Download

1 / 29

290 likes | 387 Views

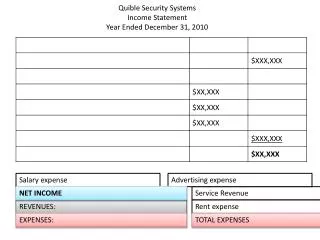

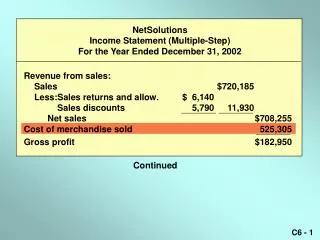

XYZ Credit Union Income Statement For the Year Ended December 31, 2010. Interest on Loans $ 900,000 Income on Investments 170,000 Total Interest Income 1,070,000 Dividends on Shares (200,000) Interest on Borrowed Funds -0-___

E N D

XYZ Credit UnionIncome StatementFor the Year Ended December 31, 2010 Interest on Loans $ 900,000 Income on Investments 170,000 Total Interest Income 1,070,000 Dividends on Shares (200,000) Interest on Borrowed Funds -0-___ Total Cost of Funds (200,000) Interest Margin 870,000 Fee Income 200,000 Other Income 75,000 Total Non–Interest Income 275,000 Expenses (see next slide) (1,065,000) Net Income $ 80,000

XYZ Credit UnionIncome StatementFor the Year Ended December 31, 2010 Comp & Benefits $ (360,000) salaries, insurance, payroll taxes Travel & Conf ( 10,000) volunteer & staff education Occupancy ( 60,000) rent, utilities, prop taxes, bldg depr. Operations (285,000) postage, telephone, ATM, debit Education & Promo ( 25,000) member education (marketing) Loan Servicing (150,000) credit reports, recording fees Prof Services ( 15,000) legal, audit Prov for Loan Losses ( 90,000) fund the allowance for loan losses Member Insurance ( 55,000) corp stabil, NCUSIF premium Operating / Supervision ( 5,000) regulators Other Expenses ( 10,000) annual mtg, association dues Total Operating Exp$ (1,065,000)

XYZ Credit UnionRatio AnalysisPower Ratios Net Worth Ratio Statutory Reserves + Undivided Earnings Total Assets 2,300,000 = 9.89% 23,250,000 Congress defined well capitalized as 7%. (can be higher for complex credit unions) 6% = adequately capitalized, 4% = undercapitalized. If you are undercapitalized you will need a capital restoration plan approved by the regulators. Net worth above 7% allows the credit union the ability to weather a storm. For example a bad recession. This is why I refer to it as a power ratio, it buys you time if you’re losing money, or allows you to grow.

XYZ Credit UnionRatio AnalysisPower Ratios Return on Assets Net Income Average Assets 80,000 = 0.34% 23,250,000 Net income must be annualized. If you are using income for the month multiply by 12 to annualize. Return on assets is a power ratio because earnings are the only way to increase net worth which allows a credit union to grow.

How these Power Ratios Work Together If the board wants to maintain capital and they want the credit union to grow, the return on assets ratio can tell us what our rate of growth should be. By moving the decimal to the right one place, the 0.34% return on assets becomes a growth rate of 3.4%. If the credit union grows faster than 3.4%, net worth will be depleted. The rule works in reverse. If the board sets an annual growth rate of 9%, the return on assets required can be calculated by moving the decimal to the left one place. The 9% growth rate equates to a required return on assets of 0.90% to maintain net worth.

Select Ratio Analysis Delinquency Ratio Delinquent Loans Total Loans 150,000 = 1.20% 12,500,000 Delinquent loans are calculated for the purpose of this ratio to include loans over 2 months delinquent. Caution should be used when making decisions based on this ratio. A credit union heavy in real estate loans may have low delinquency, but also may have a lower yield on loans. A small credit union can see this ratio move a lot from month to month because one or two members can cause the ratio to change dramatically.

Select Ratio Analysis Net Charge Off Ratio Charge offs – Recoveries Average Loans 100,000 = 0.80% 12,500,000 This ratio needs to be annualized. If XYZ Credit Union has a net charge off ratio of 0.80% and ABC Credit Union has a net charge off ratio of 0.20%, which credit union is doing a better job?

That was a trick question.The proper answer is that I did not give you enough information. Yield Net Net on Loans Charge offs Yield ABC CU 5.50% 0.20% 5.30% XYZ CU 7.20% 0.80% 6.40% From this example XYZ has four times the amount of charge offs, yet they still make more money on their loans. Why? ABC may have more A credit borrowers with lower rates and lower delinquency. ABC may have a different loan mix, heavy in real estate loans, whereas XYZ may be more of a consumer lender.

