Download

1 / 7

80 likes | 303 Views

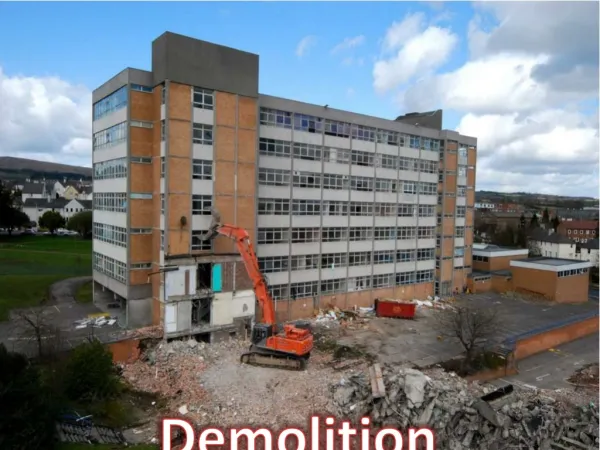

Demolition of ships. At the beginning of 2009, there were 99,741 commercial vessels of 100 GT and above.

E N D

At the beginning of 2009, there were 99,741 commercial vessels of 100 GT and above. • During the year, 3,658 new vessels were delivered (+3.7 per cent of the existing fleet at the beginning of the year, in terms of vessel numbers), while 1,205 ships were withdrawn and mostly demolished (a reduction of 1.2 per cent from the existing fleet). • The resulting fleet total in January 2010 amounted to 102,194 ships (+2.5 per cent compared to January 2009)

The market for ship demolition – also called scrapping or recycling – is far more volatile than the market for shipbuilding, as ships can be sold for demolition at short notice. • In periods when freight and charter rates are high, shipowners are very reluctant to withdraw any ships from the market, while in times of low demand for maritime transport, owners are much more inclined to sell their ships to scrap yards. • The disadvantage of selling in times of low demand is that prices for scrap metal are very low. Between mid-2008 and early 2009, the price for scrap metal had fallen from around $650 per light displacement ton (ldt) to just $200. Since then, the price has recovered, reaching about $400 in March 2010.

The tonnage on order as at 31 December 2009 consisted of 258.3 million dwt of dry bulk carriers (54.5 per cent of the total world deadweight tonnage on order), • 109.3 million dwt of oil tankers (23.1 per cent), • 15 million dwt of general cargovessels(3.2 per cent), 53.9 million dwt of container ships (11.4 per cent) and • 37.4 million dwt of other vessel types (7.9 per cent). • The total tonnage on order stood at 9,222 vessels, with a combined capacity of 474 million dwt.