Download

1 / 38

670 likes | 1.6k Views

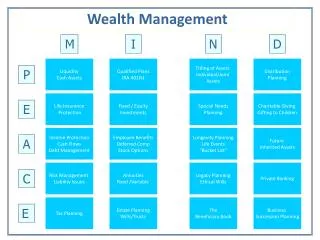

An Introduction to Wealth Management. Doug Alsdorf Fine print: use at your own risk. We’ll talk about these:. Basic Personal Finance Buy Low Sell High; Diversify? Health care and life insurance Buy a home or invest? Refinance? Living trusts IRAs and saving for college (needs work)

E N D

An Introduction to Wealth Management Doug Alsdorf Fine print: use at your own risk

We’ll talk about these: • Basic Personal Finance • Buy Low Sell High; Diversify? • Health care and life insurance • Buy a home or invest? Refinance? • Living trusts • IRAs and saving for college (needs work) • Investments and investment managers • 8 things to consider • Finding an investment manager • Picking an investment manager • Investing methods (needs work) • Work with smart people!

Microsoft in 2012 Dollars $58 $30 Log scale Y Axis $0.35 $0.09 MSFT: Purchase 1000 shares in 1986 at 9 cents per share would give you at least $30,000 in 2012. That’s an increase of 333X. Purchase 1000 shares in 1999 at $40 per share, now worth $30,000 or a loss of $10,000. MSFT starting providing dividends in ~2003. These appear to be 10 cents a share, on average or maybe more, and 33 payouts since 2003, provides you with an extra $3300, so your loss would “only” be $6700.

The Dow Since 1900 Q: Which is bigger, crash of 1929 or 2008? A: 1929, see log scale plot

The Dow Since 1900a broad indicator of the U.S. Economy Q: How long is enough time to make money? A: Probably about 30 years Lesson: Start investing at age 35 to retire by 65 Dow doubled in 40 years 1900 to WWII Dow increases 6X 1945-1965 No growth 1965-1980 Increases 10X No growth 2000-2012

How make money? • The Dow is one of several indices. It’s a broad indicator of the overall U.S. economy. • Investing in the Dow stocks (i.e., the exchange traded funds or ETFs that mimic the Dow) will produce some wealth. • Probably will need investments in other sectors. • Lets look at a couple of commodities, Gold and Oil

Gold From $300 to $1600 in 10 years. That’s a nice growth!

Oil From $30 to $100 over about 10 years. That’s a nice growth

Diversify? • Price of oil from 1980 to 2000 went down from $37 to $27, while Dow soared. • Price of gold from 1980 to 2000 declined from about $400 to $300, while Dow soared. • From the simple examples of the Dow and two commodities, you can see that diversity in your investments might help. • $1000 of Dow, $1000 of oil, and $1000 of gold in 1980 would be worth $12500 in 2000. Carrying forward the $12500 from 2000 to 2012, would increase to over $17500. Total growth in wealth is about 6X. • Dow alone over same 30 year period went up 10X, but you would have been angry the past 10 years of no growth. How disciplined are you in sticking with an investment? How long should you stick with an investment? • Lots of ways to diversify. • See Spreadsheet

Buy Low, Sell High • Many professional investment managers will tell you that timing the market is a bad idea. • Many academic studies show that timing the market, on average, results in losses or growth that is less than the passive approach. • Look at the charts. Take any given point in time and can you tell from the previous history which way the price will go, i.e., up or down? • Need additional evidence beyond that of price alone, but are you an expert in this additional stuff? • Professional investors are experts, but like all expertise, some are better than others. • See DJIA Spreadsheet, S&P 500 tab

Health Insurance • When I was young, I didn’t care about health insurance; nothing could stop me, I was indestructible. • Hopefully you aren’t as foolish as me. • Get a good job that has health benefits (duh!). • When changing jobs, make certain that the time period between jobs has health coverage. • If you are laid-off, make certain you understand the health coverage.

Life Insurance • In case you die, life insurance allows your family to live without having to sell everything. • Life insurance avoids the double whammy of family dealing with your death and loss of income hence loss of home. • How much life insurance do you need? • Depends on income. If spouse earns significant more than the other, then might need differing amounts of insurance. • Life insurance is cheap when you’re young but when you’re old, you should have a savings thus don’t need life insurance. • See spreadsheet

Is Your Home a Good Investment? • Your home and your 401(k) will probably be your first big investments. Unfortunately, your home is not the best nor worst investment you can make. • First, we’ll look at how much it costs you to take-out a loan to pay for your home. • 30Yr fixed 3.875%, $240,000 loan costs $166K in interest. Each monthly payment equals $1129 so your total of all payments equal $406K. Only after 12yrs 2mos will your interest payment be less than the principal payment. • See HomeMortgage spreadsheet

Is Your Home a Good Investment? • Home was purchased with 20% down, i.e., $60K. So, could be investing in “the Market” $60K plus each monthly payment of $1129. • Next, consider if the above was invested. • Assume 4.0% ROI, after 30 years would have $956K. • Home value increases at say 3.5% • After 30 years, home is worth $842K • So, what’s the catch? • Home loan interest payments are tax deductible • See HomeMortgage spreadsheet