Select Ratio Analysis Loan to Share Ratio Total Loans Total Shares 12,500,000 = 60.24% 20,750,000 This ratio is especially important in a low interest rate environment. The peer is yielding 6.57% on its loan portfolio while yielding 1.85% on investments. This means that a loan generates 4.72% more interest. A 10% increase in XYZ Credit Union’s loan to share ratio equates to $2,075,000 in additional loans. This increases income by $97,940. Considering that XYZ’s net income for the year was $80,000, this increase is significant.

Select Ratio Analysis Operating Expense Ratio Operating Expenses975,000 = 4.19% Average Assets 23,250,000 Net Operating Expense Ratio Operating Expenses – Fee Income775,000 = 3.33% Average Assets 23,250,000 Operating expenses do not include dividends or provision for loan losses. This ratio must be annualized. I use the net operating expense ratio. I believe this to be a more fair comparison if comparing to other credit unions or the peer. The reason is that one credit union may have a service such as drafts, it is only fair to be able to reduce the expense by the income generated (NSFs).

Select Ratio Analysis Fixed Asset Ratio Fixed Assets Total Assets 800,000 = 3.44% 23,250,000 Credit Unions are generally limited to 5% of assets in fixed assets. 5% of XYZ Credit Union’s assets is equal to $1,162,500. This means XYZ is under the limit by $362,500. This can be helpful if the board is considering expansion.

Select Ratio Analysis Liquidity Ratio Cash + Investment under 1 year Total Assets 4,100,000 = 17.63% 23,250,000 State chartered credit unions must exceed 10%.

Select Ratio Analysis Productivity Ratios Assets 23,250,000 = $ 2,447,368 Full Time Equivalent Employees 9.5 Members 4,200 = 442 Full Time Equivalent Employees 9.5 Salary & Benefits 360,000 = $ 37,894 Full Time Equivalent Employees 9.5 Once again be careful with these ratios. There are several factors that could make these ratios not comparable. If a credit union has not purged membership or has a high number of $5 accounts, the number of members may be inflated. If a credit union has an employee that works 10 hours per week they are still counted as half an employee. A credit union with multiple locations may have a higher number of employees than a single location credit union.

Select Account DetailsLoans Common Types New Vehicle Used Vehicle 1st Mortgage 2nd Mortgage Home Equity Share Secured Other Secured Credit Card Commercial Open End – this means that the member has a limit that can be advanced. Credit cards and home equity loans are examples. The difference between the loan limit and the loan balance is a loan commitment. Closed End – this loan type has a specific end date.

Select Account DetailsLoans Common Risks Default risk – the risk that the member does not pay. Interest risk – the risk that a change in interest rates causes the loan to lose money in the future. The longer the term of the loan, the greater the risk. Example of interest rate risk. The credit union offers 30 year mortgages. The credit union decides that these loans are safe because they have had no mortgage loan losses. In 2010 XYZ Credit Union increased its 1st mortgage portfolio to $10,000,000. The credit union charges 5.50% on 1st mortgage loans. When subtracting 0.86% cost of dividends and 3.72% operating expenses the credit union nets 0.92% on these mortgage loans (good job).

Select Account DetailsLoans Now five years pass; and some things have changed, interest rates return to the 1970s rates. The mortgage loans are still yielding 5.50% since they were at a fixed rate. The credit union has done a great job of holding expenses at 3.72%. The cost of funds have gone up substantially because rates have gone up and the cost of dividends is now at 6%. A 1st mortgage in this market would be at 12%. Now when the 3.72% operating expenses and the 6.00% cost of funds are subtracted the net return is a negative 3.22%, not so good. Example of default risk changes. In 2005, 50% of the credit union’s loan portfolio consisted of vehicle loans, of these 80% were A paper. In 2010, 50% of the credit union’s loan portfolio was in vehicle loans, of these 30% were A paper. The C, D, and E paper went from 5% of the vehicle loans in 2005 to 50% of the vehicle loans in 2010. It is likely that the default risk went up even though the portfolio composition stayed the same.

