Download

1 / 15

150 likes | 337 Views

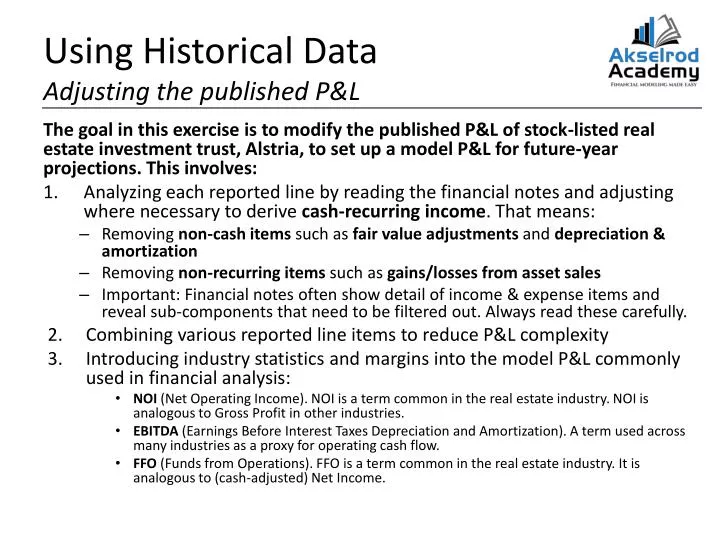

Using Historical Data Adjusting the published P&L. The goal in this exercise is to modify the published P&L of stock-listed real estate investment trust, Alstria , to set up a model P&L for future-year projections. This involves:

E N D

Using Historical DataAdjusting the published P&L The goal in this exercise is to modify the published P&L of stock-listed real estate investment trust, Alstria, to set up a model P&L for future-year projections. This involves: • Analyzing each reported line by reading the financial notes and adjusting where necessary to derive cash-recurring income. That means: • Removing non-cash items such as fair value adjustmentsand depreciation & amortization • Removing non-recurring items such as gains/losses from asset sales • Important: Financial notes often show detail of income & expense items and reveal sub-components that need to be filtered out. Always read these carefully. • Combining various reported line items to reduce P&L complexity • Introducing industry statistics and margins into the model P&L commonly used in financial analysis: • NOI (Net Operating Income). NOI is a term common in the real estate industry. NOI is analogous to Gross Profit in other industries. • EBITDA (Earnings Before Interest Taxes Depreciation and Amortization). A term used across many industries as a proxy for operating cash flow. • FFO (Funds from Operations). FFO is a term common in the real estate industry. It is analogous to (cash-adjusted) Net Income.

Adjusting the Published P&LReading the Notes Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P<he Revenue Line Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LOperating Expenses & NOI Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LCorporate Expense Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LOther Operating Income & Expense Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LEBITDA & EBITDA Margin Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LDepreciation & Amortization Alstria REIT AG, D&A Calculation Alstria REIT AG, Model P&L • Depreciation & Amortization is now subtracted here, even though we previously stripped these expenses out of individual line items as “non-cash” • The reason D&A is now subtracted is so that Cash Taxes can be calculated: • Cash Taxes are calculated based on Profit Before Tax (PBT) • PBT is calculated based on all expenses, including non-cash expense like D&A • Ergo, to calculate Cash Taxes we need PBT. And to calculate PBT, we need to subtract D&A– even though it is a non-cash expense • PBT is then multiplied by the Tax Rate to derive Cash Taxes • D&A is added back after the tax calc’nto derive FFO • For REITs this is irrelevant as they are tax exempt. The methodology is shown for illustrative purposes

Adjusting the Published P&LFinancial Expenses Alstria REIT AG, Published P&L Alstria REIT AG, Published CF Statement

Adjusting the Published P&LFinancial Expenses Alstria REIT AG, Financial Expenses Alstria REIT AG, Model P&L • Comparing net financial expenses on the Cash Flow Statement of ca. €45.9mm with the figures on the P&L of ca. €43.2mm shows a material difference • …and looking at the P&L notes doesn’t reveal much about this difference • …so we provisionally use the higher CF/Statement amount… • …and ask management to clarify the discrepancy…

Adjusting the Published P&LGetting Management Clarification You: Hi Alex, I was looking at your financial statements and had a quick question about 2010 financial expenses. It seems that the net financial expenses on the P&L are about €2.7mm lower than on the Cash Flow Statement. Can you explain the difference please? Alexander Dexne (CFO, Alstria): Of course, the difference between the CF/S and P&L amounts is related to a timing-mismatch in the actual cash payments we make on our debt. Essentially some of the interest expense payments that belong to the calendar year 2011, were made in 2010… so the 2010 cash interest payments are artificially high.

Adjusting the Published P&LFinancial Expenses Alstria REIT AG, Financial Expenses Alstria REIT AG, Model P&L • Following management feedback, we understand the mismatch in CF/S and P&L financial expenses relates only to timing • We therefore use the (lower) P&L expense, as we would otherwise be incorrectly allocating interest expense that belongs to the 2011 calendar year into 2010 • We also strip €278k of non-cash value adjustments out of the financial expenses

Adjusting the Published P&LNon-Operating Items Alstria REIT AG, Non-Operating Items Alstria REIT AG, Published P&L • Looking at Joint Venture Income, we notice that the amount is relatively high, but reading “Note 4” reveals little about its nature • Given the size of the item, we suspect that it may be “one-time” or non-cash income… • …so we search the Annual Report document (“CTRL + F”) for the term “Joint Venture”… • …and find in the published FFO calculation that the income is indeed entirely made up of non-cash fair value adjustments • We also exclude the Net loss from fair value adjustments on derivatives as a non-cash expense

Adjusting the Published P&LNon-Operating Items Alstria REIT AG, Published P&L Alstria REIT AG, Model P&L

Adjusting the Published P&LPublished FFO vs. Model FFO Alstria REIT AG, Published FFO Calculation Alstria REIT AG, Model P&L • We note that published FFO of €27.5mm is ca. €2.7mm below the €30.2mm we calculate, or €0.05 per share using average shares outstanding…a material difference vs. published disclosure.