Download

1 / 7

70 likes | 227 Views

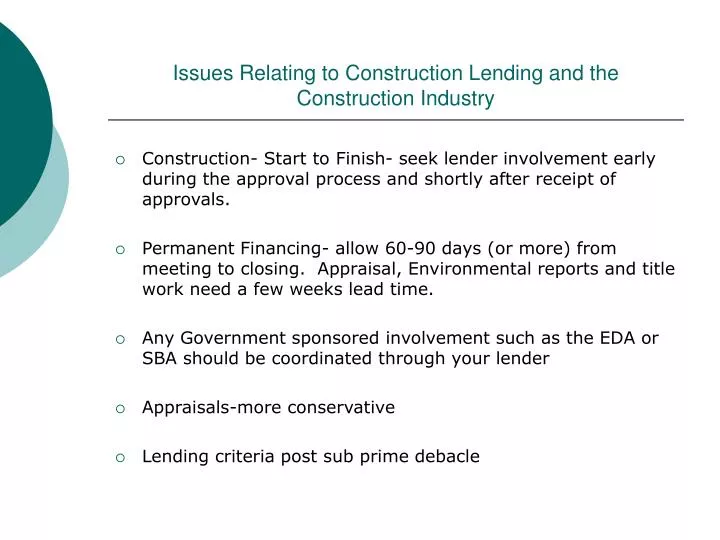

Issues Relating to Construction Lending and the Construction Industry. Construction- Start to Finish- seek lender involvement early during the approval process and shortly after receipt of approvals.

E N D

Issues Relating to Construction Lending and the Construction Industry • Construction- Start to Finish- seek lender involvement early during the approval process and shortly after receipt of approvals. • Permanent Financing- allow 60-90 days (or more) from meeting to closing. Appraisal, Environmental reports and title work need a few weeks lead time. • Any Government sponsored involvement such as the EDA or SBA should be coordinated through your lender • Appraisals-more conservative • Lending criteria post sub prime debacle

Lending to Contractors- Specialized Field • Some Lenders will not entertain lending to this specialized field. • Lending to some specialties and not others.

Choosing a Bank • Questions to ASK! • What is your legal lending limit? • What is your ‘hold’ or limit? • Prohibition on certain industries or groups. i.e. road building contractors, bridge or dam builders etc. • What is the approval process? Is it a signature process or committee process? Usually driven by the loan amount.

Loan Structure • Collateral- business assets, lien on real estate. • Cash Flow- debt service coverage. • Conditions • Capacity- ability to service the debt. Previous history and proforma cash flow. • Character- most important in some lenders eyes.

Specialized Criteria for Lending to Contractors • Stricter covenant criteria. • A/R to A/P ratio: Minimum: 1.5X--Like to see: 2.0X to 2.5X • Debt to Worth: Minimum: 2.0X—Like to see: 1.5X to 2.0X • Current Ratio Minimum: 1.0—Like to see: 1.20 to 1.0 or better • Cash to Total Assets: Like to see: 5% to 7% • EBIT/Interest Expense: Like to see: 3.0X to 8.0X

Financial Reporting: • An accurate and timely reporting of financial information is crucial to a successful borrowing relationship.

Reporting for Working Capital Lines of Credit: • FYE- audited are preferred for credits in excess of $5 million. • Reviewed FYE with disclosures. Within 120 days of FYE. • Semi Annual Statements- compiled or reviewed with disclosures. Can be negotiated. • Quarterly financial statements – company or mgmt prepared. • A/R and A/P agings- quarterly. • Contract Status Report – quarterly.