Select Account DetailsAllowance for Loan Losses This account is used to fund the amount of time between when the adverse event occurs in a member’s life that puts collection of a loan in jeopardy and when a loss actually occurs. Since it is impractical for a credit union to evaluate each loan individually, the accounting standards allow for loans with similar characteristics to be pooled together to determine a loss rate for that pool. Generally the larger the credit union the more pools they will have. A small credit union may only have 2 pools secured loans and unsecured loans. In a large credit union indirect new vehicle loans granted with C paper may get their own pool. In addition to pooling individual classification is used for loans that are too unique to be pooled. Common examples of these are commercial loans or large real estate loans. The third component would be economic conditions. If the pooling method uses historical data for the past three years while the sponsor company’s employees are working overtime and now there are layoffs, historical data may not be enough. The Board should be careful. This account uses a great deal of estimation and management assertions. If examiners and auditors are repeatedly telling you that the account is underfunded that should be a red flag.

Select Account DetailsInvestments Common types. Certificates of Deposits Negotiable Certificates US Government and Federal Agency Securities Mortgage Backed Securities Classifications Hold to Maturity (ability and intent is not to sell) Available for Sale (may choose to sell for liquidity reasons) Trading (buy and sell regularly – rarely used) Accounting & Reporting Hold to Maturity – recorded at cost (market value on investment report) Available for Sale – recorded at market value on balance sheet Trading - recorded at market value on income statement also If your investments are recorded as hold to maturity, management should not be selling them.

Select Account DetailsInvestments Common risks. Default risk -- Most credit unions do not buy investments with high default risk. Interest rate risk -- Once again the longer the term the greater the interest rate risk. Although available for sale may appear to reduce some of this risk, be careful, the credit union may still be reluctant to recognize a loss on investments. Premiums are an adjustment of interest rate. If an investment has a coupon rate of 6%, but the current market rate for that term and level of risk is 4%, the seller will sell the investment at a premium. When the market is working properly the net of the coupon rate and the amortization of the premium (the yield) will equal the market rate (4%). Discounts are an adjustment of interest rate. If an investment has a coupon rate of 2%, but the current market rate for that term and level of risk is 4%, the seller will sell the investment at a discount. When the market is working properly the net of the coupon rate and the amortization of the discount (the yield) will equal the market rate (4%). Call dates are dates in the future, but before the maturity date, that a party to the investment can force an early maturity.

Select Account DetailsFixed Assets Common types. Land not depreciated Land improvements landscaping, parking lots Building Building improvements additions, remodeling Furniture desks Equipment data processing Fixed assets are depreciated because the property will last for several accounting periods, therefore the cost of the asset will be spread over the period of time that the credit union benefits from the asset. As noted earlier the amount of fixed assets should be below 5% of total assets. Periodic inventories should be done for two major reasons: The first reason is to determine that assets on the books are still being utilized by the credit union. The second is to determine that nobody has taken a credit union asset.

Select Account DetailsAssets Acquired in Liquidation Assets acquired in liquidation is the transfer of ownership of collateral from the member to the credit union. This is required for vehicles, but many credit unions ignored the requirement because it was immaterial to the financial statements and because of the short time between repossession and subsequent sale of the vehicle. The increase in foreclosures has caused credit unions to begin recording assets acquired in liquidation. Assets acquired in liquidation are carried on the balance sheet at the LOWER of cost or the fair market value less selling expenses. Example – XYZ Credit Union has a 1st mortgage on a home with a loan balance of $150,000. After meeting with a local realtor the fair value (selling price) was determined to be $100,000. Expected selling expenses are $5,000. The Credit Union will charge off $55,000 of the loan and transfer the remaining $95,000 to assets acquired in liquidation. The house is later sold for $85,000, the $10,000 loss is recorded as loss on sale of assets.

Complex Credit Unions Generally adequately capitalized credit unions have 6% of assets in net worth. An additional 1% of net worth increases the status to well capitalized (remember our power ratio). This is true for non-complex credit unions. A complex credit union has certain characteristics that requires additional net worth. Page 12 of the quarterly call report details the risk based net worth requirement to be considered adequately capitalized. The following are assets that require additional net worth: Long Term Real Estate Loans. The first 25% of assets in long term real estate loans require net worth of 6%. Any real estate loans above 25% of assets require net worth of 14%. Member Business Loans. The first 15% of assets in member business loans require net worth of 6%. The next 10% of assets in member business loans require net worth of 8%. Any business loans above 25% of assets require net worth of 14%. Long Term Investments. Investments maturing in under 1 year require net worth of 3%. Investments maturing in 1-3 years require net worth of 6%. Investments maturing in 4-10 years require net worth of 12%. Investments maturing in over 10 years require net worth of 20%.