Download

1 / 16

160 likes | 396 Views

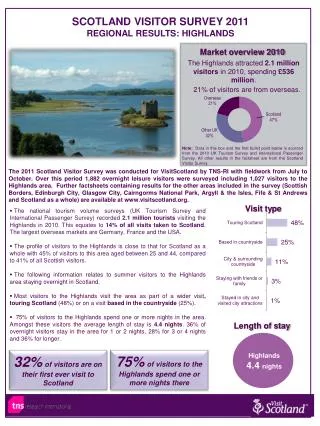

Chicago Metropolitan Industrial Market Overview November 16 2010. Prepared by: George Cutro Colliers International. Industrial Market Presentation Outline. Chicago’s Industrial Market Statistics Chicago’s “Core” Markets Central DuPage Fox Valley I-55 Lake County North Suburbs

E N D

Chicago Metropolitan Industrial Market OverviewNovember 16 2010 Prepared by: George Cutro Colliers International

Industrial Market Presentation Outline Chicago’s Industrial Market Statistics Chicago’s “Core” Markets • Central DuPage • Fox Valley • I-55 • Lake County • North Suburbs • O’Hare Largest Transactions of 2010 Changes and Industry Trends

Metro Chicago Gross Absorption Sq. Ft. Millions 46.88 43.37 46.06 49.72 46.87 59.78 57.20 53.38 45.5 38.56

Metro Chicago Construction Deliveries Sq. Ft. Millions 12.27 21.84 19.10 19.85 13.36 15.22 17.54 20.90 20.86 6.80

Metro Chicago Net Absorption Sq. Ft. Millions

Central DuPage • Inventory 83.97 msf • Available SF 9.93 msf • Vacancy Rate 11.83 % • YTD Leasing Volume (sf) 1.44 msf • YTD Sales Volume (sf) 197,300 sf • YTD Net Absorption (sf) -683,000 sf • Central DuPage Notes • Vacancy rate climbs! • 2010 leasing volume down. • Demand up for buildings for sale. • Rents higher for “Core” product near I-355 expressway.

Fox Valley • Inventory 89.10 msf • Available SF 12.06 msf • Vacancy Rate 13.54 % • YTD Leasing Volume (sf) 1.56 msf • YTD Sales Volume (sf) 1.40 msf • YTD Net Absorption (sf) 1.34 msf • Fox Valley Notes • Available supply dropping • Sale volume spikes • Positive absorption!

I-55 Corridor • Inventory 72.94 msf • Available SF 12.87 msf • Vacancy Rate 17.64 % • YTD Leasing Volume (sf) 2.33 msf • YTD Sales Volume (sf) 666,700 sf • YTD Net Absorption (sf) -1.39 msf • I-55 Corridor Notes • YTD leasing volume down. • Net absorption negative! • Speculate development non-existent • 17.64 % highest vacancy rate ever!

Lake County • Inventory 69.95 msf • Available SF 10.15 msf • Vacancy Rate 14.51 % • YTD Leasing Volume (sf) 1.20 msf • YTD Sales Volume (sf) 401,000 sf • YTD Net Absorption (sf) -640,500 sf • Lake County • Vacancy rate falls! • Third quarter net absorption posts positive results! • Local company expands presence in market.

North Suburbs • Inventory 57.65 msf • Available SF 5.90 msf • Vacancy Rate 10.23 % • YTD Leasing Volume (sf) 255,700 sf • YTD Sales Volume (sf) 172,700 sf • YTD Net Absorption (sf) -2.33 msf • North Suburbs • Vacancy rate at all-time high. • Inventory continues to shrink. • Sale activity Anemic!

O’Hare • Inventory 140.18 msf • Available SF 17.50 msf • Vacancy Rate 12.48 % • YTD Leasing Volume (sf) 3.91 msf • YTD Sales Volume (sf) 524,200 sf • YTD Net Absorption (sf) -644,100 sf • O’Hare Notes • Vacancy rate hits all time high. • Leasing activity up. • 6B Tax program still obtainable. • Freight forwarders in play

Top Lease Transactions 2010 Clorox 1,350,000 sf Far South World Kitchen, LLC 700,200 sf Far South 3M 650,000 sf DeKalb Co. Sony Music Entertainment 579,900 sf I-55 BP North American 574,300 sf NW Ind. Jacobson Companies “Fonterra Milk Prdts” 507,200 sf I-80 AGL Direct 499,200 sf I-55 Midwest Custom Case, Inc. 455,900 sf Far South NACA Logistics USA, Inc. 440,200 sf Central DuPage Hosely International Trading Company 376,000 sf NW Ind.

Top User Sale Transactions Uline 1,000,000 sf SE Wis. Freudenberg Household Products 525,000 sf I-88 R. R. Donnelley 514,000 sf I-88 MAT Holdings 506,800 sf I-55 Ionian, LLC 492,800 sf Chicago Gordon Food Service 480,000 sf SE Wis. The Jel Sert Company 304,500 sf I-88 GRM Information Management Svc’s 296,100 sf South Subs. Ascent Corporation 284,200 sf I-290 North EMCO Chemical Distributors 259,600 sf SE Wis.

Metro Chicago Trends • Speculative development dead, however BTS construction volume up • Institution/REIT Landlords compete hard for deals • Land prices falling??? • Cap rates for “Core Product” falling • Some landlords not competing for high TI transactions • Ownership stability