Download

1 / 25

250 likes | 507 Views

Feld, Hyde, Wertheimer, Bryant & Stone, P.C. 2000 SouthBridge Parkway, Suite 500 Birmingham, AL 35209 Phone: 205.802.7575 Fax: 205.802.7550 Web site: http://www.feldhyde.com. Captive Insurance Companies and the Closely-Held Business. James J. Coomes, Esq.

E N D

Feld, Hyde, Wertheimer, Bryant & Stone, P.C. 2000 SouthBridge Parkway, Suite 500 Birmingham, AL 35209 Phone: 205.802.7575 Fax: 205.802.7550 Web site: http://www.feldhyde.com Captive Insurance Companies and theClosely-Held Business James J. Coomes, Esq. FELD HYDE WERTHEIMER BRYANT & STONE, P.C. ATTORNEYS AT LAW Birmingham Estate Planning Council October 1, 2009

What is a Captive Insurance Company? • A Captive insurance company is an insurance company formed primarily or exclusively to insure the risks of one or more affiliated businesses. • There are many types of captives, however, the materials contained herein focus on captive insurance companies that insure property and casualty risks of affiliated closely held businesses (i.e., business risk insurance) through the issuance of insurance policies in return for premium payments; and • The Captive insurance company is owned by one or more of the owners of the affiliated closely held business (and/or the heirs of the owners).

Lets Talk About Insurable Risks Some traditional risks • General liability (includes property) • Errors and omissions • Directors and officers • Employment practices • Employee fidelity • Construction defects • Subcontractor default • Workers compensation

Lets Talk About Insurable Risks Some non-traditional risks • Deductibles • Administrative actions • Data breach/cyber risk • Loss of key customer • Loss of key supplier • Loss of key employee • Litigation expenses • Business interruption • Tax audit • Product recalls • Loss of franchise agreement • Subcontractor default • Terrorism • Earthquake • Mold • Kidnap, ransom • Accounts Receivable • Intellectual property

Reasons to Form a Captive • Underwrite risks that are presently being self insured (i.e., those that are not presently being insured by a third party) • Underwrite risks that are presently being insured by third party insurance companies • Underwrite risks that are difficult to obtain or are expensive • Tailor insurance policies to specific needs • Risk management incentives • Greater control over claims • Share in underwriting profits • Tax benefits • Asset protection benefits • Estate Planning opportunities

Taxation of Captives • Captives are formed as C corporations and are subject to Chapter C and Chapter L of the Internal Revenue Code. • Business risk insurance premiums paid by a business to a Captive are a deductible business expense. IRC Section 162. T.R. Section 1.162-1(a) • The premiums received by a Captive “may” be income tax-exempt.

Did You Say Tax Advantage? - continued • The Internal Revenue Code provides a certain “tax advantage” to small property and casualty insurance companies depending on the amount of annual premiums it receives. • Property and casualty insurance companies with annual premiums of $1.2 million or less can elect to be taxed only on net investment income under IRC Section 831(b).

Did You Say Tax Advantage? - continued • Income tax consequences of an “831(b)” election: • Investment income earned on assets owned by the Captive is taxable at ordinary C Corporation rates. • Premiums received by the Captive are income tax free. • Only investment related expenses may be deducted by the Captive. • So is the 831(b) election really a “tax advantage”?

Some Ground Rules • The Captive must be respected as a valid insurance company for federal income tax purposes. • What “ground rules” must be followed?

Some Ground Rules - continued • The Captive must be operated as a bona-fide insurance company. • The Captive must be respected and treated as a separate entity (i.e., separate books, records and accounts, no commingling of assets with personal funds or funds of other entities, etc.). • Insurance policies issued by the Captive must be commercially reasonable with respect to their terms (including premiums). • The Captive must comply with capitalization, surplus, investment and other regulatory requirements of the jurisdiction in which the Captive is domiciled.

Some Ground Rules - continued • Risk distribution must be present. • The Captive must insure a sufficient number of insureds: • Revenue Rulings 2002-90 and 2005-40: 12 insureds is enough. • Case Law: 8 insureds is enough. • Third party risk pools are available for those Captive insurance companies that do not meet the safe harbor ruling.

Jurisdiction: Onshore vs. Offshore • Fees (both startup and ongoing) • Capitalization requirements • Margin of solvency requirements • Investment restrictions • Degree of regulation • Premium taxes • Income taxes • Federal excise tax (offshore only but does not apply if IRC Section 953(d) election is made) • But aren’t there income tax advantages to forming offshore? • NO , NO and NO!!! • Captive will elect to be treated as a U.S. Corporation for federal tax purposes. IRC Section 953(d)

Typical Ownership Structures Publicly Held Company Parent Corporation Captive Insurance Company

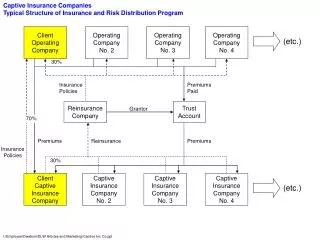

Closely Held Companies Individual Owners Jack and Joe Individual Owners Jack and Joe $400,000 in premiums Closely Held Business Captive Insurance Company Insurance policies/claims paid • Business receives $400,000 ordinary business deduction. • Captive insurance company receives $400,000 income tax free.

Closely Held Companies Jack and Joe Children of Jack and Joe (or trust FBO children) $400,000 in premiums Closely Held Business Captive Insurance Company Insurance policies/claims paid • Business receives $400,000 ordinary business deduction. • Captive insurance company receives $400,000 income tax free. • Premium payment should not represent a gift to heirs for gift tax purposes.

Closely Held Companies Jack and Joe GST Trust FBO heirs of Jack and Joe $400,000 in premiums Closely Held Business Captive Insurance Company Insurance policies/claims paid • Business receives $400,000 ordinary business deduction. • Captive insurance company receives $400,000 income tax free. • Premium payment should not represent a gift to heirs for gift tax or generation skipping tax purposes.

Closely Held Companies Jack and Joe Key Employees of Closely Held Business $400,000 in premiums Closely Held Business Captive Insurance Company Insurance policies/claims paid • Business receives $400,000 ordinary business deduction. • Captive insurance company receives $400,000 income tax free.

How are assets of the Captive Insurance Company Invested? • Recall that the Section 831(b) captive insurance company is taxed on its investment income at C corporation rates. • Subject to applicable regulatory restrictions, the captive insurance company may invest in the following: • Money market funds, CDs, etc. • Stocks/Bonds • Real Estate • Closely held Businesses • Life Insurance

How do the owners of the insurance company benefit from the profits earned by the insurance company? • Dividends • Taxed at 15% federal rate. IRC Section 1(h) • Liquidation • Taxed at 15% federal rate plus C corporation tax rates on the net appreciation of the assets owned by the insurance company. IRC Sections 331 and 336

THANK YOU Under requirements imposed by the IRS, any advice concerning one or more U.S. federal tax issues contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to another party any transaction or tax-related matter addressed herein. 75031006\PPT\90142