Download

1 / 39

390 likes | 566 Views

Stockholders’ Equity. Chapter 10 . 10- 2. Learning Objectives. Identify the advantages and disadvantages of the corporate form of ownership Record the issuance of common stock Contrast preferred stock with common stock and bonds payable Account for treasury stock

E N D

Stockholders’ Equity Chapter 10

10-2 Learning Objectives • Identify the advantages and disadvantages of the corporate form of ownership • Record the issuance of common stock • Contrast preferred stock with common stock and bonds payable • Account for treasury stock • Describe retained earnings and record cash dividends

10-3 Learning Objectives • Explain the effect of stock dividends and stock splits • Prepare and analyze the stockholders’ equity section of a balance sheet and the statement of stockholders’ equity • Evaluate company performance using information on stockholders’ equity

10-4 Part A Invested Capital

10-5 Learning Objective 1 Identify the advantages and disadvantages of the corporate form of ownership

10-6 Corporations • Articles of incorporation: corporate charter describing: • Nature of business activities • Shares of stock to be issued • Initial board of directors • The board of directors establish corporate policies and appoints officers who manage the corporation

10-7 Stages of Equity Financing • Corporations first raise money from founders of the business, friends, and family • To grow, companies seek investments from: • Angel investors • Venture capital firms • Initial public offering (IPO)

10-8 Public or Private Public Private • Allows public investment • Many shareholders • Stocks trade on stock exchanges or by over-the-counter (OTC) trading • Regulated by the (SEC) • Examples—Wal-Mart, Microsoft, Intel • Does not allow investment by the general public • Fewer stockholders • Stocks not traded in the open market • Not regulated by the (SEC) • Examples—Cargill (agricultural commodities) Koch Industries (oil and gas), Chrysler (cars)

10-9 Learning Objective 2 Record the issuance of common stock

10-10 Common Stock • Treasury stock: repurchased shares, included as part of shares issued, but excluded from shares outstanding

10-11 Par Value • Legal capital per share of stock that’s assigned when the corporation is first established • Has no relationship to the market value today

10-12 Accounting for Common Stock Issues

10-13 Learning Objective 3 Contrast preferred stock with common stock and bonds payable

10-14 Preferred Stock • Issued in addition to common stock to attract wider investment • Preferred stockholders have: • First rights to a specified amount of dividends • Preference over common stockholders in the distribution of assets at the time of dissolution • Most preferred stock does not have voting rights

10-15 Features of Preferred Stock • Flexibility allowed in its contractual provisions • Types: • Convertible: shares can be exchanged for common stock • Redeemable: shares can be returned to the corporation at a fixed price • Cumulative: shares receive priority for future dividends, if dividends are not paid in a given year • Dividends in arrears - unpaid dividends

10-16 Learning Objective 4 Account for treasury stock

10-17 Treasury Stock • Corporation’s own stock that it has reacquired • Companies buy back their own stock for various reasons: • To boost underpriced stock • To distribute surplus cash without paying dividends • To boost earnings per share • To satisfy employee stock ownership plans

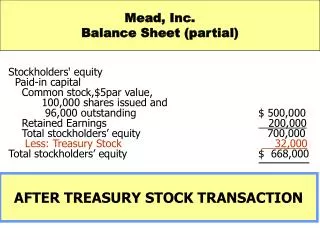

10-18 Purchase of Treasury Stock

10-19 Illustration 10.11—Stockholders’ Equity before and after Purchase of Treasury Stock

10-20 Reissuing Treasury Stock

10-21 Reissuing Treasury Stock

10-22 Part B Earned Capital

10-23 Learning Objective 5 Describe retained earnings and record cash dividends

10-24 Retained Earnings • Earnings retained in the corporation and not paid out as dividends • Equals all net income, less all dividends • Has a normal credit balance • Accumulated deficit: a debit balance in retained earnings

10-25 Dividends • Distributions by a corporation to its stockholders • Declaration date: date on which board of directors declare the cash dividend to be paid • Record date: specific date on which the company will determine who will receive the dividend (registered owners of stock) • Payment date: date of the actual cash distribution

10-26 Recording Cash Dividends

10-27 Learning Objective 6 Explain the effect of stock dividends and stock splits

10-28 Stock Dividends and Stock Splits • Stock dividends: additional shares of a company’s own stock given to stockholders as dividends • Stock split: a large stock dividend that includes a reduction in the par or stated value per share Small stock dividend Large stock dividend or stock split (2-for-1)

10-29 Stock Splits or Large Stock Dividends • Stock split • Reduces par value per share and increases shares outstanding • No need to record transaction • Large stock dividends • Records an increase in common stock and decrease in retained earnings • Recorded at par value

10-30 Small Stock Dividends • Recorded at market value • Believed to have little impact on market price

10-31 Part C Reporting Stockholders’ Equity

10-32 Learning Objective 7 Prepare and analyze the stockholders’ equity section of a balance sheet and the statement of stockholders’ equity

10-33 Statement of Stockholders’ Equity • Summarizes the changes in the balance in each stockholders’ equity account over a period of time

10-34 Learning Objective 8 Evaluate company performance using information on stockholders’ equity

10-35 Return on Equity • Measures the ability of company management to generate earnings from the resources that owners provide

10-36 Return on the Market Value of Equity • Analysts often relate earnings to the market value of equity Net income Return on the market value of equity = Market value of equity

10-37 Earnings per Share • Measures net income earned per share of common stock • Useful in comparing earnings performance for the same company over time • Not useful for comparing earnings performance of one company with another

10-38 Price-Earnings Ratio • Indicates how the stock is trading relative to current earnings • Commonly are in the range of 15 to 20 • Growth stocks: stocks whose future earnings investors expect to be higher • Value stocks: stocks that are priced low in relation to current earnings

10-39 End of Chapter 10