Download

1 / 9

90 likes | 109 Views

Explore potential outcomes in plant destruction, Force Majeure events, insolvency, law changes, environmental risks, and more. Mitigants & conclusions provided.

E N D

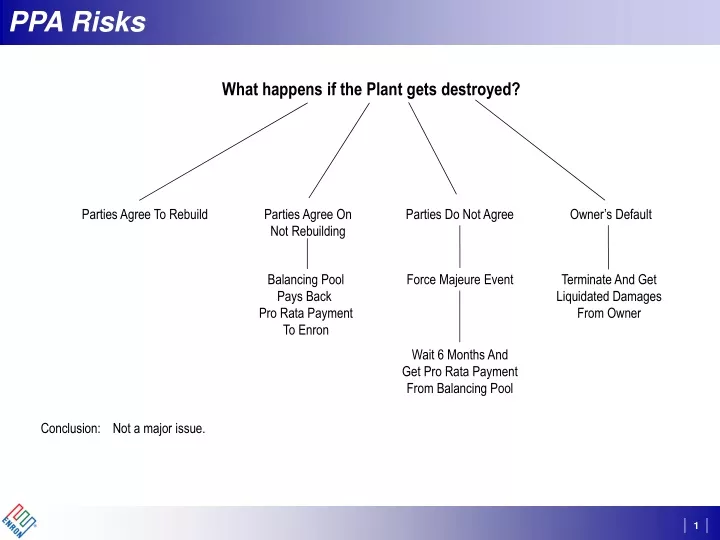

PPA Risks What happens if the Plant gets destroyed? Parties Agree To Rebuild Parties Agree OnNot Rebuilding Parties Do Not Agree Owner’s Default Balancing PoolPays Back Pro Rata PaymentTo Enron Force Majeure Event Terminate And GetLiquidated DamagesFrom Owner Wait 6 Months AndGet Pro Rata PaymentFrom Balancing Pool Conclusion: Not a major issue.

PPA Risks What happens under a Force Majeure event? Less Than 6 Months More Than 6 Months Termination At Our Option Enron Will Not MakeCapacity or Energy Payments/Owners Do Not PayPenalties Balancing PoolPays OwnersCapacity Payments Pro Rata PaymentPaid Back FromBalancing Pool Comment: We get hurt under Short Term Force Majeure because we do not get a pro rata share of our up-front payment back. Balancing Pool also gets hurt during Force Majeure and thus their interests are aligned with ours. Mitigant: PPA’s call for the Owners to mitigate Force Majeure, and obligate Owner to operate at “Good Operating Standard” and to do all things necessary to ensure continuous availability. Government will not accept the owner abusing Force Majeure. Market surveillance regulators would become involved. Conclusion: Acceptable risk given the expected value.

PPA Risks What happens in insolvency? Enron makes determination Not terminate Terminate Argue that the PPA’s continue tobe attached to the assets Recourse to Ownernot Balancing Pool Liquidated damages Positive damages Negative damages • It is our legal opinion that the Trustee does not likely have the right to terminate a provincial regulation that is binding the plant. Unsecured claimsunder bankruptcy Enron pays nothing Conclusion: best case however highly unlikely Conclusion: worst case scenario Mitigant: “not terminate scenario”

The asset has an out of the money obligation attached to it (the PPA). PPA’s are a form of regulation that arguably cannot be terminated in bankruptcy. This could have occurred under current environment and it is assessed that it would not have been allowed. The PPA process will lead to the Owner getting a better rate of return than they get in the current environment. Owners get the plants back after the term of the PPA. Owners profit from excess energy that they produce and additional capacity that they bring on. Government would discourage the owner from negatively affecting the PPA process. Owner may not retain the assets after the bankruptcy process. (We would be a significant unsecured creditor with a substantial say in the insolvency outcome.) Owner would have to give up any positive equity value to attempt this strategy. There is a regulatory process that we could utilize to try to prevent them from moving the assets into a less credit worthy entity. PPA Risks Does the Owner have an incentive to move the Unitinto a highly leveraged subsidiary and ultimately move the asset into bankruptcy? Yes No Conclusion: Acceptable risk.

PPA Risks What about change in law? We are exposed to change of law risk(most applicable to environmental laws (Kyoto Accord) andpermit renewals - see next page) We can walk away from the PPA if a change in law renders it“unprofitable”, however, we walk away from our up-front payment. Conclusion: This risk is acceptable due to the high expected value of the deal and the fact that we are dealing with in a stable,pro-business and democratic province. Also a change in law that affects all coal plants in Alberta would ultimately affect the price of power in Alberta (Alberta generation is 75% baseload coal).

PPA Risks What about Environmental Risks? (Enron is not directly liable for Environmental claims due to owning PPA’s - only exposed to increased cost due to change in law) External consultant has confirmed that the units are currently in compliance The fixed cost structure has budgeted capital costs that includeforeseeable environmental permit requirements. Any future changes in environmental laws have not been budgeted. Conclusion: Could be significant issue in the future. Acceptable risk given value of deal and the option to walk away from PPA.

PPA Risks What happens if Owner exceeds Target Availability? Enron gets pool price and paysowner 30 day average price(peak or off peak) Enron pays fixed capacity paymentsbased on target availability Conclusion: Not Material

PPA Risks What if the Owner does not meet the Target Availability? Owner pays Enron penalty that equals 30 day rollingaverage Pool Price (Peak or Off Peak) on short amount. We pay Capacity Payment on Target Availability. Mitigants: Do not sell long term firm power against this contract. Link the risks that we have to any hedge. Conclusion: Minor issue relative to value of deal.

PPA Risks Do the Owners have an incentive to have low prices in Alberta? TransAlta: The Units we are bidding on are all owned by TransAlta TransAlta has no load after the auction and they own several unregulated gas units Conclusion: TransAlta’s incentives are aligned with ours.