Is Your Home a Good Investment? • Deducting the interest payments from your annual income, reduces your overall taxes paid. Investing this amount, annually, earns $97K after 30 years (assume 4.0% ROI). • $842K + $97K = $939K compare to $956K by investing. Investing or home owning, neither is better nor worse • But, you can’t live inside your Market investments, or maybe you can live in your parents basement? • Play with the numbers. Assume market ROI of 5.0% and home only grows 3.0%, then Market investments come out ahead by $314K. • What’s the catch? Capital Gains Taxes! Single = $250K, Married = $500K tax deduction on home sale. But, not on Market investments. • See HomeMortgage spreadsheet

Should You Refinance? • There are two major costs to consider when refinancing: • The amount you’ve already paid (sum interest and principal) • The refinance loan costs (i.e., all fees, inspections, appraisals, etc.) • Balance these against the old and new loan total amounts paid. • For example: say you have a 3.875% $240K 30yr fixed loan that you’ve been paying for 12 months. If refi rates are now 2.875%, then compare: • After 12mos, you’ve paid $13.5K of which $4300 is on the principal and $9200 is the interest (monthly is $1129). Subtract $4300 from $240K equals $235,700. • Refi $235,700 at 2.875% gives a total cost of $352K (i.e., $235,700 + $116K interest). Resets to 30yrs, not 29. New monthly payment is $978. • Total original loan: $406K (i.e., $240K + $166K interest) • Compare: $406K vs. $366K (i.e., $352K + $13.5K); saving = $40K. • Still need to subtract loan fees, inspections, etc. which cost ~$5K. • You should refinance and save about $35K over 30 years. • If you can handle monthly payments of $1600, then switch to 15yr and save nearly $100K! • The lessons: • it’s the interest and length-of-loan period that costs big bucks • Watch out for how much you’ve already paid! • See HomeMortgage spreadsheet

Living Trust • A will is not enough. Your estate will still go to probate and cost thousands of dollars • Benefits of a Living Trust • The trust owns your assets, so when you die, the assets are still owned by the trust • Transfer of ownership to your beneficiaries is a simple legal cost of a couple hundred dollars • You are the trustee of your trust, so you control its assets, hence your assets • Typical Living Trust costs about $2K in lawyer and filing fees. • What goes in the trust? • Your home, your investments, old cars, checking account (if you carry a large balance and are single), etc. • Anything with a title. • Your will which indicates where you want non-titled assets to transfer, i.e., so and so gets the jewelry, or the furniture, etc. • 401(k), Life Insurance, IRAs, and perhaps other things that have the beneficiaries already named in the policies • Get a living trust as soon as you have a home and/or kids.

Picking an Investment Manager • People work well in their comfort zone and some will tell you anything in order to get your money. So, how to determine an investment manager’s capabilities? • Two types of investment managers: • Conservative: balances your entire portfolio of ETFs, mutual funds, 401(k), mortgage, IRAs, kids college, etc. and wants to get you ready for retirement • Aggressive: wants just some pile of your cash to invest in equities, hedge funds, etc. • Stick with the comfort zone • Your expectations should match the investment manager’s capabilities (e.g., conservatives never buy stocks) • Do not expect a conservative investment manager to perform aggressively (vice/versa too).

Picking an Investment Manager • Here’s 8 things to consider when picking an investment manager • Pay attention to taxes • Pay attention to fees • Quantify their past performance • Do they give pro and con advice? • Timing the market and cashing out at the highs • Do investment advisors buy stocks? • Big vs. Small funds • Some helpful tools

1. Taxes • Money made on investments is taxable. • Short-term gains = less than a year • Taxed at your income rate • Long-term gains = more than a year • Taxed at 20% starting in 2013 • Example: Invest $25K at age 40, how much will you have at age 65? • If both short and long term investing methods yield 5% ROI, then short term leaves you with $67K compared to long term at $73K. • But, if short term gains usually invested in higher ROIs and higher risks, so say 6% ROI. Then, make $81K, i.e., $8K better than long-term at 5%. • See Spreadsheet

2. Fees • Investment managers make money based on their fees (because they run your money) or based on an hourly advisory basis (because you run your money but need their advice). • Typically: 1% to 2% a year. Does this make a difference? YES! • $100K at 6.5% ROI, after 25 years yields $337K with a 1.5% fee or $380K with 1% fee. $43K savings is like a college education! • With no fee, you would have made $482K because fee is taken out quarterly, it reduces amount actually invested. • Fees are negotiable, usually graduated based on how much you have invested with the management team. • See Spreadsheet

3. Quantify Past Performance • When interviewing investment managers, ask them to give you their annual percentage gains, after fees, for the past 10 years as based on the investment method that they are suggesting is best for your needs. • They will either show you an actual 10 year record based on one of their existing clients or will put together a model based on the performance of their recommended stocks, bonds, ETFs, etc. Both of these are reasonableand expected given the reporting and regulatory rules. • There is NOTHING more important than this 10 year history when evaluating an investment team. • A good investment manager will regularly beat the market (e.g., S&P 500). • See Spreadsheet

4. Pro and Con Advice • Stay away from the narrow minded and ill informed investment managers • Annuities have been recommended to me as a way of making great ROIs, but it was never explained that the investment manager gets a kick-back, nor were the risks explained. • Some investment managers just offer the ETFs, funds, annuities, etc. that are partnered with their big institution. They have a narrow comfort zone. This is fine, so long as you understand this. • Some investment managers are not bound to large institutions, but also don’t have the breadth of information and research to make informed choices. This is fine, so long as you understand this.

