Download

1 / 22

220 likes | 230 Views

Explore the efficiency of stock markets and the implications for investors and management. Learn about random walks, pricing efficiency, and behavioral finance.

E N D

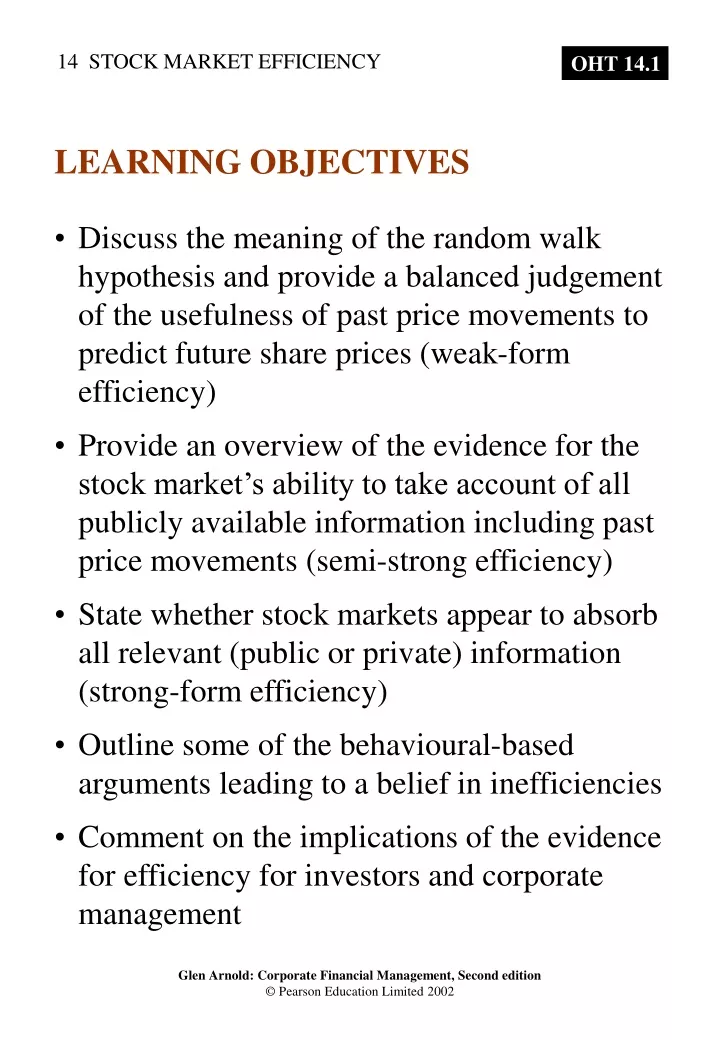

LEARNING OBJECTIVES • Discuss the meaning of the random walk hypothesis and provide a balanced judgement of the usefulness of past price movements to predict future share prices (weak-form efficiency) • Provide an overview of the evidence for the stock market’s ability to take account of all publicly available information including past price movements (semi-strong efficiency) • State whether stock markets appear to absorb all relevant (public or private) information (strong-form efficiency) • Outline some of the behavioural-based arguments leading to a belief in inefficiencies • Comment on the implications of the evidence for efficiency for investors and corporate management

WHAT IS MEANT BY EFFICIENCY? In an efficient capital market security (for example shares) prices rationally reflect available information. The current level is an unbiased estimate of its true economic value based on information revealed 1 The direction of the price share movement 2 The size of that movement 3 The absence of abnormal profit possibilities Most investors are too late.

TYPES OF EFFICIENCY 1 Operational efficiency 2 Allocational efficiency 3 Pricing efficiency

THE VALUE OF AN EFFICIENT MARKET 1 To encourage share buying 2 To give correct signals to company managers - feedback - required rate of return - disclosure 3 To help allocate resources

V olvo share price Exhibit 14.1 New information (an electric car announcement by BMW) and alternative stock market reactions – efficient and inefficient Line 3 Overreaction followed by deflation Line 2 Anticipatory Efficient market price movements (information leak) B A BMW/ share price 4 Persistent inefficiency Line Line 1 Slow reaction –10 –5 0 +5 +10 +11 Days before (–) Announcement and days after (+) date announcement

Share index Share index RANDOM WALKS 180 170 160 150 140 Share index 130 120 110 100 90 80 W eeks ( ) a 150 140 130 Share index 120 110 100 90 80 W eeks ( ) b Exhibit 14.2 Charts showing the movements on the FT 100 share index and a randomly generated index of prices. Which is which?

