Download

1 / 47

1.38k likes | 3.25k Views

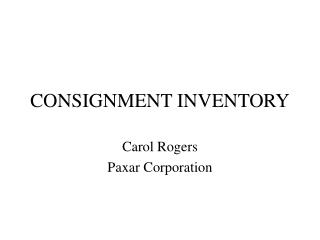

Consignment. Consignor (Owner of the goods). Goods. Consignee (Agent). Net proceeds + Account sales. Consignment account Goods sent on Consignment account Consignee account. Consignor account. Consignment. Nature of a consignment.

E N D

Consignor (Owner of the goods) Goods Consignee (Agent) Net proceeds + Account sales • Consignment account • Goods sent on • Consignment account • Consignee account • Consignor account Consignment

Nature of a consignment • If the owner of the goods does not have retail outlets, he can consign the goods to an agent. • The agent will sell the goods for him and receive a commission in return.

Consignor • The owner of the goods who sends the goods to an agent for sale. • Consignee • Who sells the goods for the consignor. • Sells the goods and collects the money from the customers. • Will pay the consignor the net proceeds (Proceeds – Expenses – Commission) and provide the consignor an account sales showing all the proceeds and expenses.

Goods sent on consignment • Goods sent on consignment are the property of the consignor until the goods are sold. • The consignor should include all the unsold goods on consignment in his closing stock.

Consignor’s Books • Consignment account • It is a profit and loss account for the consignment. Consignment Account Expenses Income

Consignee Account 2. Consignee account Amount owing form consignee e.g. Sales Amount owing to consignee e.g. Expenses, commission

3. Goods sent on consignment account Goods sent on consignment account Transferring to trading account Cost of goods sent

Goods sent on consignment account • $ • Trading x • $ • Consignment x

Consignment • $ • Goods sent on consignment x • Banks-consignor’s expenses x • Consignee- consignee’s • expenses x • consignee’s • commission x • P & L-profit on consignment x • x • $ • 4. Consignee-sales x • 6. Bank/Insurance Co.-claim x • 6. Bank/Insurance Co.-claim x • 7. Profit and Loss-net stock loss x • _ • x

Consignee • $ • Consignment-sales x • _ • x $ 3. Consignment-consignee’s expenses x consignee’s commission x 8. Bank-settlement from consignee x x

Consignee $ Consignment-sales 18,000 ______ 18,000 $ Consignment-expenses 2,400 -commission 1,800 8. Bank 13,800 18,000

E. Bad debts of Consignments • A consignee(agent) sells goods and collects money on behalf of the consignor. • If he can’t collect the debts, these debts should be treated as the bad debts of the consignor. Accounting entries in the books of the consignor: Dr Consignment Cr Consignee

Consignment $ Consignee-bad debts x Consignee $ Consignment-bad debts x

If a consignee receives an additional commission (del credere commission), he must bear all the losses from the bad debts. • In case of a bad debts arising from sales of goods on consignment, no entry is required in the books of the consignor.

Accounting entries in the books of the consignee Dr Bad debts Cr Debtors (with the bad debts borne by the consignee personally)

Valuation of stock • If there are unsold goods on consignment at the end of the accounting period, the value of the unsold stock will be carried down to the following period.

Consignment $ Year 1 x x Year 2 Balance b/d x $ Year 1 Balance c/d – value of unsold stock x x

Valuation of stock = Consignor’s Cost +Consignee’s Expenses

Consignor’s cost = Total consignor’s cost * Units of closing stock / Total units of goods SENT on consignment = [Cost of goods on consignment + Consignor’s expenses] * Units of closing stock / Total units of goods SENT on consignment

Consignee’s expense = Total consignees expenses (excluding marketing expenses) * Units of closing stock / Total units of goods RECEIVED by consignee (after normal loss) • Marketing expenses e.g. advertising expenses,ordinary commission,del credere commission, salesmen’s salaries, bad debts, discounts allowed, delivery charges(to customers), selling expenses, distribution expenses.

Consignment $ Goods on Consignment 60,000 Chan – sales 94,000 (500+440)*$100 Bank - freight 500 - insurance 200 Chan – port charges 700 - delivery charges to warehouse 1,280 - advertising 1,000 - delivery charges to customer 900 - dis. allowed 320 - ordinary com. 4,700 ($94000*5%) - del credere com. 500 (50000*1%)

Workings Value of the stock loss (10 boxes) Stock loss = (1,000 * $60 + $500 +$200) * 10/1,000 = $607

Consignment $ Goods on Consignment 60,000 Chan – sales 94,000 (500+440)*$100 Bank - freight 500 - insurance 200 Bank – claim 300 Profit and Loss – stock loss 307 (607-300) Chan – port charges 700 - delivery charges to warehouse 1,280 - advertising 1,000 - delivery charges to customer 900 - dis. allowed 320 - ordinary com. 4,700 ($94000*5%) - del credere com. 500 (50000*1%)

