Download

1 / 17

170 likes | 348 Views

KBC policy towards Central Europe. Conference on t he current economic situation and future developments in the Visegrad countries on the eve of their accession to the European Union , 29 September 2003 Dirk Mampaey, General Co-ordinator Banks Central Europe KBC Group.

E N D

KBC policy towards Central Europe Conference on the current economic situation and future developments in the Visegrad countrieson the eve of their accession to the European Union, 29 September 2003 Dirk Mampaey, General Co-ordinator Banks Central Europe KBC Group

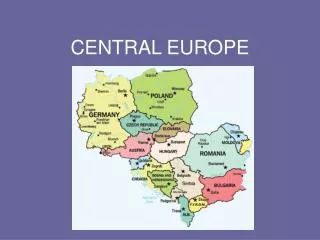

KBC strategy in Central Europe Main bank-insurance group in CE with focus on Retail – SME Geographical priority : Czech Rep, Slovak Rep, Poland, Hungary, Slovenia (EU accession countries) Development of specialised activities Markets, Leasing, Asset Management, Structured Finance Estonia Latvia Russia BalticSea Lithuania Byelarus POLAND Ukraine CZECH SLOVAKIA Moldova HUNGARY Slovenia Romania Croatia Bosnia Bulgaria Serbia Montenegro Macedonia

In search for a second home market • Need to expand ‘domestic’ customer base : • But saturated Belgian home market • Second home market in Western Europe ? • Also largely saturated • Very high acquisition prices • KBC only medium-sized player • Second home market in Central Europe ? • Room for further development of banking and insurance sector • Early entry • Ability to buy considerable market shares • Risk tempered by expected EU-entry

How it startedMilestones - Bank • 1994 : Approval of first Central European policy • 1996 : First investment in Kredyt Bank, Poland • 1997 : First investment in K&H Bank, Hungary • 1999 : KBC acquires 82% in CSOB, Czech & Slovak Republics • 2000 : CSOB acquires IPB • 2001 : Merger of K&H Bank and ABN AMRO Magyar • 2002 : Agreement on 34% stake in NLB

How it startedMilestones - Insurance • 1993 : Argosz (Hungary) : greenfield • 1998 : - K&H Life: greenfield - 34% stake in Chmelarska Pojist’ovna (now CSOB Poj.) • 2000 : KBC acquired 40% stake in Warta • 2002 : - 65% stake in IPB Pojist’ovna - Majority stake in Ergo • 2003 : NLB Vita : greenfield

The KBC Group in Central EuropeParticipation rate of KBC (30-6-03) Poland Kredyt Bank (76%) Warta (40%) Indirect presence Lituania & Ukraine (via Kredyt Bank) Bosnia & Macedonia (via NLB) Czech Republic CSOB (84%) CSOB Pojist’ovna (96%) Patria Finance (100%) Slovakia CSOB (84%) Ergo Poist’ovna (74%) Hungary K&H Bank (59%) K&H Life (80%) Argosz (99%) Slovenia NLB (34%) NLB Vita (67%) Percentages concern direct + indrect presence

Current presence of the KBC Groupin Central Europe / Banking side (30-6-03) Poland (banking) Ranking: 7th Market share: 6% Clients: 1.2 m * Branches: 379 Czech Republic (banking) Ranking: 2nd Market share: 18% Clients: 2.9 m Branches: 208 Slovakia (banking) Ranking: 4th Market share: 5,7 % Clients: 0.2 m Branches: 67 Hungary (banking) Ranking: 2nd Market share: 12% Clients: 0.7 m Branches 157 Slovenia (banking) Ranking 1st Market share: 44% Clients: 0.9 m Branches 264 Market share is average of share in customer credits and in customer deposits * estimate

Current presence of the KBC Groupin CE / Insurances side (30-6-03) Poland (non-life / life insur.) Ranking: 2nd/9th Market share: 14%/1% Czech Republic (non-life / life insur.) Ranking: 6th/5th Market share: 4%/9% Slovakia (non-life / life insur.) Ranking: 8th/6th Market share: 2%/4% Hungary (non-life / life insur.) Ranking: 6th/14th Market share: 4%/2% Slovenia (non-life / life insur.) Start-up phase of life assurance cy

Economy : LT growth potential Benefits of EU/EMU accession • Growth potential higher than in EU-15 : • Increase in competition and efficiency, lower transaction costs • Possibility of economies of scale • EU-membership stimulates significant inflow of foreign direct investments • Gives investors clear signal about direction of economic policy in long term • Puts new members on path to EMU fosters macro-economic stability • Prospect of selling goods produced in candidate countries throughout EU single market

Central European growth potential * Purchasing power parities ** Banking: average of deposits and domestic credits in % of GDP (2002). Insurance: premiums in % of GDP (2001).

EMU accession : when?Not before 2008/2009 Maastricht convergence criteria

Economy…stimulates productivity n.a. Source: OECD

Economy LT growth potential : outlook for 2002-2020 Source : EC, OECD, UN

Financial sector in CE • Likely to undergo significant further changes in future. Moving from an era of transition, instability and restructuring into an era of stability, strengthening and development,but still largely underdeveloped despite considerable progress • EU-accession and EMU-entry important milestones Anticipation has already begun to shape Central European financial sectors • Adoption EU-compatible financial regulation and legislation • High share EU-ownership in banking sectors • Strong financial integration with EU

Financial sector in CE • Strong growth potential, which can be gauged by comparing current situation with average of financial sector indicators in euro area : integration process can be expected to eventually make accession countries broadly comparable to current euro area member countries • Different government approach in restructuring the financial sector and in taking over bad loans • High degree of foreign involvement

Financial sectorUse of banking products % of total population over 15 years who use this productUse of banking products not widely spread room for further development Source: HVB

KBC policy towards Central EuropeConference on the current economic situation and future developments in the Visegrad countrieson the eve of their accession to the European Union, 29 September 2003Dirk Mampaey, General Co-ordinator Banks Central Europe KBC Group