Download

1 / 22

350 likes | 1.64k Views

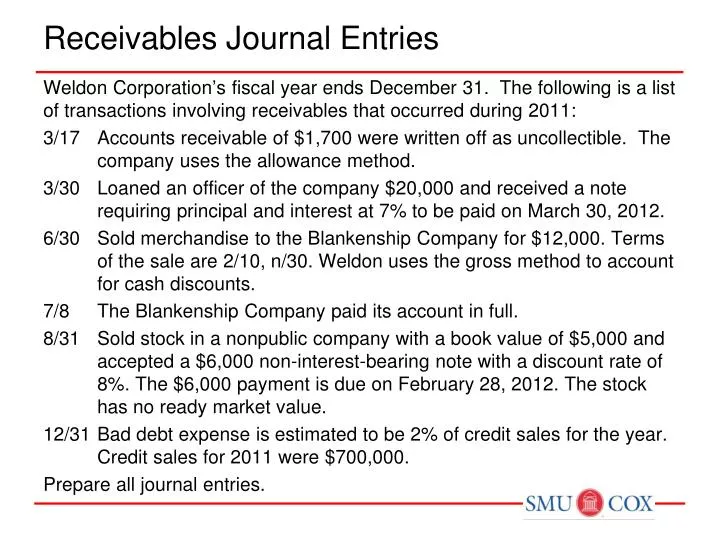

Receivables Journal Entries. Weldon Corporation’s fiscal year ends December 31. The following is a list of transactions involving receivables that occurred during 2011: 3/17 Accounts receivable of $1,700 were written off as uncollectible. The company uses the allowance method.

E N D

Receivables Journal Entries Weldon Corporation’s fiscal year ends December 31. The following is a list of transactions involving receivables that occurred during 2011: 3/17 Accounts receivable of $1,700 were written off as uncollectible. The company uses the allowance method. 3/30 Loaned an officer of the company $20,000 and received a note requiring principal and interest at 7% to be paid on March 30, 2012. 6/30 Sold merchandise to the Blankenship Company for $12,000. Terms of the sale are 2/10, n/30. Weldon uses the gross method to account for cash discounts. 7/8 The Blankenship Company paid its account in full. 8/31 Sold stock in a nonpublic company with a book value of $5,000 and accepted a $6,000 non-interest-bearing note with a discount rate of 8%. The $6,000 payment is due on February 28, 2012. The stock has no ready market value. 12/31 Bad debt expense is estimated to be 2% of credit sales for the year. Credit sales for 2011 were $700,000. Prepare all journal entries.

Receivables Journal Entries 3/17 Accounts receivable of $1,700 were written off as uncollectible. The company uses the allowance method. • Allowance for uncollectible accounts 1,700 Accounts receivable 1,700 3/30 Loaned an officer of the company $20,000 and received a note requiring principal and interest at 7% to be paid on March 30, 2012. • Note receivable 20,000 Cash 20,000

Receivables Journal Entries 6/30 Sold merchandise to the Blankenship Company for $12,000. Terms of the sale are 2/10, n/30. Weldon uses the gross method to account for cash discounts. • Accounts receivable 12,000 Sales revenue 12,000 7/8 The Blankenship Company paid its account in full. • Cash ($12,000 x 98%) 11,760 Sales discounts ($12,000 x 2%) 240 Accounts receivable 12,000

Receivables Journal Entries 8/31 Sold stock in a nonpublic company with a book value of $5,000 and accepted a $6,000 non-interest-bearing note with a discount rate of 8%. The $6,000 payment is due on February 28, 2012. The stock has no ready market value. • Notes receivable (face amount) 6,000 Discount on note receivable 227 Investments (book value) 5,000 Gain on sale of investments (difference) 773 PV(FV=6,000, pmt=0, n=6/12, i=8%) = 5,773 12/31 Bad debt expense is estimated to be 2% of credit sales for the year. Credit sales for 2011 were $700,000. • Bad debt expense ($700,000 x 2%) 14,000 Allowance for uncollectible accounts 14,000

Receivables Journal Entries Adjusting Entries: To accrue interest earned on note receivable from loan to officer. • Interest receivable1,050 Interest revenue ($20,000 x 7% x 9/12) 1,050 To accrue interest earned on note receivable from sale of stock. • Discount on note receivable 154 Interest revenue ($5,773 x 8% x 4/12) 154

Percentage-of-Completion Example – 3 Perfectionist Construction Company was the low bidder on an office building construction contract. The contract bid was $9,000,000, with an estimated cost to complete the project of $7,000,000. The contract period was 30 months starting May 1, 2012. Because of changes requested by the customer, the contract price was adjusted downward to $8,600,000 on May 1, 2013. A record of construction activities for the years 2012–2015 is as follows: Prepare all journal entries and the relevant balance sheet entries for 2012–2015 under the percentage-of-completion method of revenue recognition.

Percentage-of-Completion Example – 3 2012 Construction in progress 1,900,000 Cash, materials, etc. 1,900,000 Accounts receivable 2,500,000 Billings on construction contract 2,500,000 Cash 1,900,000 Accounts receivable 1,900,000 Percent complete: 1,900,000 / (1,900,000 + 5,150,000) = 26.95% Expected profit: 9,000,000 – (1,900,000 + 5,150,000) = 1,950,000 Construction in progress 525,525(26.95% * 1,950,000) Construction expenses 1,900,000 Revenue from long-term contract 2,425,525 (26.95% * 9 mil) (CA) Accounts receivable 600,000 (CL) Billings in excess of cost and profit 74,475

Percentage-of-Completion Example – 3 Perfectionist Construction Company was the low bidder on an office building construction contract. The contract bid was $9,000,000, with an estimated cost to complete the project of $7,000,000. The contract period was 30 months starting May 1, 2012. Because of changes requested by the customer, the contract price was adjusted downward to $8,600,000 on May 1, 2013. A record of construction activities for the years 2012–2015 is as follows: Prepare all journal entries and the relevant balance sheet entries for 2012–2015 under the percentage-of-completion method of revenue recognition.

Percentage-of-Completion Example – 3 2013 Construction in progress 3,600,000 Cash, materials, etc. 3,600,000 Accounts receivable 3,400,000 Billings on construction contract 3,400,000 Cash 3,100,000 Accounts receivable 3,100,000 Percent complete: (1,900+3,600) / (1,900+3,600+1,600) = 77.46% Expected profit: 8,600,000 – (1,900,000+3,600,000+1,600,000) = 1,500,000 Construction in progress 636,035 Construction expenses 3,600,000 Revenue from long-term contract 4,236,035 (77.46%*8.6mil)–2,425,525 (CA) Accounts receivable 900,000 (CA) Cost and profit in excess of billings 761,560

Percentage-of-Completion Example – 3 Perfectionist Construction Company was the low bidder on an office building construction contract. The contract bid was $9,000,000, with an estimated cost to complete the project of $7,000,000. The contract period was 30 months starting May 1, 2012. Because of changes requested by the customer, the contract price was adjusted downward to $8,600,000 on May 1, 2013. A record of construction activities for the years 2012–2015 is as follows: Prepare all journal entries and the relevant balance sheet entries for 2012–2015 under the percentage-of-completion method of revenue recognition.

Percentage-of-Completion Example – 3 2014 Construction in progress 1,670,000 Cash, materials, etc. 1,670,000 Accounts receivable 2,700,000 Billings on construction contract 2,700,000 Cash 2,500,000 Accounts receivable 2,500,000 Percent complete: 100% Expected profit: 8,600,000 – (1,900,000+3,600,000+1,670,000) = 1,430,000 Construction in progress 268,440 (1,430,000–525,525–636,035) Construction expenses 1,670,000 Revenue from long-term contract 1,938,440 The rest Billings on construction contract 8,600,000 Construction in progress 8,600,000 (CA) Accounts receivable 1,100,000

Percentage-of-Completion Example – 3 Perfectionist Construction Company was the low bidder on an office building construction contract. The contract bid was $9,000,000, with an estimated cost to complete the project of $7,000,000. The contract period was 30 months starting May 1, 2012. Because of changes requested by the customer, the contract price was adjusted downward to $8,600,000 on May 1, 2013. A record of construction activities for the years 2012–2015 is as follows: Prepare all journal entries and the relevant balance sheet entries for 2012–2015 under the percentage-of-completion method of revenue recognition.

Percentage-of-Completion Example – 3 2015 Cash 1,100,000 Accounts receivable 1,100,000

P6-7 Answer the following questions related to Dubois Inc. • Dubois Inc. has $600,000 to invest. The company is trying to decide between two alternative uses of the funds. One alternative provides $80,000 at the end of each year for 12 years, and the other is to receive a single lump-sum payment of $1,900,000 at the end of the 12 years. Which alternative should Dubois select? Assume the interest rate is constant over the entire investment. First alternative: i(PV=600,000, FV=0, pmt=80,000, n=12) = 8.09% Second alternative: i(PV=600,000, FV=1,900,000, pmt=0, n=12) = 10.08% Choose second alternative.

