following public entities as a guide: Construction and Engineering Industry Reporter - August 2004 BRERETON AND COMPANY, INCORPORATED Page 6

Private Investment Banking Brereton and Company is a boutique investment bank dedicated to maximizing the value and liquidity of closely held businesses. Attention • Strategic and Financial advisors to businesses seeking value Maximization • Hands-on attention from experienced senior dealmakers who stay with your deal to closing • Founded in 1995 drawing from prior investment banking experience • Empathetic professionals who have acquired, operated and divested businesses for their own account • Broad industry experience in middle market Mergers & Acquisitions • Strategic planning framework for evaluation of financial alternatives • Structured timelines and processes for multiple bidder-based value maximization Expertise Process • If you are: • Undercapitalized and experiencing explosive demand for your product • Facing a difficult transition after many years at the helm • Unsure about how to best maximize the value of your business for your heirs • Ready to harvest your business investment to diversify your net worth • Please give us a call. Our initial discussions and analysis are strictly confidential and complimentary. Brereton and Company, Inc.1075 N. Tenth Street, Suite 110San Jose, CA 95112www.brereton.net Brandt Brereton, Managing Director E-Mail: brereton@brereton.netTelephone: (408) 938-9255 Facsimile: (408) 938-9259 Member: International Network of Mergers and Acquisitions Partners (www.imap.com) BRERETON AND COMPANY, INCORPORATED Page 8