Download

1 / 34

370 likes | 509 Views

Options. Wiggs Civitillo. Basic Function. a contract between two parties concerning the buying or selling of an asset at a reference price

E N D

Options Wiggs Civitillo

Basic Function a contract between two parties concerning the buying or selling of an asset at a reference price The buyer of the option gains the right, but not the obligation, to engage in some specific transaction on the asset, while the seller incurs the obligation to fulfill the transaction if so requested by the buyer.

Price price of an option derives from the difference between the reference price and the value of the underlying asset (commonly a stock, a bond, a currency or a futures contract) plus a premium based on the time remaining until the expiration of the option

Terminology Call: an option that conveys the right to buy something Put: an option that conveys the right to sell something Strike/exercise price: reference price at which asset could be traded Exercising an option: trading an option at the agreed price Spot Price: Market price of asset

Expiration Most options have expiration dates after which they become void and worthless

Term Sheet whether the option holder wants a call or put option the quantity and class of the underlying asset (ex: 100 shares of Co. B stock) the strike price the expiration date (the last date the option can be exercised) the settlement terms, for instance whether the writer must deliver the actual asset on exercise, or may simply tender the equivalent cash amount the total amount to be paid by the holder to the writer of the option.

Types of Options Many options are created in standardized form and are traded in an anonymous options exchange over-the-counter options are customized to the desires of the buyer

Standardized Options • stock options • commodity options • bond options and other interest rate options • stock market index options or, simply, index options • options on futures contracts • callable bull/bear contract • derivative that provides investors with a leveraged investment

Embedded Options Callable bond allows the issuer to buy back the bond at a predetermined price at certain time in future. Callable bonds cannot be called for the first few years of their life. This period is known as the lock out period. Puttable bond allows the holder to demand early redemption at a predetermined price at certain time in future. Convertible bond allows the holder to demand conversion of bonds into the stock of the issuer at a predetermined price at certain time period in future. Extendible bond allows the holder to extend the bond maturity date by a number of years. Exchangeable bond allows the holder to demand conversion of bonds into the stock of a different company, usually a public subsidiary of the issuer, at a predetermined price at certain time period in future.

Bond Option Example Trade Date: 23 Jan, 2011 Maturity Date: 28 Jan, 2013 Option Buyer: Bank A Underlying asset: ABC Bond Spot Price: $101 Strike Price: $110 On the Trade Date, Bank A enters into an option with Bank B to buy certain ABC Bonds from Bank B for the Strike Price mentioned. Bank A pays a premium to Bank B which is the premium percentage multiplied by the face value of the bonds. At the maturity of the option, Bank A either exercises the option and buys the bonds from Bank B at the predetermined strike price, or chooses not to exercise the option. In either case, Bank A has lost the premium to Bank B.

OTC (Over the counter) • interest rate options • currency cross rate options, and • options on swaps or swaptions • Swaptions: options on interest rate swaps.

Swaption Example Wiggs is in Mexico and is aware of an upcoming election. He has some variable rate bonds that are paying very well, but would like to hedge against the risk of political upheaval. Jake is in the UK, and rates are low and constant. Jake would like some extra money and thinks that political change will not affect the rates too significantly. In this case, Wiggs would wish to purchase a swaption from Jake. Wiggs and Jake engage in a swap; Wiggs obtains fixed cash flows from the UK bond and Jake obtains the variable rate bonds. They agree on terms that set the swap as even money (present valued) for both of them. However, they do not do the swap yet because Wiggs’ debt is about to expire, he plans to reinvest, and he wants to do the swap only if the variable rates drop below a threshold (at which point his income decreases; he wants to lock in profits). In order to lock in the profits, Wiggs is willing to arrange the option on slightly favorable terms with Jake. Jake wants the higher temporary cash flow and is willing to accept the small risk that the variable rates may drop. In this case, the swaption can be exercised and both people may still make a profit, depending on the timing and amounts involved. At the very least, both parties either reduced or enhanced their risks/rewards as they desired.