5. Cash-Out at the Highs, Timing the Market • Its tough to make money in a flat market. So, should you time it? • Many investment managers will tell you to never time the market. Instead, they “rebalance” your portfolio. This is pretty much the same as timing the market. • Buy Low Sell High is timing the market. Just a matter of how much time goes by. See first slides on the market over the past 100 years. • This “amount of time” is incredibly difficult to know! There are ways to understand the fluctuations in the market or in individual companies, but this is for the professionals. • See SP500 tab in DJIA spreadsheet • Sell in March 2000, Buy in Oct 2002, Sell in Sept 2007, Buy in Feb 2009, Sell in Feb 2012. Is a 249% gain in 12 years! $25K would have become $87K. • Are you really that prescient?

6. Do Investment Advisors Buy and Sell Stocks? • No. • Its too difficult for them to know all of the companies and their mechanisms of profit and loss, the position of the company with respect to their competition, the technicals and fundamentals of the company, and so on. • It’s easier for investment advisors to add new clients and thus grow the advisors income, rather than grow an individual client’s portfolio via equities. • Instead, they do Sector Analysis • Buy ETFs, mutual funds, bonds that are from well performing market sectors, sell them (rebalance) when sector underperforms. See Morningstar reports. • They use models to designate risk vs. return. Don’t want too much risk yet low return. • Example: an investing team that I’ve hired created a model using this approach where we would have earned 6.5% after fees for the past 10 years. A nice 2X performance.

7. Big vs. Small Funds • Big Mutual Funds • Are around $10B in size • Can buy and sell a $100M company with little positive or negative impact on the $10B (e.g.,the company is just 1% of the fund) • Small Mutual Funds • Are around $1B in size • Can buy and sell a $100M company with significant positive or negative impact on the $1B (e.g., the company is 10% of the fund) • Neither is better or worse, just different risk tolerances and performances for the same purchase.

8. Tools To Help You Search and Learn • Morningstar http://www.morningstar.com • Get a free account • Learn how to read their 3x3 box representing sectors of the market. • They have performance scores for all kinds of investments. Indicate how much $10K would have advanced or lost over 10 years. • Lots of others • http://www.marketwatch.com/ • http://finance.yahoo.com/ • http://research.stlouisfed.org/ • http://www.onlinebrokerrev.com • http://online.barrons.com • http://online.barrons.com

Finding an Investment Manager • The Three Step Process to Finding and Selecting and Investment Advisor • 1. Use online reviews, I like Barron’s annual reviews for all U.S. and top 20 or so in each state. • Some have a hard low-end investment amount, most do not, even though they say they do. • Select a half dozen or so • 2. Review their SEC reports! • If manager is not listed, then run away! • Avoid people with disputes, they are poor communicators • 3. Use SEC reports to determine, are you their typical client? Remember the comfort zone. • Email them with a one paragraph inquiry, if they don’t respond, cross them off the list. If they respond, but after several days, cross them off the list. • Ask specific questions in follow-up email. Try to identify their comfort zone • Do you rebalance sectors or do you focus on stocks? • Which approach do you use for your own investments? • Are my moneys in the same pool as your own moneys? • Do you manage my money or one of your team members? • Are all of your clients in the same pool of investments? • What are your annual returns over the past 1, 5, 10, and 20 year periods? • How are you compensated?

Interviewing an Investment Manager • Email responses could be vague. That’s OK, the manager doesn’t know you yet. You could be a wackadoodle, or a competitor. • Meeting in person: first two meetings are free. • Your goal is to get quantitative during the meeting(s). • They’ll want to be your best friend, ugh! • Quantitative: • Critical: get their performance over the past 10 years. • I used a spreadsheet and two investment scenarios. Your goal is to determine their comfort zone. Most will be comfortable providing small ROIs, some will claim they can do large ROIs but is not routine, few will be able to prove they can do large ROIs. • See spreadsheet, ROI tab • Spreadsheet is your and their scorecard used to evaluate performance at the end of each year. • How much time is needed to hit this annually averaged mark (CAGR)? • Some will want to perform a total financial portfolio and run all of your assets for you. • For now, don’t muddy the waters with all this additional stuff. • Now is not the time for “kumbayah” • Too much emphasis on trust makes me skeptical, is that how they make money, i.e., by adding new clients rather than growing your wealth?

Concluding Thoughts • Buy Low Sell High • You are smart enough to handle your personal finances, but are you too busy to do the daily grind? • Be quantitative with investment managers and with yourself; know their comfort zone and know yours too.