Download

1 / 26

260 likes | 275 Views

Learn vital financial advice such as prudent spending, saving for emergencies, and efficient investing strategies. Discover common pitfalls to avoid and tips for building wealth and security.

E N D

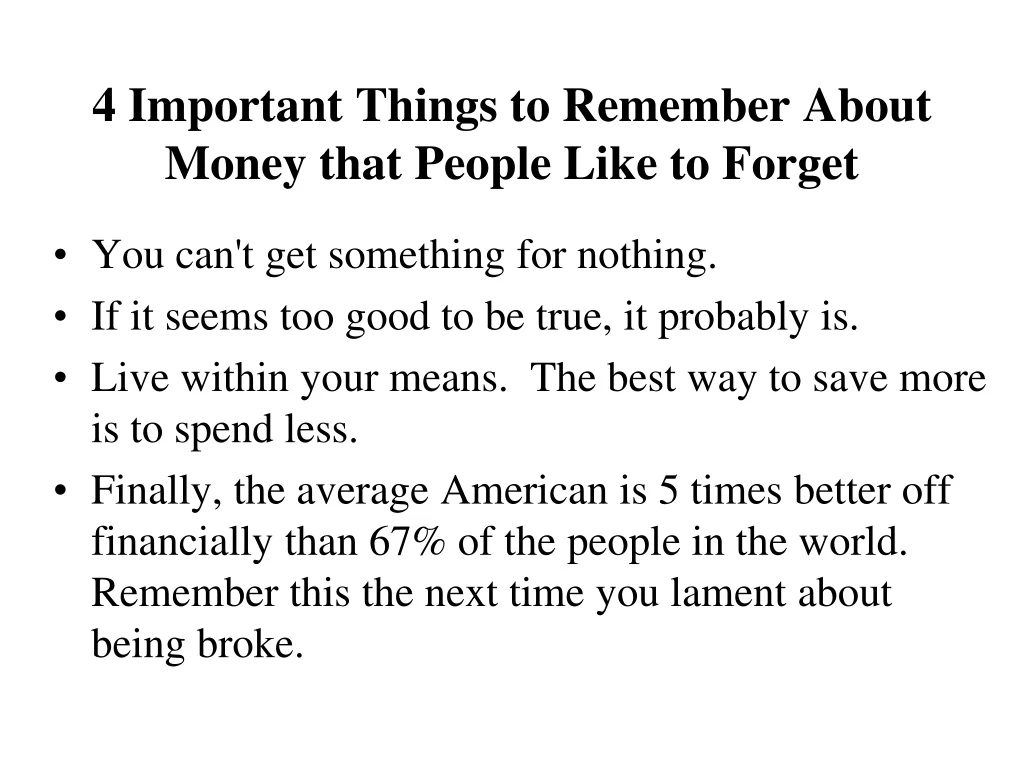

4 Important Things to Remember About Money that People Like to Forget • You can't get something for nothing. • If it seems too good to be true, it probably is. • Live within your means. The best way to save more is to spend less. • Finally, the average American is 5 times better off financially than 67% of the people in the world. Remember this the next time you lament about being broke.

GET RID OF BAD DEBT • Bad debt is money owed on depreciating goods like cars and credit cards • Good debt is money owed on appreciating goods like homes, real estate, jewelry, art, & education • Pay off all credit cards and high interest loans. There aren't any investments that will pay more than what a credit card charges. Why put money in a 3% savings account when you are paying 20% on your visa? • When your debt ratio starts to push beyond 25-33%, you're in danger. (Bad) Debt = Debt to Income Ratio Annual Income • Example: You make $30,000/year but owe $15,000 in loans. Your debt ratio is 50%.

MAKE A BUDGET • Spending less is the only way you'll have money to invest. Stick to your budget, even if you have to use desperate measures. SAVE 10% FOR RETIREMENT • If you save 10% of your income every month starting in your early 20's, you'll have plenty for retirement.

SAVE AN ADDITIONAL 10% FOR OTHER EXPENSES • You'll need money for a house, kids, vacations, home improvements, etc. . . Americans save less than 5% of their income versus 10% for Germans and 15% for Japanese. BUILD A SAFETY NET • You should have 3-6 months worth of income saved for emergencies (like losing your job). This is NOT spending money.

Consequences of Overspending • PAY MORE TAXES. The more you spend, the more sales tax you pay. Plus you have less money to fund retirement accounts which save you money on income taxes. • HARDER TO BUY A HOUSE(OR ANY OTHER TYPE OF LOAN). Banks will be less likely to loan you money for a home, school, or business if you have outstanding debts. • CONSTANT INSECURITY. Living paycheck to paycheck can be stressful, especially when the economy turns sour.

Two Things To Know Before You Start Investing • Now that you have gotten rid of your debt, you're ready to start investing. In order to invest wisely and appropriately, you need to know two things: • your net worth and • your marginal tax rate.

