Download

1 / 13

130 likes | 454 Views

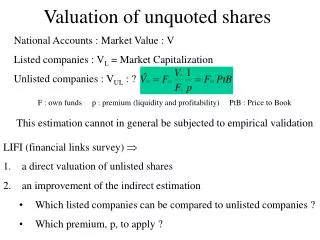

Valuation of Unquoted Shares in the U.S. Financial Accounts. Prepared by Susan Hume McIntosh and Erik Johnson Taskforce on the Valuation and Measurement of Equity April 14, 2005 Statistics Canada, Ottawa. Relative Importance of Unquoted Shares. Not a major issue in U.S.

E N D

Valuation of Unquoted Shares in the U.S. Financial Accounts Prepared by Susan Hume McIntosh and Erik Johnson Taskforce on the Valuation and Measurement of Equity April 14, 2005 Statistics Canada, Ottawa

Relative Importance of Unquoted Shares • Not a major issue in U.S. • Vast majority of mid-size and nearly all large U.S. corporations have publicly traded shares. • Unquoted shares at year-end 2003 estimated at only 12% of the total market value of equity of domestic corporations.

Current Valuation Method • Annual data from estate tax returns. • Gives split between closely held stock (unquoted shares) and publicly traded shares (including mutual funds). • Assume same ratio of unquoted to publicly traded shares for aggregate household sector.

Advantages • Estate tax data specifically reports on unquoted shares. • Method ties this value of unquoted shares to a market value of quoted shares.

Disadvantages • Incentive to have low value on unquoted shares to hold down estate taxes. • Only estates over $1.5 million must file. • Threshold rising. • Assumes aggregate household sector holds same proportion as wealthy decedents.

Method Proposed by WGUS • Use balance sheet information and equity market valuations for publicly traded corporations to estimate median market-to-book ratios by industry. • Book value of own funds = paid-in capital and accumulated retained earnings. • Apply industry market-to-book ratios to own funds of non-publicly traded corporations (S-corporations).

Aggregation of Closely Held Equity(Exhibit 1) Market value of S-corps + Market value of private C-corps + Leveraged buyouts (LBOs) (quoted to unquoted) - Initial public offerings (IPOs) (unquoted to quoted) -------------------------------------------- = Market value of closely held equity (unquoted)

New Valuation Method: S-corps(Exhibit 2) • Used IRS Statistics of Income (SOI) tax data. • Latest annual tax data available is for 2001. • For 2001, 2.9 million returns, $1.8 trillion in assets, $535 billion in stockholders’ equity. • Divided into 14 industries. • 2001 growth rate of stockholders’ equity used for 2002-2004. • Linear interpolation of annual stockholders’ equity to obtain quarterly values.

New Valuation Method: S-corps(Exhibit 2) • Calculate market value to stockholders’ equity for public companies for the 14 industries quarterly from 1996-2004 from Compustat data. • Use the median market-to-book ratio. • S-corps stockholders’ equity x Median market-to-book ratio of public corps = S-corps market value

New Valuation Method – C-corps(Exhibit 3) • List of private C-corps with greater than $1 billion in revenue from Forbes magazine. • Find a comparable public company by matching industry and revenue with each private C-corp. • Compute market-to-revenue ratio for comparable public company. • Revenue of private C-corp x Market-to-revenue ratio of public company = Market value of private C-corp

New Valuation Method – C-corps(Exhibit 3) • For 2003, 281 private C-corps with revenues greater than $1 billion. • Able to obtain the Forbes’ list back to 1996. • Will still miss smaller private C-corps. • Only information available in Forbes is revenue, industry classification, and number of employees. • No balance sheet information on private C-corps is available. • Matching of companies is time consuming.

Leveraged Buyouts and Initial Public Offerings • Leveraged Buyouts (LBOs) • Corporations converting from public to private. • Data from Securities Data Company. • Market value of LBOs calculated as Last public price x number of shares outstanding • Initial Public Offerings (IPOs) • Corporations converting from private to public. • Data from Securities Data Company. • Market value of IPOs calculated as Initial market price x number of shrs. outstanding