Download

1 / 13

390 likes | 965 Views

Chapter 6 The trial balance. Learning objectives. After you have studied this chapter, you should be able to: Prepare a trial balance from a set of accounts Explain why the debit and credit trial balance totals should equal one another. Learning objectives (Continued ).

E N D

Learning objectives After you have studied this chapter, you should be able to: Prepare a trial balance from a set of accounts Explain why the debit and credit trial balance totals should equal one another

Learning objectives (Continued) Explain why some of the possible errors that can be made when double entries are being entered in the accounts do not prevent the trial balance from ‘balancing’ Describe uses for a trial balance other than to check for double entry errors

Review of double entry bookkeeping For each debit entry there is a credit entry and for each credit entry there is a debit entry. The total of all the items recorded in all the accounts on the debit side should equal the total of all the items recorded on the credit side of the accounts. To check that there is a matching credit entry for every debit entry, we prepare a trial balance.

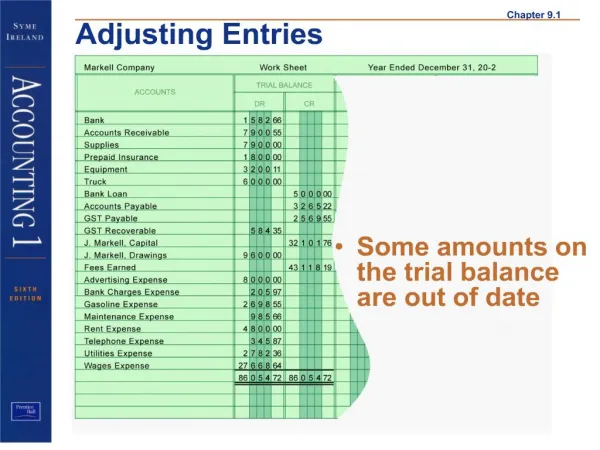

The trial balance The trial balance is a list of account balances arranged according to whether they are debit balances or credit balances.

Drawing up a trial balance The first stage is to balance each T-account.

Drawing up a trial balance (Continued) The second stage is to enter the account balances into the appropriate column.

Drawing up a trial balance (Continued) The trial balance always has the date of the last day of the accounting period to which it relates. It is a snapshot of the balances on the ledger accounts at that date. The totals of the two columns must always match. A trial balance can be drawn up at any time but it is normal practice to prepare one at the end of an accounting period before preparing an income statement and statement of financial position.

Trial balances and errors It is easy to assume that if the trial balance balances, the entries in the accounts must be correct. However, there are several types of error that will not affect the balancing of a trial balance. Errors that are revealed include: addition errors; using one figure for the debit entry and another for the credit entry; entering only one side of the transaction.

Inventory in the trial balance The closing inventory figure is not found in an account in the ledger and so does not appear in the trial balance. It is noted underneath the total figure and incorporated into the financial statements later. Opening inventory is recorded in a ledger account and so would be included in a trial balance prepared.

Learning outcomes You should have now learnt: How to prepare a trial balance That trial balances are one form of checking the accuracy of entries in the accounts That errors can be made in the entries to the accounts that will not be shown up by the trial balance That the trial balance is used as the basis for preparing income statements and statements of financial position