Download

1 / 15

160 likes | 356 Views

The Black-Scholes Model for Option Pricing. -Meeting-2, 09-05-2007. Introduction. Reference:. Computational Methods for Option Pricing Yves Achdou and Olivier Pironneau SIAM, 2005. Option Pricing: Recap. Types. European American Asian Vanilla & Exotic. Vanilla European Model.

E N D

The Black-Scholes Modelfor Option Pricing -Meeting-2, 09-05-2007

Reference: • Computational Methods for Option Pricing • Yves Achdou and Olivier Pironneau • SIAM, 2005

Types • European • American • Asian • Vanilla & Exotic

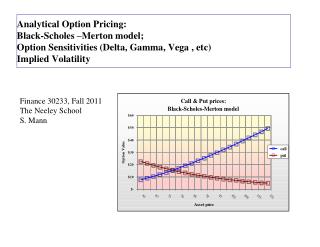

Vanilla European Model Contract that gives the owner a right to buy a fixed number of shares of a specific common stock at a fixed price at a certain date. • SorSt : Spot price (price of the asset) • K: Strike or exercise price • T: expiry or maturity date • Ct: Price of the Call option • Pt: Price of the Put option

Problem Statement • An Option has a value. • Is it possible to evaluate the market price Ct of the call option at time t, 0 t T ? • Assumptions: • No cost for transactions, • Transactions are instantaneous, • No arbitrage, and • Cannot make instantaneous benefits without taking any risks.

Pricing at Maturity • ST : Spot price at maturity • Value of the call at maturity:

Probability: Basics • : a set • A : a –algebra of subsets of • P : a nonnegative measure on such that: P()=1 The triple (,A,P) is called a probability space.

…. Probability: Basics • X : a real-valued random variable on (,A,P) is an A–measurable real-valued function on ; • For each Borel subset B on R: • Filtration : • Ft represents a certain past history available at time t.

The Black-Scholes Model • A continuous-time model involving a risky asset (St) and a risk-free asset (St0) • Evolution of risk-free asset is given by an ODE: r(t) is instantaneous rate If r is contant

… The Black-Scholes Model • Evolution of risky asset is a solution to the following stochastic DE • Deterministic term (drift): dt , where is an average rate of growth of the asset price, and • Random term that models variations in response to external effects.

… The Black-Scholes Model • Bt is a standard Brownian motion on a probability space (,A,P) • A real-valued continuous stochastic process whose increments are independent and stationary. • t : the volatility (assumed constant)

Pricing the Option • The Black-Scholes Formula: