Download

1 / 25

350 likes | 614 Views

Strategy for Agriculture Exports. Flow Of Presentation. Global Trends Concentration of Modern Retailing Agriculture Trading shares by Channel Consumer, Product & Business dynamics Global Super Market supply chain Where do we stand Strengths Weaknesses Strategic Framework for Agri-Exports

E N D

Flow Of Presentation • Global Trends • Concentration of Modern Retailing • Agriculture Trading shares by Channel • Consumer, Product & Business dynamics • Global Super Market supply chain • Where do we stand • Strengths • Weaknesses • Strategic Framework for Agri-Exports • 360 Degree Model • Policy Issues & Way forward • Export Opportunities

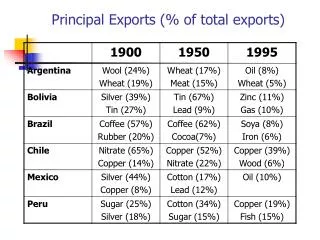

Global Trends Concentration of Modern Retailing & Trends Top 30 retailers: $2.1 trillion=31% of global market Over concentration of Modern retailing in developed markets: Reduced ROI’s for Retailers & Suppliers. Increasing internationalization: Asia & Eastern Europe Growth of discounters and specialty formats Growth of Private label brands: 30 to 50% of top 30 retailer sales & 20 to 47% of market share by value. Food= 60-75%, Non-food=25-40% $1.3 trillion food sales $175 billion F&V Carrefour , Tesco, Metro F&V: $29.5b

Global Trends Agriculture Trading Shares by ChannelModern Retailing: HyperMarkets, Super Markets, DiscountersTraditional retailing: Street stalls, Growers, Traditional Markets, Growers, Others

Consumer Trends: Greater demand for convenience= fresh cut, processed foods. More diversity of choice, for prolonged seasons Growth of demand for ethnic and exotic products Increased demand for organic and fair-trade products More ready-cooked, take-out foods Growth of out-of-home market Business Dynamics: Buying Consolidation and emergence of Modern Retailing: Straight line sourcing: Elimination of middlemen Large scale trading by retail chains: Uniform, consistent quality over prolonged seasons Large centrally controlled purchasing systems Control of supply chain from production areas: Farm to fork Long term business partnerships rather than trading mindset Channelizing of fruit through large and sophisticated specialized companies Supplier’s response: Increasing collaboration: Marketing boards, large scale farming, cooperatives and collaboration between all stake holders of the value chain. Specialization of functions/ activities Marketing focus on customer demands and changing trends Extension of seasons: Production in multiple regions and countries. Customized growing for customers Global Trends • Product : • Food safety • Traceability • Quality systems: Global Gap, HACCP, IFS, BRC • Farm to fork value chain. • Uniformity of sizing and product appearance • Precision agriculture • Consistent and stable quality.

Global Trends Super Market Supply Chain (Farm To Fork) Farmers & Exporters Exporters Specialized handling Co’s Customer demand assesment Customized Product Development Processing & Packaging Inland and sea logistics Importer/ Handling company of Super market Distribution Centers= repackaging / break bulk operations, JIT deliveries Super Markets Consumers HORECA Traders Offices Cash & Carry Hotels Resturants Carteres Food Services Channels

Strengths of Agriculture • Low Labour cost • 4 seasons and variation of climates • Plenty of land • Extended seasons: All four provinces • Strategic Location in Asia: Feed Regional markets • Variation in day and night temperatures These strategic strengths can not be acquired by other nations

Weaknesses of Agriculture & Export Sector • Agriculture: • Very small or very large landholding • Lack of Cooperatives, large scale to spread the fixed cost factors. • No concept of precision agriculture • Diseased fruit trees , especially Mangoes & Kinnows. • Lack of business and commercial sense. • Exports: • Major lack of product diversification and new export markets • Lack of infrastructure, processing and cold chain facilities to meet SPS and quarantine requirements. • Lack of collaboration b/w exporters & farmers for product development. • Volume based, rather than value based exports. • Serious lack of entrepreneurship & reliable business relationship. • Lack of strong government regulations for exports: Quality standards and Supply management. • Minimal Super market penetration • Price killing by over supply • Marketing Failure • Over dependence on government & subsidies The weaknesses can be removed through intelligent effort

Strategic Framework for Agri-Exports Value/ Kg Seasonality Freight Solutions Product economics NATIONAL AGRICULTURAL STRATEGY Market Research & Product identification Hire experts: Why re-invent the wheel?: Do we have the luxury of time? Product Based: Project teams for value chain solution Precision growing, drip irrigation, Agricultural engineers. R&D focus: Reverse engineering of value chain hardware. Local solutions for cost efficiencies 10 acre experimental training farms Product clusters from South-North National Food Security Exports Production/ R&D/ Transfer of technology Product specific pack houses Cold chain near production area Model Projects: PPP: Farmers have eyes, not ears ERP solutions for value chain Production & Process Management Supply Chain is built around a product. Identification of supply chain synergies critical, for cost optimization and increased capacity utilization. Global Gap, HACCP, IFS, BRC Traceability SPS, QA & MRL standards Product Handling guides to shelf Quality Standards Reefer,CA, MAP technologies Customs regulations Cross docking platforms Freight Solutions

360 Degree Model, inclusive of all stake holders Investment Marketing/ lobbying Adoption of technology/ standards MNC’s: Quality inputs & local manufacturing Global Retailers: Access to markets, Marketing Direction Policy making Strategic intervention Legislation for Private sector facilitation Diplomacy & FTA’s Government Exporters/ Private Sector Farmer mobilization Capacity building & technical training 360 Degree Adoption of technology/ standards Precision agriculture Group cooperation Farmers NGO’s Product based project teams: Production & value chain. Demand driven R&D with private sector. Farm management HR Farm economics models Transfer of technology & R&D for local adaptation Funding Technical experts International best practices Donors Academia

Structure to support strategy: • Centralization & Empowerment of government departments within one organization: Private sector culture • Complete financial and administrative authority • HR: representatives & experts from within Pakistan as well as expatriates • Solid Business plan, compensation linked to KPI’s • Reduce duplication of efforts & better utilization of public money • Excellence in execution & better utilization of public money • Large Scale Farming & JV’s with foreign companies: • Sell the benefits: • Large local market, greater consumer propensity to spend • Regional markets of Gulf, Central Asia and Asia: Reduced freight costs: Better margins and lower consumer price: Growth in market size. • Tax breaks and other benefits • MNC seed and pesticide companies inclusion Legislation: • Seed Act & Nursery reforms • International buyers protection against fraud: Criminal cases • Legislation for enforcement of business contracts: e.g. farmers & exporters: criminal cases. • Compulsory Pre-shipment inspections for all export consignments by 3rd parties. • Production Technology & R&D: • Drip Irrigation: 90% government subsidy for export based farming. Essential for supermarket quality. • Hybrid seeds & customized agronomy: Development of product engineers. • CA and Reefer experimentation facilities at UAF for global freight solutions • Government to underwrite losses of private sector for pioneering projects, of new product and new market development. • 20 to 40% R&D subsidy for new projects on CNF value for limited time, till technical issues resolved. • New certified mango orchards, with drip irrigation and precision agriculture. Recovery of young mango orchards. • Sponsor project based transfer of technology and foreign learning. Policy Issues & Way forward Govt structure: function specific. Product based project management: cross functional teams.

Proposals by Engro: • Information system for individual farmer profiles: • Details of farming activities, land, usual crops, revenues and loans status. • Form as a basis for unsecured loans by Banks • Develop reliable crop reporting system (GIS) based: • With collaboration of USAID & Foreign Agriculture Service (FAS) of USDA • Project to replace primitive crop reporting system • Form basis for reliable information for planning crop commodity imports, exports, storage, distribution • Develop Standardization laws and verification and certification agency for exports: • Agency to have accredited & well equipped labs and equipment • Develop single new non governmental organization with public/ private sector representation • Interest free lending for corporate farms: • Loan channelizing by USAID through commercial banks. • 90% interest free USAID funding & 10% funding with interest. • Corporate Meat farm by Engro: Exports to Middle East. • Channelizing of funds through USAID to Basmati Rice farmers, with Engro guaranteeing Buy-back. • Export oriented floriculture farms in Sind Policy Issues & Way forward Govt structure: function specific. Product based project management: cross functional teams.

Export Opportunities • Medium to long term: • Organics & Fair trade: Labor intensive, in-line with developing countries agricultural practices, hot climates, absorption of air freight, plenty of virgin land availability • Retailers Own Brand Development • Sea Food exports • Tap growth of Asian Cuisine and target Food Services channels • Hybrid Vegetables: Middle East, Central Asian & South East Asian market. • New products: • Melons • Water Melons • Grapes • Lychees (Madagascar: 23000 tons • Baby corn • Pumpkins • Peas • Sweetcorn • Guava Juices • Immediate: • Kinnows: China, Latin America • Mangoes: Sea freight • Floriculture: Freight solution for exports • Potatoes: Better varieties,Value addition & shelf life extension • Value added products • Pulps & Nectars • Packaged vegetables: Kenya example • Convenience packaging: ready to eat meals • Halal meat exports to Middle East, Europe & Asia. • Basmati Rice: Product & Brand development for direct Super Market exports. • Contractual farming & Buy back to ensure BRC standards. • Dairy exports: Specialty Cheeses & Milk based products We need to upgrade from Commodity trading to Product/ Brand development: increase margins by moving up the value chain

All stake holders need to act UNITED and play their respective roles in a FOCUSED AND SYNERGISED effort to: • Make up for lost time • By making 360 degree efforts on a war footing • To develop world class products & services in next 3-5 years • to capitalize on the emerging global trade opportunities • Metro’s support to act as a catalyst will always be there. • THANK YOU

Developing countries F&V exports to E.U 35 % of E.U market7 billion Euros exportsTop importing countries: U.K, France, Germany, Holland, Begium, Italy.

Steps to Mango Exports Shipment Post shipment handling Fruitdevelopment Harvest & Packing • Loading • Temperature and CA settings • Transit conditions monitoring • Developing special Mango ripening chambers across E.U. • Special equipment in Metro stores for Mangoes • Identification of disease free orchards • Customized agronomy for each farm • Develop strong fruit for sea exports • Reception • Selection • HWT • Drying • Waxing • Grading • Packing • Pre-cooling • Cooling Farmers + Metro Farmers + Third party Metro + Maersk Metro

Benefits of Metro • Above average buying price for Mangoes. • Guaranteed buy back • No middle men = better profits • Long term profitable, reliable business partner. • State of the art, transfer of technology. • Global supply chain excellence. • Massive reach and depth in 31 countries. ** Metro provides a comprehensive farm development, supply chain and marketing solution.

Mango VISION • Pakistan Mangoes: Oil/ Gold of the future • Build exotic, premium positioning for Pakistan Mangoes = High vaue/kg • Build before India.

FOUR MAIN EXPORT DESTINATIONS VOLUME AND VALUE FOR PAKISTAN MANGOES FRUTOPIA GROUP

FOUR MAIN EXPORT DESTINATIONS VOLUME AND VALUE FOR PAKISTAN MANGOES FRUTOPIA GROUP