Value of the Closing StockConsignor’s Cost: ($1,000 * $60 + $500 + $200) * 50/1,000 3,035Consignee’s Expenses:($700 + $1,280) * 50/990 1003,135 Workings

Consignment $ $ Goods on Consignment 60,000 Chan – sales 94,000 (500+440)*$100 Bank - freight 500 - insurance 200 Bank – claim 300 Profit and Loss – stock loss 307 (607-300) Chan – port charges 700 - delivery charges to warehouse 1,280 - advertising 1,000 - delivery charges to customer 900 - dis. allowed 320 - ordinary com. 4,700 ($94000*5%) - del credere com. 500 (50000*1%) Balance c/d 3,135 Profit and Loss – Profit on consignment 27,642 97,742 97,742

Chan $ $ • Consignment • port charges 700 • delivery changes to • warehouse 1,280 • advertising 1,000 • delivery charges to • customers 900 • dis. allowed 320 • ordinary com. 4,700 • del credere com. 500 Consignment - sales 94,000 Bank 84,600 94,000 94,000

Consignee’s books • A consignee collects sales proceeds and pays expenses on behalf of the consignor. • A consignor account should be maintained to record the money due to or due from the consignor.

Consignor Account $ Bank – consignee’s expenses x Commission Received x - ordinary x - del credere x Debtors – dis. allowed x Debtors – bad debts x Bank / Bill payable – to consignor x x $ Bank – sales x Debtors – sales x _ x

Example The facts are the same as in the pervious example, but the transaction would be shown in the books of consignee. In Chan’s Books Tang – Consignor Account $ $ Debtor – sales (500 x $100) 50,000 Bank -port charges 700 -delivery changes to warehouse 1,280 -advertising 1,000 -delivery charges to customers 900 Bank – sales (440 x $100) 44,000 • Commission Received • ordinary 4,700 • Del credere 500 Bank – to consignor 84,600 94,000 94,000

Consignments and the Final AccountsThe accounts related to a consignment would be disclosed in the final accounts as follows:

In Consignor’s Book Trading and Profit and Loss Account $ $ $ Sales N Opening Stock N Add Purchases T LessGoods on Consignment C N N Less Closing Stock N Cost of Goods Sold N Gross Profit N N Expenses N Stock Loss of Consignment C Net Profit T N Gross Profit N Consignment Profit C T T N=figure from normal trading; C=figure from Consignment T= Total figures

Balance Sheet (Extract) $ $ Current Assets Stock (N+C) T Consignee Account (if it is a debit balance) C Current Liabilities Consignee Account (if it is a credit balance) C OR

In Consignee’s BookThe only entries needed is for the commission received. Trading and Profit and Loss Account $ $ $ Sales N Opening Stock N Purchases N N Less Closing Stock N Cost of Goods Sold N Gross Profit N N Expenses N Bad Debts N Bad Debts(If he has received a del credere commission, he will bear the Consignment’s bad debts) C Net Profit T N Gross Profit N Commission Received (from consignor) C T T

Balance Sheet (Extract) $ $ Current Assets Stock N Consignor Account (if it is a debit balance) C Current Liabilities Consignor Account (if it is a credit balance) C OR

Consignments and Joint Ventures: • If the party to a joint venture sends some goods to an agent for sale, the transactions will be entered as follows: • No consignment account is openedIf no consignment account is kept, all the transactions of the consignements should be recorded in the foint venture account. • A consignemnt account is opened

(i) No consignment account is opened Joint Venture Account $ $ Bank – joint venture expenses X Bank – consignment expenses incurred by the consignor X Consignee – consignment expenses incurred by the consignee X Profit and Loss – share of profit X Bank – settlement X Bank – joint venture sales X Consignee – consignment sales X Stock c/d – unsold stock of joint venture and consignment X X X

Memorandum Joint Venture Account $ $ Expenses – joint venture and consignment X Share of Profit: A X B X X Sales – joint venture and consignment X Stock c/d – joint venture and consignment X X X

(ii) A consignment account is opened Joint Venture Account $ $ Bank – joint venture expenses X Profit and Loss – share of profit X Bank – settlement X Bank – joint venture sales X Goods Sent on Consignment X Consignment – profit X Stock c/d – unsold stock of joint venture only X X X

Consignment Account $ $ Goods Sent on Consignment X Bank – expenses X Consignee – expenses X Joint Venture – consignment profit X Sales – joint venture only X Goods Sent on Consignment X Consignment – profit X Stock c/d – joint venture only X X X

Memorandum Joint Venture Account $ $ Expenses – joint venture only X Share of Profit: A X B X X Sales – joint venture only X Goods Sent on Consignment X Consignment – profit X Stock c/d – joint venture only X X X