NET WORTH • is your Total Assets (savings, pension) - your Total Liabilities (student loans, credit cards, car loan). If your net worth is. . . • LESS THAN HALF OF YOUR ANNUAL INCOME: Bad news, but you're in the majority. Get rid of debts first & then build a safety net of 3-6 months income. • MORE THAN HALF OF YOUR INCOME BUT LESS THAN A FEW YEARS: Okay, especially if you're younger, but if you don't have a house, you should reduce spending & accelerate saving. • MORE THAN A FEW YEARS' INCOME: Good. You're on track to meet reasonable financial goals.

MARGINAL TAX RATE • is the rate of tax that you pay on your last or highest dollars of income. For example, if you make $30,000, you pay 34% tax on every dollar between $27,057-30,000. You would pay 32% tax rate on every dollar from $1-27,057.. SINGLES TAXABLE INCOMECOMBINED STATE & FEDERAL TAX RATE • Less than $27, 057 32% (28 + 6) • $27,057-35,792 34% (28 + 8) • $35,793-65,550 35% (28 + 9) • $65,551-136,750 37% (31 + 9) • $136,751-297,350 42% (36 + 9) • OVER $297,350 45% (40 + 9) Note: the combined state & federal tax rates do not add up because some state income tax is deductible from federal taxes

MistakesINVESTING WITH IGNORANCE • Don't buy an investment based on a sales pitch, timing, or a friend's recommendation if you don't understand what you're buying or its risks. Ask questions. • Timing is when you invest or sell your investments by timing the market; i.e., you always try to buy at certain times when you think the market will be lowest and sell when you think it’s at its peak. • Timing can also be when you day-trade. Day trading is buying and selling stocks, bonds, and mutual funds within a day.

MistakesPAYING HIGH FEES AND COMMISSIONS • All fees & commissions come out of your pocket, & there is no proof that more expensive investments yield better results. NOT DIVERSIFYING • Putting all your money in one place is neither profitable nor safe. You're either risking too much or not enough. IGNORING TAX CONSEQUENCES • Your growth and value of your investments will depend tremendously on your MTR. Know your MTR when making investments.

Rule of 72 • You can calculate how long it will take your money to double in a lending investment by following the Rule of 72 • Divide 72 by the interest rate you are earning on your investment and that equals the number of years it takes your money to double. • Example of Rule of 72: If you are earning 6% on your CD, divide 72 by 6 and you will find it takes 12 years to double your money. (72/6 = 12).

Investment Types: LENDING • Lending investments mean that you make money by lending someone--the government, a company, a bank--money for a certain amount of time at which time they agree to return the principal (original amount loaned) plus interest. • examples included CDs (certificates of deposit), treasury notes & bills, and corporate bonds. • ---benefits: safe and easy to purchase; make more money than savings accounts • ---downfalls: inflation rates can change the value of your investment; don't make big money off of bonds

Investment Types: Bonds • Bonds are lending money to the government (local, state, or federal) or a corporation. • You are guaranteed the principal (the amount you loan) plus interest for a certain time period (6 months to 30 years) • If it is a corporate bond and the company has financial trouble, you are paid before the stockholders. This is one the reasons bonds are considered a safe investment. • Types of bonds include CDs (certificate of deposit), Treasury Bills (T-bills), Savings Bonds, etc. . . • You can compare bond rates at bankrate.com

Investment Types: OWNING • Owning investments mean that you make money by owning something--land, stock (part of a company), gold. You make money if its value goes up and you sell. • ---benefits: make the highest profits of any type of investment; power & voice in your investment • ---downfalls: highest risk investment with no guarantees; can be time consuming to manage Safe Risky Least Profit Greatest Profit

Investment Types: Stocks • Stocks are shares of ownership in a publicly held company, aka, a corporation • A stock market is a public place to buy and sell stocks; some famous ones are the NYSE, NASDAQ, and local stock markets like the Pacific Stock Exchange • On average, over the past 150 years, stocks earn a 10% return. This accounts for lows, highs, recessions, etc. . .

Things to consider when buying stock • Stability. How long has the company been around? What is the outlook for its future? • Past Record. How has it performed in the past? What kinds of ups and downs has the company endured? • Price-Earnings Ratio. This is the ratio of the price of the stock to its actual earnings. If the ratio is high, it usually means that the company is overvalued, that the price of the stock doesn’t actually represent the value of the company. Facebook is a good example--it hasn’t made much profit yet, but its stock is valuable.

The Great Compromise to Owning and Lending Investments: Mutual Funds Benefits of Mutual Funds • A mutual fund is a large collection of different stocks and bonds which offer you various levels of profit and safety depending on your investment goals. • PROFESSIONAL MANAGEMENT. Fund managers spend all their time surveying stocks and bonds so you don't have to. Sometimes computers serve this role (S&P Index) • LOW COST. Good mutual funds charge less than 1% to be managed. This is much less than the high commissions for single stocks, annuities, and life insurance. • DIVERSIFICATION. If one of your stocks fail in your mutual fund, the other 50 (or whatever) absorb the loss. • FLEXIBILITY. You can determine the profit and risk level by the type of fund you buy. In general, stock funds are riskier but more profitable, while bond funds are the opposite.

