Download

1 / 15

190 likes | 592 Views

Administrative Set up of Excise Department. INTRODUCTION. The organization of excise department is structured to facilitate collection of indirect

E N D

INTRODUCTION The organization of excise department is structured to facilitate collection of indirect taxes. The apex body in-charge of administration of the collection of both custom duties and excise duties is central board of excise and customs (CBEC).

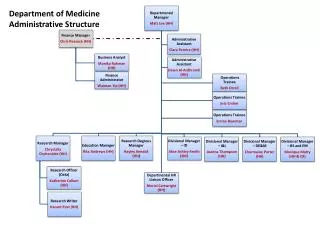

Ministry of Finance CBEC & C Principal /Chief Commissioners Commissioner (Appeals) Commissioner (Adjudication) Commissioner Additional Commissioner Joint Commissioner Deputy/ Assistant Commissioner of Center Excise (for each division) Range Officer/Superintendent (for each range) Sector Officers (Inspector) (for each sector)

The apex body in charge of administration of the collection of both custom duties and central excise duties is central board of excise and customs (CBCE), New Delhi. • The board consist of a chairman and five members. • Chairman of is empowered to work among himself and other members. • The responsibilities are equally divided between the members and chairman. CENTRAL BOARD OF EXCISE AND CUSTOMS

POWERS OF CBEC 1.It deals with the task of formulation of policy Concerning levy and collection of customs and central excise duties. 2.CBEC is the administrative authority. 3.CBEC has the powers to appoint central excise officers. 4.The board can issue orders, instructions and directions to excise officers acting for purpose of uniformity in policies and procedures.

PRINCIPAL COMMISSIONER/ CHIEF COMMISSIONER OF CENTRAL EXCISE The powers of chief commissioner of central excise are mainly supervisory in nature. There are 23 chief commissioner in India looking after ‘zones’ assign to each one. All chief commissioner of excise are chief commissioners of customs too.

COMMISSIONER OF CENTRAL EXCISE Main Administrative powers for routine working of department are Delegated to “Commissioner”. There are 92 sub-regions headed by Commissioners of Central Excise. Each commissioner administrative in-charge of sub-region in a region.

Powers of Central Excise Officer Central excise act,1944 • 1.Power to arrest [Section 13] • 2.Power to summon person [section 14] • 3.Special audit in certain cases (section 14A) • 4.Special audit in case Where credit of duty availed or utilized is not within the normal limits (Section 14 A) Central Excise Rules, 2002 • 1.Granting exemption from duty (rule 21) • 2.Access to Registered premises [rule 22] • 3.Power to stop and search [rule 23] • 4.Power to detain good or seize the goods [rule 24] • 5.Disposal or confiscated goods. • 6.Power to issue supplemental instructions [Rule 3]

These powers are discussed in brief below:- 1. Exercising Power of Subordinate Officers.A Central Excise officer can exercise the powers and discharge the duties, imposed under the Act.2.Power to stop and seize (Rule 23):Excise Officer can detain or stop any person or vehicle and examine the goods or he person. If any contravention of rule is suspected, such goods can be detained seized.3.Access to Registered Premises (Rule 22 (1)): An Officer empowered by the Commission shall have access to any premises registered for the purpose of carrying out any scrutiny, verification and check to safeguard the interest of revenue. 4. Power of Summon (Section 14):(a) Any Central Excise Officer shall have power to summon any person whose attendance he considers necessary.b) All persons so summoned shall be bound to attend, either in person or by an authorised agent.

5. To Order Special Audit In Certain Cases (Section 14A): (a) If at any stage of enquiry the value has not correctly declared by manufacturer he may direct such manufacturer to get the accounts, audited by a cost accountant.(b) The cost accountant shall, submit the report of such audit duly signed by him to said CEO. 6. To order special audit in case where credit of duty availed or utilized is not with in the normal limits, etc. (Section 14AA). If the Commissioner of Central Excise has reason to believe that the credit of duty availed of under the rules by manufacturer of excisable goods. Is not with in the normal limits. has been availed of by the reason of fraud, collusion and willful miss statement 7. Power to Arrest (Section 13): Any Central Excise Officer arrest any person whom he has “reason to believe” be liable to punish under the provision of the act or the rules. 8. Power of Search: Excise Officer has power to enter or search at any time, any land, building premises, vehicle or other places where he has reasons to believe that excisable goods are processed in contravention of excise rules. Inspector of Central Excise is empowered to carry out search with written permission.