Option Styles European option - an option that may only be exercised on expiration. American option - an option that may be exercised on any trading day on or before expiry. Bermudan option - an option that may be exercised only on specified dates on or before expiration. Barrier option - any option with the general characteristic that the underlying security's price must pass a certain level or "barrier" before it can be exercised Exotic option - any of a broad category of options that may include complex financial structures. Vanilla option - any option that is not exotic.

Valuation Models The current market price of the underlying security, the strike price of the option, particularly in relation to the current market price of the underlier (in the money vs. out of the money), the cost of holding a position in the underlying security, including interest and dividends, the time to expiration together with any restrictions on when exercise may occur, and an estimate of the future volatility of the underlying security's price over the life of the option.

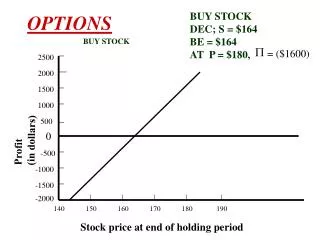

Long Call A trader who believes that a stock's price will increase might buy a call option rather than just purchase the stock itself. If the stock price at expiration is above the exercise price by more than the premium (price) paid, he will profit. If the stock price at expiration is lower than the exercise price, he will let the call contract expire worthless, and only lose the amount of the premium. A trader might buy the option instead of shares, because for the same amount of money, he can control (leverage) a much larger number of shares.

Short Call A trader who believes that a stock price will decrease, can sell the stock short or instead sell, or "write," a call. The trader selling a call has an obligation to sell the stock to the call buyer at the buyer's option. If the stock price decreases, the short call position will make a profit in the amount of the premium. If the stock price increases over the exercise price by more than the amount of the premium, the short will lose money, with the potential loss unlimited.

Short Put A trader who believes that a stock price will increase can buy the stock or instead sell a put. The trader selling a put has an obligation to buy the stock from the put buyer at the put buyer's option. If the stock price at expiration is above the exercise price, the short put position will make a profit in the amount of the premium. If the stock price at expiration is below the exercise price by more than the amount of the premium, the trader will lose money, with the potential loss being up to the full value of the stock.

Butterfly Spread limited risk, non-directional options strategy that is designed to have a large probability of earning a small limited profit when the future volatility of the underlying is expected to be different from the implied volatility.

Long Butterfly • A long butterfly position will make profit if the future volatility is lower than the implied volatility. • Long 1 call with a strike price of (X − a) • Short 2 calls with a strike price of X • Long 1 call with a strike price of (X + a) • Or: • Long 1 put with a strike price of (X + a) • Short 2 puts with a strike price of X • Long 1 put with a strike price of (X − a)

Short Butterfly A short butterfly position will make profit if the future volatility is higher than the implied volatility. A short butterfly options strategy consists of the same options as a long butterfly. However all the long option positions are short and all the short option positions are long.

Iron Condor buy (long) options contracts for the outer strikes using an out-of-the-money put and out-of-the-money call. The trader will also sell or write (short) the options contracts for the inner strikes, again using an out-of-the-money put and out-of-the-money call. The difference between the put contract strikes will generally be the same as the distance between the call contract strikes. Since the premium earned on the sales of the written contracts is very likely greater than the premium paid on the purchased contracts, a long Iron Condor is typically a net credit transaction. This net credit represents the maximum profit potential for an Iron Condor. The potential loss of a Long Iron Condor is the difference between the strikes on either the call spread or the put spread (whichever is greater if it is not balanced) multiplied by the contract size (typically 100 or 1000 shares of the underlying instrument), less the net credit received.

Saddle purchasing, both a call option and a put option on some asset an investor may take a long straddle position if he thinks the market is highly volatile, but does not know in which direction it is going to move. This position is a limited risk, since the most a purchaser may lose is the cost of both options. At the same time, there is unlimited profit potential

Strangle Similar to a saddle, however the options have different strike prices.

Covered Call seller of call options owns the corresponding amount of the underlying instrument, such as shares of a stock or other securities.