Download

1 / 47

500 likes | 763 Views

Options. Financial options contracts. An option is a right (rather than a commitment) to buy or sell an asset at a pre-specified price The right to purchase is a call option; the right to sell is a put option The strike price (or exercise price) is the price at which an option can be exercised

E N D

F520 Options Options

F520 Options Financial options contracts • An option is a right (rather than a commitment) to buy or sell an asset at a pre-specified price • The right to purchase is a call option; the right to sell is a put option • The strike price (or exercise price) is the price at which an option can be exercised • Options which can be exercised only at maturity are “European Options”; “American Options” can be exercise any time prior or at maturity • Options can be traded on exchanges or OTC markets.

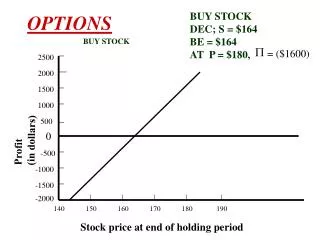

F520 Options Call Options • Buying a Call Option--Gives the purchaser the right, but not the obligation, to buy the underlying security from the writer of the option at a pre-specified price • t=0 pay C t=1 receive Max(0,PR-X) • Writing a Call Option—Gives the writer the obligation to sell the underlying security at a pre-specified price • t=0 receive C t=1 pay Max(0,PR-X) C = Call Premium PR = Price of underlying security X = Exercise Price

F520 Options Net Payoff of a Call Option(includes call premium) Buyer of a Call Net Payoff A Payoff of Call ($) 0 Security Price -C X Writer of a Call Payoff of Call ($) +C Net Payoff 0 Security Price X A

F520 Options Value of a Call Option Price ($) Call Price Intrinsic value max(0,S-X) Time Value Security Price X

F520 Options Put Options • Buying a Put Option - Gives the purchaser the right, not the obligation, to sell the underlying security to the writer of the option at a pre-specified exercise price. • t=0 pay P t=1 receive Max(0,X-PR) • Writing a Put Option - Gives the writer the obligation to buy the underlying security at a pre-specified price. • t=0 receive P t=1 pay Max(0,X-PR) P = Put Premium

F520 Options Net Payoff of a Put Option +(S0-P) Buyer of a Put Payoff of Put ($) 0 Security Price -P Net Payoff B X Writer of a Put Net Payoff Payoff of Put ($) +P 0 B X Security Price -(S0-P)

F520 Options Value of a Put Option Intrinsic value max(0,X-S) Price ($) Put Price Time Value Security Price X

F520 Options Caps, Floors, and Collars • A cap is a call option where the seller guarantees to pay the buyer when the designated reference price exceed a predetermined cap price. The buyer pays a cap fee. • A floor is a put option where the seller guarantees to pay the buyer when the designated reference price falls below a predetermined floor price. The buyer pays a floor fee. • A collar is a position that simultaneously buys a cap and sells a floor.

F520 Options Option Price Option Price Intrinsic Value Time Value + = Security Price (S) Exercise Price (X) Volatility (s) Interest rate (r) Time to Expiration (T) Call intrinsic value = max(0,S - X) Put intrinsic value = max(0,X - S)

F520 – Futures http://www.lme.com/metals/non-ferrous/copper/

F520 – Futures Copper Futures, price per pound, 25,000 pounds per contract Daily Settlements for Copper Future Futures (FINAL) - Trade Date: 09/13/2013 | http://www.cmegroup.com/trading/metals/base/copper_quotes_settlements_futures.html

F520 Options Understanding Option Quotes Copper Options on Futures (Call in Dec)

F520 Options Understanding Option Quotes Copper Options on Futures (Put in Dec)

F520 Options Understanding December Quotes • How much does it cost to purchase: • one call of Copper Futures Options contract (exercise price of 317)?Call = .1335 / lb * 25,000 lb per contract = $5,075.49 per contract • What is the intrinsic value of a call on Copper Futures Options (exercise price of 317)?Call = max(0,F-X) = max(0,3.20 – 3.17) = 0.03 centsUse the futures copper price (not the cash price)What is the time value of money?Option Price - Intrinsic Value = 0.1335 – 0.03 = 0.1035 / lb • What is the intrinsic value of a call on Copper Futures Options (exercise price of 324)?Call = max(0,F-X) = max(0,3.30 – 3.24) = 0 centsUse the futures copper price (not the cash price)What is the time value of money?Option Price - Intrinsic Value = 0.0955 – 0 = 0.0955 / lb • What is the intrinsic value of a call on Copper Futures Options (exercise price of 320)? Option Price - Intrinsic Value = 0.1165 – 0 = 0.1165 / lb • Why there greater intrinsic value for options near the money.