WHY DOES THE RANDOM WALK OCCUR? The price at any one time reflects all available information and it will only change if new information arises. Actual movement after ‘pattern’ is identified Movement expected by chartist Share price A B T ime 6 months Exhibit 14.3 A share price pattern disappears as investors recognise its existence

THE THREE LEVELS OF EFFICIENCY 1 Weak-form efficiency Share prices fully reflect all information contained in past price movements. 2 Semi-strong form efficiency Share prices fully reflect all the relevant publicly available information. 3 Strong-form efficiency All relevant information, including that which is privately held, is reflected in the share price.

WEAK-FORM TESTS A simple price chart – chartists Exhibit 14.4 The ‘head and shoulders’ pattern A Share price B T ime

Exhibit 14.5 A ‘line and breakout’ pattern Break out Resistance line Share price Support line T ime

The Filter approach • Focuses on the long-term trends and on filtering short-term movements. • The Dow theory • The stock market is characterised by three trends. • The primary trend is the long-term move in • share prices • The intermediate trend runs for weeks or • months • Tertiary trends last for a few days Exhibit 14.6 The Dow theory D C B Market index A Time

Weight of evidence: the weak form of efficiency is generally accepted. However, there are exceptions. Overreaction hypothesis De Bondt and Thaler Dissanaike Chopra, Lakonishok and Ritter Simple trading rules Weak-form efficiency

SEMI-STRONG FORM TESTS • Is it worthwhile expensively acquiring and analysing publicly available information? • Semi-strong efficiency undermines fundamental analysts. • Information announcements • Manipulation of earnings • Seasonal, calendar or cyclical effects • Small firms • Underreaction/momemtum

Value investing Price-earnings ratios Share price low relative to the balance sheet assets (book-to-market ratio) High dividends relative to the share price (high-yield shares) Bubbles Comment on the semi-strong efficiency evidence SEMI-STRONG FORM TESTS

PETER LYNCH BENJAMIN GRAHAM WARREN BUFFETT and CHARLES MUNGER THE VIEWS OF SCEPTICAL PRACTITIONERS

It is possible to trade shares on the basis of inside knowledge and thereby make abnormal profits Curbing insider dealing: Criminal offence Stock market rules Information disclosure No dealing at certain times STRONG-FORM TESTS

EMH: Investors are rational Or, even if some are irrational, the actions of rational investors eliminate pricing anomalies Behavioural finance: Investors frequently make systematic errors These errors push share prices away from fundamental value BEHAVIOURAL FINANCE

Three lines of defence Investors are rational Even if some are not rational, their irrationally inspired trades of securities are random and therefore the effects of their irrational actions cancel each other out without moving prices away from their efficient level. If the majority of investors are irrational in similar ways and therefore have a tendency to push security values away from the efficient level this will be countered by rational arbitrageurs who eliminate the influence of the irrational traders on prices. Noise trader risk Risky arbitrage BEHAVIOURAL FINANCE

Overconfidence Representativeness Conservatism Narrow framing Ambiguity aversion Positive feedback and extrapolative expectations Regret Cognitive dissonance Availability heuristic Miscalculation of probabilities Some cognitive errors made by investors

MISCONCEPTIONS ABOUT THE EFFICIENT MARKET HYPOTHESIS 1 Any share portfolio will perform as well as or better than a special trading rule designed to outperform the market 2 There should be fewer price fluctuations 3 Only a minority of investors are actively trading, most are passive, therefore efficiency cannot be achieved

IMPLICATIONS OF THE EMH FOR INVESTORS 1 For the vast majority of people public information cannot be used to earn abnormal returns 2 Investors need to press for a greater volume of timely information 3 The perception of a fair game market could be improved by more constraints and deterrents placed on insider dealers IMPLICATIONS OF THE EMH FOR COMPANIES 1 Focus on substance, not on short-term appearance 2 The timing of security issues does not have to be fine-tuned 3 Large quantities of new shares can be sold without moving the price 4 Signals from price movements should betaken seriously