9. Power of Seizer (Rule 24): Seizer means take possession of goods in pursuance of demand under legal right. Excise Officer is empowered to seize the goods if he has reasons to believe that such goods are liable for confiscation under the Central Excise act 1944. 10.Granting Exemption from Excise Duty (Rule 21):If the goods stored in the ware house are lost or destroyed then the Commissioner can grant the exemption of excise duty on it. 11.Disposal of Goods Confiscated (Rule 29): Confiscated goods in respect of which the option of paying a fine in lieu of confiscation has not been exercised, shall be sold or destroyed. 12. Power to Issue Supplemental Instructions (Rule 31): The board, the Chief Commissioner and the Commissioner have the powers to issue in writing the supplemental instructions for the implementation of the rules.

DUTIES:Provisions regarding duties under Central Excise 1944 are as under:-1. Officers required to assist Central Excise Officer (Section 15):All officers of Police and all officers of Govt. engaged in the collection of the land revenue and all village officers are empowered and required to assist the CEO in execution of the act. 2. Procedures to be followed in case of searches and arrests (Section 18): All searches and arrest made under this act can be carried out in accordance with the provisions of code of criminal procedures, 1973. 3. Disposal of Persons Arrested: Every person arrested under the act must be forwarded, without delay to nearest CEO empowered send persons so arrested to a magistrate. 4. Duty of Officer-In-charge of Police Station (Section 20):The Officer Incharge of a police station to whom any person is forwarded under section 19 shall admit him to bail to appear before the magistrate. Failure of Central excise officer in Duty: Any Central excise officers who ceases or refuses to perform or withdraws himself from the duties of his office, shall on conviction before a magistrate be punishable with imprisonment from a term which may extend to three months, or with fine which may extend to three months pay.

Powers of The Deputy Commissioner • To permit the withdrawal of 75% of the amount of Bond deposited by the tax-payer. • To permit the export of goods. • To order the filing of return in relation to products. • To grant pardon for not resorting to special proceeding. • To grant permission in case of need for re-entry of goods in the factory. • To appoint the In-charge of the Warehouse. • To increase the time limit for the return of the goods. • Powers of The Assistant Commissioner • To grant permission to with draw money from the current Account • (PLA) • To permit the filing up of Bond for temporary determination of duty • To accept the bond. • To forfeit the security. • To sell the seized goods. • To accept Refund. • To determine the stock.

Powers of Superintendent • To ratify the appointment of authorized agent. • To grant permission to take out of the factory the goods, which are exempt from duty. • To grant permission to take out of the factory the goods, on which excise duty is paid. • To Excuse the delay in filing the application form. • To accept the application for renewal. • To order advance payment of Excise Duty. • Powers of Inspector • He is the lowest officer in the chain of officers. • An Inspector has to perform all the duties assigned to him by superior under whom he is working. • He would submit his report to the officer under whom he is working. • Though he is the lowest officer but is very important because it is on his report that his senior initiate further action.

TYPES OF EXCISE CONTROL Physical Control: The goods were cleared from factory under supervision of Excise authorities only which was known as Physical Control. Assessment is done by a Central Excise Officer and thereafter the goods are removed under his supervision . Self Assessment Procedure: Under Self Assessment Procedure assesses need not submit application for removal in the form (AR-I) for assessment. He can prepare his own invoice and clear the goods without obtaining counter signature of excise inspectors. The Compounded Levy Scheme : It is applicable in case of small scale industries. The payment of duty under the Compounded Levy Scheme is greatly beneficial to SSI as it abserves manufacturers from observing day to day formalities regarding maintenance of accounts etc.