F520 Options Understanding Option Prices Option Price Intrinsic Value Time Value + = Security Price (S) Exercise Price (X) Volatility (s) Interest rate (r) Time to Expiration (T) Call intrinsic value = max(0,S - X) Put intrinsic value = max(0,X - S)

F520 Options Value of a Call Option Price ($) Call Price Intrinsic value max(0,S-X) Time Value Security Price X

F520 Options Value of a Put Option Intrinsic value max(0,X-S) Price ($) Put Price Time Value Security Price X

F520 Options The Black-Scholes Option Pricing Model • The B-S option pricing model for a call is: C = S0 - Xe-rT + P C = S0N(d1) - Xe-rTN(d2) where d1 = [ln(S/X)+(r+ ½s2)T]/sÖT d2 = d1 - sÖT N(d) = cumulative normal distribution

F520 Options Black-Scholes Put Price • Price of a European put is: P = C - S0 + Xe-rT = S0[N(d1)-1] - Xe-rT[N(d2)-1] where d1, d2, and N(d) are defined as before.

F520 Options Black-Scholes Pricing Example • Assume: • S0 = $100 • X = $100 • r = 5% • s = 22% • T = 1 year • Then: • d1 = 0.34, N(d1) = 0.6331 • d2 = 0.12 N(d2) = 0.5478 C = S0N(d1) - Xe-rTN(d2) d1 = [ln(S/X)+(r+ ½s2)T]/sÖT d1 = [ln(100/100)+(.05+ ½(0.22)2)1]/(0.22)Ö1 d1 = 0 + .0742/.22 = .337274 d2 = d1 - sÖT d2 = .33727 - 0.22/Ö1 = .117273

F520 Options Call Option Example • Price of a call is then: C = S0N(d1) - Xe-rTN(d2) C = 100(0.6331) - 100(0.9512)(0.5478) = $11.20 • Price of a put is then: P = S0[N(d1)-1] - Xe-rT[N(d2)-1] P = 100[.6331 - 1] - 100(1/e(.05*1))(.5478-1) P = 100(-0.3669) - 100(0.9512)(-0.4522) = $6.32 • Double check through Put-Call Parity: P = C - S0 + Xe-rT 6.32 = 11.20 – 100 + 100(0.9512)

F520 Options Relationship of Option and Security Prices Parameters: X = $100, T = 3 months, r = 5%, and s = 25% Changing S

F520 Options Relationship of Option Prices to Interest Rates Parameters: S=$100, X = $100, T = 3 months, and s = 25% Changing r

F520 Options Relationship of Option Prices to Volatility Parameters: S=$100, X = $100, T = 3 months, and r = 5% Changing s

F520 Options Relationship of Option Prices to Time to Expiration Parameters: S = $100, X = $100, r = 5%, and s = 25% Changing t

F520 Options Parameters of the Black-Scholes Model • Need to know: • S, X, r, T, s. • All readily observable, except the last. • The interest rate should be a continuously compounded rate • To convert simple annualized rate to continuously compounded rate: r = ln(1+R)

F520 Options Volatility as a Parameter • In pricing options, analysts usually use some measure of historical volatility of the underlying security. • Volatility obtained from other than annualized returns must be converted to annualized volatility. • e.g., Variance of weekly returns must be multiplied by 52. • e.g., Standard deviation of weekly returns must be multiplied by Ö52.

F520 Options Implied Volatility • Alternatively, can use all the other inputs, and infer a volatility estimate from the current option price. • Is called the implied volatility. • Can then compare implied volatility with recent historical volatility. • Higher implied than historical may indicate the option is expensive. • Lower implied than historical may indicate the option is cheap.

F520 Options Implied Volatility Using the Black-Scholes Model http://www.numa.com/derivs/ref/calculat/option/calc-opa.htm Given Information S0 = $100, X = 100 r = 8%, T = 30 days, P = $3.10, and C = $3.73 Volatility implied by option prices

F520 Options Assumptions In Original Option Pricing Model • Underlying returns log normally distributed. • Variance is constant over time. • The interest rate is constant over time. • No sudden jumps in underlying price. • No dividends. • No early exercise (i.e., European option).

F520 Options Enhancing Firm Value through Hedging • Reducing Volatility of cash flows does not guarantee increased value. • Hedging has transaction costs, so hedging is not free. • Hedging can add value if • Taxes are reduced • Transaction costs (like default risk) is reduced • When it aligns incentives to take positive NPV projects

F520 Options Unhedged

F520 Options Hedged

F520 Options Note the similarities between the payoff on stock and a call option. Buyer of a Call / Stock Net Payoff Payoff on Firm ($) 0 X = Debt Amount Market Value of Assets -C In our prior example, stockholders only get paid after the debtholders receive their value. Therefore, the value of the debt is like the exercise price on a call option. If the value of the firm is less than the value of the debt, stockholders will walk away and leave the firm to the debtholders. If the value of the firm is greater than the value of the debt, the stockholders remain in control of the firm. This also shows why reducing volatility (through hedging) does not guarantee an increase in the value of the firm. In fact, as shown in the Black Scholes formula, decreasing volatility can reduce the value of the firm to equity holders (see the hedging example several slides earlier.