P6-7 • Dubois Inc. has completed the purchase of new Dell computers. The fair value of the equipment is $824,150. The purchase agreement specifies an immediate down payment of $200,000 and semiannual payments of $76,952 beginning at the end of 6 months for 5 years. What is the interest rate, to the nearest percent, used in discounting this purchase transaction? PV = 824,150 – 200,000 = 624,150 FV = 0 Pmt = 76,952 n = 10 (semiannual for five years) i = ? 4% per period which is 8% annual

P6-7 • Dubois Inc. loans money to John Kruk Corporation in the amount of $800,000. Dubois accepts an 8% note due in 7 years with interest payable semiannually. After 2 years (and receipt of interest for 2 years), Dubois needs money and therefore sells the note to Chicago National Bank, which demands interest on the note of 10% compounded semiannually. What is the amount Dubois will receive on the sale of the note? PV = ? FV = 800,000 (no change since only paying interest) Pmt = 32,000 (800,000 * 8% * 6/12 every six months) n = 10 (semiannual for five more years) i = 5% (per period) At time of sale to bank, PV = 738,226

P6-7 • Dubois Inc. wishes to accumulate $1,300,000 by December 31, 2022, to retire bonds outstanding. The company deposits $200,000 on December 31, 2012, which will earn interest at 10% compounded quarterly, to help in the retirement of this debt. In addition, the company wants to know how much should be deposited at the end of each quarter for 10 years to ensure that $1,300,000 is available at the end of 2022. (The quarterly deposits will also earn at a rate of 10%, compounded quarterly.) PV = 200,000 FV = 1,300,000 Pmt = ? n = 40 (quarterly for 10 years) i = 2.5% (per period) Quarterly deposits should be 11,320

Balance Sheet Classification Cone Corporation is in the process of preparing its December 31, 2009, balance sheet. There are some questions as to the proper classification of the following items: • $50,000 in cash set aside in a savings account to pay bonds payable. The bonds mature in 2013. • Prepaid rent of $24,000, covering the period January 1, 2010, through December 31, 2011. • Note payable of $200,000. The note is payable in annual installments of $20,000 each, with the first installment payable on March 1, 2010. • Accrued interest payable of $12,000 related to the note payable. • Investment in marketable securities of other corporations, $80,000. Cone intends to sell one-half of the securities in 2010. Required: Prepare a partial classified balance sheet to show how each of the above items should be reported.

CONE CORPORATION Balance Sheet (Partial) At December 31, 2009 Assets Current assets: Marketable securities $ 40,000 Prepaid rent 12,000 Investments: Bond sinking fund 50,000 Marketable securities 40,000 Other assets: Prepaid rent * 12,000 Liabilities and Shareholders' Equity Current liabilities: Interest payable $ 12,000 Current maturities of long-term debt 20,000 Long-term liabilities: Note payable 180,000 * In practice, companies often report all prepaid expenses as current assets.

Additional information: 1. Net loss for the year was $2,500. 2. No dividends were declared during 2012. Prepare a classified balance sheet as of December 31, 2012. E5-11 Debits Credits Accounts Payable $10,000 Accumulated Depreciation— Equipment 9,000 Bonds Payable (due 2017) 9,000 Cash $ ? Common Stock 10,000 Equipment 48,000 Insurance Expense 1,400 Interest Expense 900 Prepaid Insurance 1,000 Rent Expense 1,200 Retained Earnings 20,000 Salaries and Wages Expense 9,000 Salaries and Wages Payable 500 Service Revenue 10,000 Supplies (inventory) 1,200 Trademarks 950 Unearned Service Revenue 2,000 Total $ ? $ ? Presented above is the adjusted trial balance of Abbey Corp at December 31, 2012.

E5-11 ABBEY CORPORATION Balance Sheet December 31, 2012 Assets Current assets Cash $ 6,850 Supplies 1,200 Prepaid insurance 1,000 Total current assets $ 9,050 Equipment 48,000 Less: Accumulated depreciation 9,000 39,000 Intangible assets—trademarks 950 Total assets $49,000

E5-11 Liabilities and Stockholders’ Equity Current liabilities Accounts payable $10,000 Salaries and wages payable 500 Unearned service revenue 2,000 Total current liabilities $12,500 Long-term liabilities Bonds payable 9,000 Total liabilities 21,500 Stockholders’ equity Common stock 10,000 Ret earn ($20,000 – $2,500*) 17,500 Total stockholders’ equity 27,500 Total liabilities and stockholders’ equity $49,000 *[$10,000 – ($9,000 + $1,400 + $1,200 + $900)]