How to Select a Good Mutual Fund • COST. Never pay a sales load or commission; you want "no load" funds. You must pay an operating expense (aka expense ratio) which covers the costs of your fund manager & paperwork, and you should select funds with OEs of less than 1%. • PERFORMANCE. This can be judged on a number of factors. Look at its rate of return & compare it to other funds in its category. Also check ratings by independent evaluators like Morningstar. • YOUR GOALS. Only choose funds that meet your needs & investment personality, not just ones with high rates of return or what your best friend chooses. Generally, however, the younger you are, the riskier your funds should be. Use the formula below: • 100 - Your Age = % of stock funds • 100-25 =75; this means that since I'm 25, 75% of my mutual funds should be in stock funds.

Categories of Mutual Funds • There are lots of types of funds, but most can be categorized into the following families. Almost all types of funds can be either domestic (stocks in US companies) or foreign. • INDEX FUNDS. These funds have the lowest expense ratios because they are not managed by a human--a computer simply buys the same funds as the designated index such as: • Russel 2000: the 2000 smallest companies with growth potential • S & P 500: the 500 largest blue chip companies • NASDAQ 100: the most profitable 100 companies in the NASDAQ • GROWTH.These funds seek long-term growth. They tend to be risky, especially aggressive growth funds. • BALANCE. These funds seek balance between growth and safety. They will have more bonds and get lower returns but are safer and more stable. • INCOME.These seek current income, not future growth. They invest in companies that are profitable now and thus will usually have lower returns than growth funds.

Socially Responsible Mutual Funds • Some people worry that the money they invest in some stock funds is supporting companies whose morals, values, or business practices they don’t agree with. • For example, if you invest in the S & P 500, you will be profiting from tobacco companies, companies that use child labor, and companies that harm the environment • An alternative is to invest in “socially responsible” mutual funds. These are funds that invest in companies with certain principles. For example, you may want to invest in a fund where none of the companies make or sell military weapons, or perhaps you want to invest in a fund where the companies pay a “living wage” to their employees. • Socially responsible funds still have the different categories like growth and balance. • Some funds perform as well or better than traditional funds; others earn less returns because the companies they invest in make less profit (due to their moral standards)

Taxable versus Tax-free Savings & Investment Methods • When investing, you have a choice of taxable and tax free investments. For example, which is better: an account that earns 5% interest but is taxable or one that earns 2.75% tax free? It depends on your MTR! In order to figure out which offer is better, use the formula below: • Formula: Subtract your MTR from 1. Multiply this result by your taxable interest rate. This gives you your REAL rate of return, what you would actually get after paying taxes. Compare it to the tax-free investment and make your decision. Example of Evaluating Tax-Free v. Taxable Investment 1) Subtract your MTR rate from 1: 1-.35 = .65 2) Multiply this result by the taxable investment rate of 5% (5 * .65 =3.25) 3) 3.25% is your real rate of return. It is .5% greater than the tax free investment rate of 2.75%, so it is the better investment.

Saving For Retirement • Employer sponsored • 401k--profitable organizations (private companies) • 403b--non-profit organizations (government jobs, teachers, etc. . .) • Both plans are ways to save for retirement while protecting your money from taxes. You may contribute up to 100% of your salary, up to $11,000, annually. They do 2 things: • 1) allow you to save money tax-free • 2) reduce your current year's income taxes.

Example of Saving w/Tax Sheltered Plans v. Non-Tax Sheltered Plan 401knon 401k Monthly Income 3000 3000 35% MTR 1,050 3000 1950 Retirement Savings (10%) 300 300 2700 1650 35% MTR 945 1755 1650 Note that while you are putting away the same amount, $300, your taxes NOW are much less (over $100 less!) and your money accumulates tax-free

Self-employed • SEP-IRAs: Simplified Employee Pension Individual Retirement Account • These are 401k's for people who own their own businesses or are self-employed. You can save 13% or $22,500 per year. Like other retirement accounts, you don't pay taxes on that money until you retire.

Other Tax Sheltered Investments • IRAs: Individual Retirement Account: you may contribute $3000/year and it accumulates tax free until you withdraw it at 59 1/2 or older • Roth IRAs: a type of IRA that lets you borrow for college expenses or a first home • You can invest in these even if you already have a 401k or 403b; they are additional tax-sheltered investments.

Final Thoughts & Words of Advice • START EARLY. Starting when you’re young, even if you don’t have much money, earns you considerably more money than when you start later with more money. • INVEST REGULARLY. Put money in every month, and don’t worry about “timing” the market. • INVEST AS MUCH AS YOU CAN. Investing even $10 more per month will net you tens of thousands of more dollars later.