Download

1 / 25

250 likes | 371 Views

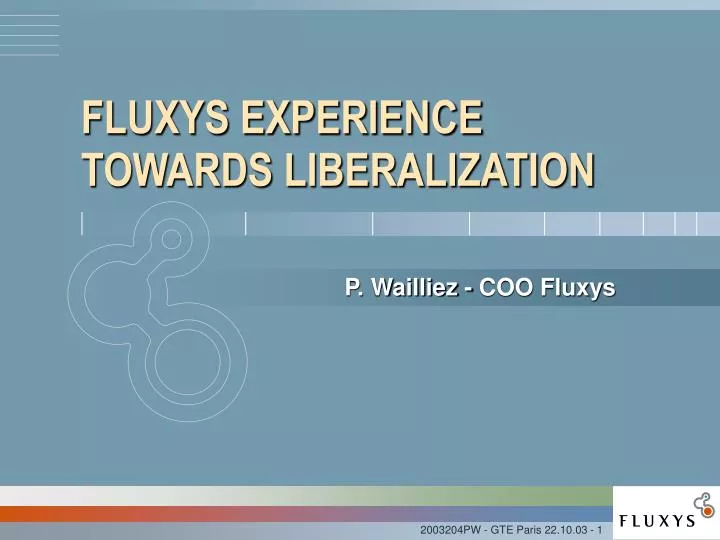

FLUXYS EXPERIENCE TOWARDS LIBERALIZATION. P. Wailliez - COO Fluxys. A strong acceleration. %. 100. 90. 2010. 2006. 2002 FL Gas. 07/2003. 80. Decree. 70. 2001 B Gas Law. 60. 50. 1999 B Gas Law. 40. 30. 20. 1998 EU GAS. 10. Directive. 0. 2000. 2001. 2002. 2003. 2004.

E N D

FLUXYS EXPERIENCE TOWARDS LIBERALIZATION P. Wailliez - COO Fluxys

A strong acceleration % 100 90 2010 2006 2002 FL Gas 07/2003 80 Decree 70 2001 B Gas Law 60 50 1999 B Gas Law 40 30 20 1998 EU GAS 10 Directive 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 MARKET OPENING IN BELGIUM: a unique example in Europe Less than 6 months between decision& implementation

TOWARDS MORE COMPLEXITY / UNCERTAINTY • Regulation • Actors • Market and Network • Costs

TOWARDS MORE COMPLEXITY / UNCERTAINTYRegulation BEFORE • Clear Objectives • Infrastructures enablingGas Market Development • Continuity of Supply • Safety

TOWARDS MORE COMPLEXITY / UNCERTAINTY Regulation NOW • Same clear objectives but • Regulators at Federal& Regional level in Belgium • Risk of regulatory pancaking • Important impact on: • Value creation • Complexity(potential dis-optimization)

TOWARDS MORE COMPLEXITY / UNCERTAINTY Regulation THEREFORE • Take initiative • Unbundling • Publishing Tariffs • Coordinate modalitiesof opening with Distributors.

TOWARDS MORE COMPLEXITY / UNCERTAINTYActors BEFORE • Integration • Non-detrimental Decisions for Transport(molecule decisions taking into account network integrity)

TOWARDS MORE COMPLEXITY / UNCERTAINTYActors NOW • Transport not underthe umbrella of incumbent(incumbent decisions not granted) • Revenues(tariff hypothesis <> reality) • Continuity of Supply(network integrity <> portfolio optimization)

TOWARDS MORE COMPLEXITY / UNCERTAINTYActors THEREFORE • Anticipate shippers Behavior & Needs • Careful design of Access Rules.

TOWARDS MORE COMPLEXITY / UNCERTAINTYMarket and Network BEFORE • Long-term contracts& Easy forecasts • Infrastructure Developed around Contracts

TOWARDS MORE COMPLEXITY / UNCERTAINTYMarket and Network NOW • Shorter Terms& Uncertainties • Infrastructure Projectsnot tied to Molecule

TOWARDS MORE COMPLEXITY / UNCERTAINTYMarket and Network THEREFORE Develop • Performant Forecasting Tools • Probabilistic above Deterministic Approach.

TOWARDS MORE COMPLEXITY / UNCERTAINTYCosts BEFORE • Transport costs includedin Commercial Margins

TOWARDS MORE COMPLEXITY / UNCERTAINTYCosts NOW • Revenues models not always favouring an Entrepreneurial Behaviour • Deregulation <> Optimisation

TOWARDS MORE COMPLEXITY / UNCERTAINTYCosts THEREFORE Further develop • Cost Consciousness • Customer-mind and Innovations

Be Proactive & Innovative! TOWARDS MORE COMPLEXITY / UNCERTAINTY Regulation - Actors - Market and Network - Costs One Example: Hub in Zeebrugge (and this happened before Liberalization)

NORWEGIANGAS FIELDS UNITEDKINGDOM Transco Ruhrgas Wingas SPAIN SWITZERLAND ITALY SWITZERLAND ITALY EASTERN COUNTRIES NETHERLANDS Zebra GTS OVERSEASLNG sources HUB Gaz de France Fluxys launched in 98-99the Zeebrugge Hub GERMANY FRANCE Soteg LUXEMBURG

Net Churning = 3 9 ZEEBRUGGE HUB: LIQUIDITY 2003 1999 2000 2001 2002 TJ/day 55 Customers OUT IN Market Evolution (// UK) Gross Traded Volumes (*) up to 15 106 m³(n) / h [6 x Transport Capacity between UK & Continental Europe] [3 x Belgian Peak Consumption] 5 Customers (*) estimated

Spread Trading HUB CONTRIBUTION TO AN EFFICIENT GAS MARKET • Opportunities for optimizing Gas Supply Portfolio through Arbitrage • Location (Zeebrugge « Bacton) • Spot / Long Term • Spark (Gas « Electricity) • LNG / Pipeline Gas

Nov ‘ 98 Start Interconnector ZEEBRUGGE HUB: ARBITRAGE OPPORTUNITIES Source: The Heren Report (ESGM) & Distrigas

SummerSurplus WinterShortage ZEEBRUGGE HUB: THE UK BEHAVIOUR TJ/month Net Seller IN OUT

Sellingin the Winter Buyingin the Summer ZEEBRUGGE HUB: ANOTHER BEHAVIOUR TJ/month Net Buyer IN OUT

Be Proactive & Innovative! TOWARDS MORE COMPLEXITY / UNCERTAINTY Regulation - Actors - Market and Network - Costs One Example: Hub in Zeebrugge (and this happened before Liberalization) One Example: Hub in Zeebrugge (and this happened before Liberalization) (would have this happened after Liberalization ?)

Liberalization: Fluxys experience CommunicationFlows ? ? HUB IN EUROPE : WHAT’S NEXT? Criteria: • Interconnected Grid • Access to Sources • Flexible & Willing Operator • Market Driven Generation A new Challenge : Harmonization of Business Practices for [multi-] Hubs Trading (EU Standard) & avoid Temptation of sub-Regional Behaviours