Download

1 / 14

230 likes | 601 Views

CHAPTER 5 Postings to ledger accounts and the trial balance. Learning outcome To be able to post journal entries for a double-entry system to the general ledger accounts to prepare a trial balance. 5- 1. KEY TERMS. Creditors Debtors Control accounts Rules of double entry Trial balance

E N D

CHAPTER 5 Postings to ledger accounts and the trial balance Learning outcome To be able to post journal entries for a double-entry system to the general ledger accounts to prepare a trial balance PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd 5-1

KEY TERMS • Creditors • Debtors • Control accounts • Rules of double entry • Trial balance • Errors in a trial balance PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

GENERAL LEDGER ACCOUNTS • Journal totals posted to ledgers to: • summarise information • classify information • Facilitates: • locating information • extracting information PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

TRANSACTION FLOWCHART Figure 5.1 Flowchart of transactions into accounting records PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

DOUBLE-ENTRY RULES DEBIT SIDE (DR) CREDIT SIDE (CR) ASSETS Increases Decreases EXPENSES Increases Decreases EQUITY Decreases Increases REVENUE Decreases Increases LIABILITIES Decreases Increases PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

DOUBLE-ENTRY RULEScont. Debit Credit ASSETS EXPENSES Increases Decreases Debit Credit EQUITY REVENUE LIABILITIES Decreases Increases PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

SUMMARY OF DOUBLE-ENTRY RULES • Account balance PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

DEBTORS CONTROL ACCOUNT PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

CREDITORS CONTROL ACCOUNT PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

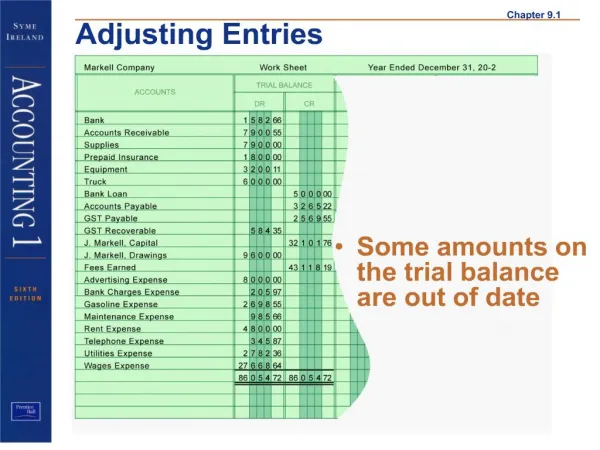

TRIAL BALANCE • Ensures ledgers are balanced • Every debit has a corresponding credit • Lists all general ledger accounts, with balances, in numerical order PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

TRIAL BALANCE cont. • Separate columns for debit balances and credit balances show if total debits equal total credits • Control accounts, not subsidiary accounts, appear in trial balance • ‘Nil’ balances usually not included PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

CHECKLIST FOR POSTING FROM JOURNALS TO LEDGER ACCOUNTS PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

CHECKLIST FOR POSTING FROM JOURNALS TO LEDGER ACCOUNTS cont. PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd

CHECKLIST FOR POSTING FROM JOURNALS TO LEDGER ACCOUNTScont. PPTs to accompany Accounting and Bookkeeping Principles and Practice byAAT & David Willis 2011 McGraw-Hill Australia Pty Ltd