F520 Options Will the Unhedged firm add a risk-free project when new capital must be added by equityholders

F520 Options Would New Bondholders add the new capital?Bondholders generally enter as subordinate to the old bonds.

F520 Options Will the hedged firm add take a risk-free project?

F520 Options Swaps • A swap is an agreement whereby two parties (called counterparties) agree to exchange periodic payments. The dollar amount of the payments exchanged is based on some predetermined dollar principal (or commodity quantity), which is called the notional amount. • It can be considered the same as entering a series of forward contracts, since it is an agreement to make the exchange at several points in the future. • Types of swaps include • Interest rate swaps • Interest rate-equity swaps • Equity swaps • Currency swaps • Commodity swaps

F520 Options Comparing Forwards and swaps • Assume the following forward prices for commodity X • 3 months $0.6230 per pound • 6 months $0.6305 per pound • 9 months $0.6375 per pound • 12 months $0.6460 per pound • A company enters 4 forward contracts (one in each month) with a promise to deliver 100,000 pounds of copper each month for the prices set above. Deliver 100,000 lbs 100,000 lbs 100,000 lbs 100,000 lbs 3 6 9 12 mo Receive $62,300 $63,050 $63,750 $64,600

F520 Options Calculating swap payment • Find the Present Value of the Cash Flows (assume 2% per quarter)PV = $62,300/(1.02)1 + $63,050/(1.02)2 + $63,750/(1.02)3 + $64,600/ /(1.02)4 = $241,433.59 • Now spread this value over 4 equal payments at the end of each period (4 period annuity).PV = $241,433.59, I = 2, N = 4, FV = 0, compute PMTPMT = $63,406.19 • A swap will have four equal payments of $63,158.72 at the end of each quarter. Deliver 100,000 lbs 100,000 lbs 100,000 lbs 100,000 lbs 3 6 9 12 mo Receive $63,406 $63,406 $63,406 $63,406

F520 Options Using Duration in Hedging • Hedge the future issuance of 90-day commercial paper. Assume today is August 10, 200X. Our projected date of cash flow needs is November 25, 200X. • üThe amount of commercial paper that will be issued is $50 million. • üThe Euro-dollar Futures contract has a face value of $1 million is if for a 90-day maturity Eurodollar issue to be made 107 days from today. • Should you take a long or a short position?

F520 Options Should you take a long or a short position? • You want to protect against rising interest rates that results in falling prices. Therefore, you want the futures contract to make money when prices fall (a short position). These profits from the futures contract will offset the lower set of funds your will be able to bring in if interest rates increase and you issue the commercial paper at a larger discount. • How many contracts do we need?

F520 Options How many contracts do we need? Formula from Hedging notes: $ amt. of security duration of asset # of Contracts = --------------------------- X ------------------------ $ amt. of fut. contract duration of future sec $50,000,000 90-days # of Contracts = ----------------------- X ------------------------ = 50 $1,000,000 90-days contracts

F520 Options • If commercial paper rates go up by 40 basis points (from 3.53% to 3.93%) and Eurodollar future rates also go up by 40 basis points (from 3.565% to 3.965), how much money will get from the futures contract and how much money will we get from our commercial paper issuance? • Futures contract • 40 bp * $25 per basis point *50 contracts = $50,000 profit • Commercial paper issuance: • 1,000,000 * (1-.0393*(90/360)) = $990,175 • x 50 contracts • $49,508,750 • This is exactly $50,000 less than what we had anticipated raising if rates had remained at 3.53%. • Between the profits from the futures contract and the expected commercial paper issuance proceeds, we have locked in our expected cash flow. Now let’s just hope that our basis risk (difference between spot and futures prices) remains the same over this time period. • Notes: • üThe change in $1 million for a 1 bp interest rate change is equal to $1,000,000*(.0001*(90/360)) = $25 • ü1,000,000 * (1-.0353*(90/360)) = $990,175 • x 50 contracts • $49,558,750

F520 Options How many contracts do we need? Situation 2 If we had a desire to issue commercial paper 107 days from now with 120-days to maturity, how many contracts would we need? $50,000,000 120-days # of Contracts = --------------------- X --------------------- = 66.67 $1,000,000 90-days contracts

F520 Options Contracts • Options and Futureshttp://www.cmegroup.com/education/getting-started.html • Future and Option contractshttp://www.cmegroup.com/globex/ • www.cmegroup.com