Download

1 / 13

160 likes | 316 Views

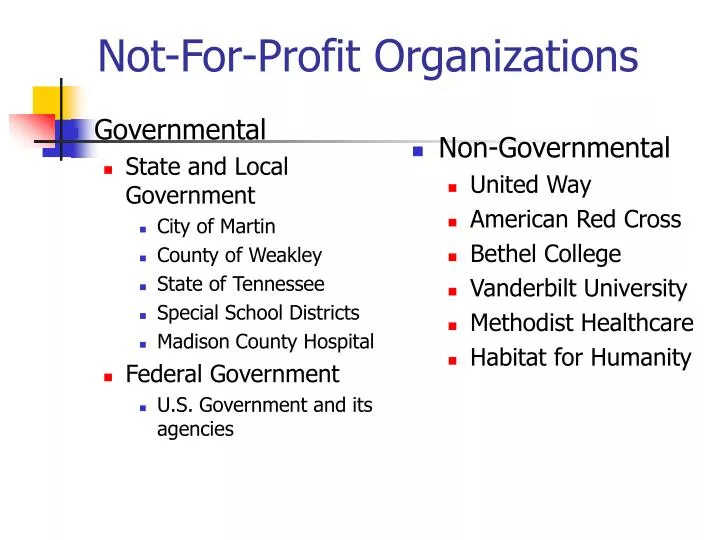

Governmental State and Local Government City of Martin County of Weakley State of Tennessee Special School Districts Madison County Hospital Federal Government U.S. Government and its agencies. Non-Governmental United Way American Red Cross Bethel College Vanderbilt University

E N D

Governmental State and Local Government City of Martin County of Weakley State of Tennessee Special School Districts Madison County Hospital Federal Government U.S. Government and its agencies Non-Governmental United Way American Red Cross Bethel College Vanderbilt University Methodist Healthcare Habitat for Humanity Not-For-Profit Organizations

Definition of a Government • Popular election or appointment by popular elected officials • Potential for unilateral dissolution by government • Power to tax • Power of Issuance of tax exempt debt directly

Governmental State and Local Objectives GAAP Hierarchy (pp. 4-5) GASB is King (Queen) Federal Objectives GAAP Hierarchy (pp. 4-5) FASAB is King (Queen) Non-Governmental Objectives (p. 6) GAAP Hierarchy (pp. 4-5) FASB is King (Queen) Recent FASB Activity Little until middle 1990s SFAS 116, 117, 118, 121 changed this inactivity Financial Reporting-NFPs

State and Local Government • Financial Reporting • User considerations are much more diverse • Investors and creditors • Legislative and oversight officials • Political and social decisions as well as economic • Measurement Focus • Economic resources • Flow of current financial resources

State and Local Government • Basis of Accounting • Accrual • Modified Accrual • Method of Reporting • Comprehensive Annual Financial Report • Sections of CAFR • Introductory • Financial • Statistical

Exchange and Non-exchange Transactions • Exchange • Each party receives and gives up equal values • City cleans up privately owned property and bills the owner for the service • Non-Exchange • One party does not receive proportionate value for value given up • Property tax revenue

Financial Statements • Government-Wide • Accrual basis of accounting • Economic resources measurement focus • Statement of Net Assets • Statement of Activities • Fund: A fiscal and accounting entity • Modified accrual basis of accounting • Flow of current financial resources measurement focus • Each fund is a self-balancing set of accounts

Fund Financial Statements • Governmental Funds • Balance Sheet • Statement of Revenue, Expenditures, and Changes in Fund Balances • Proprietary Funds • Statement of Net Assets • Statement of Revenue, Expenses, and Changes in Fund Net Assets • Statement of Cash Flows

Fund Financial Statements • Fiduciary Funds • Statement of Fiduciary Net Assets • Statement of Changes in Net Fiduciary Assets • Special Considerations • Differences in measurement focus and basis of accounting between Government-Wide and Fund Financial Statements require reconciliation schedules • Fiduciary Fund Statements are not included in the Government-Wide financial statements

Governmental General Special Revenue Capital Projects Debt Service Permanent Proprietary Funds Enterprise Internal Service Fiduciary Funds Agency Pension Trust Investment Trust Private-Purpose Trust Types of Governmental Funds

Governmental Funds and Budgeting • Required for governmental type funds • Optional for proprietary type funds • Adopted by the legislative body • Entered into the accounting records in reverse debit/credit approach • A part of appropriate financial statements and/or schedules

Accounting for Capital Assets and Infrastructure • Long-lived assets • All (except collections of works of art and historical treasures) must be capitalized and depreciated on government-wide and proprietary fund financial statements • Capital assets and related depreciation expense do not appear on governmental type fund financial statements • More elaborate discussion in next chapter

Long-Term Debt • Payable more than one year from Statement of Net Assets Date • All entity long-term debt must be reported on the Statement of Net Assets (GW) • Governmental type funds do not report long-term debt on financial statements (Flow of current financial resources measurement focus)