Download

1 / 6

120 likes | 565 Views

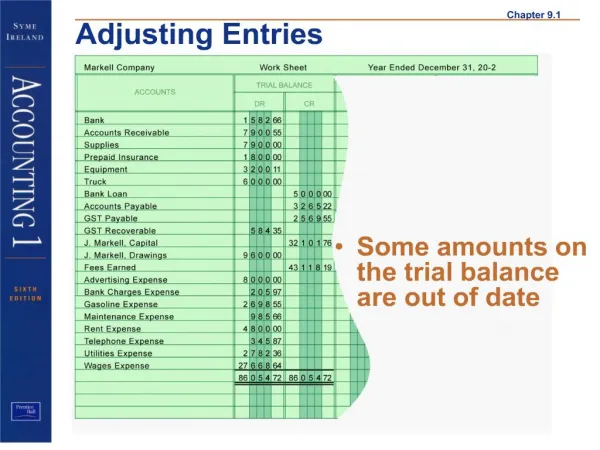

Chapter 4.4: Trial Balance. Bank Loan. 750. 2000. 1900. J. Yogi, Capital. Supplies. A/R. Cash. A/P. 850. 800. 900. Ledger. A “book” storing all accounts Total of all debit balance accounts equal total of all credit balance accounts. Methods of Taking Off a Trial Balance.

E N D

Bank Loan 750 2000 1900 J. Yogi, Capital Supplies A/R Cash A/P 850 800 900 Ledger • A “book” storing all accounts • Total of all debit balance accounts equal total of all credit balance accounts

Methods of Taking Off a Trial Balance • Step 1: List all the accounts and their balances. Leave room for a 3-line heading • Step 2: Place the debit balances in a debit balances in a debit column and credit balances in a credit column. • Step 3: Add up the two columns. • Step 4: See if the two columns are the same (balances). • Step 5: Write a heading on the top (Who, What, When)

Trial Balance • Checks accuracy of the ledger • Account balances may still be incorrect

Trial Balance Errors • If a ledger does not balance, follow these four steps: • 1. Re-add the trial balance accounts • 2. Check the figures from the ledger against those of the trial balance. Make sure none are missing or on the wrong side or for the wrong account. • 3. Recalculate the account balances. • 4. Check that there is a balanced accounting entry in the accounts for each transaction.

Trial Balance Errors • Find the difference between debits and credit totals • If 1, 10, 100, etc. may be adding error on trial balance or accounts • Check for difference in an account balance • Divide difference by 2, meaning an account balance on wrong side on trial balance • If difference is divisible by 9 with no remainder, transposition error made, e.g. 72 not 27 • Missing entry from journal to ledger • Re-check!