Download

1 / 27

270 likes | 378 Views

MBA795 Strategy Formulation. Steven E. Phelan. Introduction. Course Objectives Course Assessment Group Formation. Registration Codes. www.bsg-online.com Intro to simulation next week! Registration required for passing grade Company Registration Code Company A 9099-SPN-A

E N D

MBA795 Strategy Formulation Steven E. Phelan

Introduction Course Objectives Course Assessment Group Formation

Registration Codes www.bsg-online.com Intro to simulation next week! Registration required for passing grade Company Registration Code Company A 9099-SPN-A Company B 9099-SPN-B Company C 9099-SPN-C Company D 9099-SPN-D Company E 9099-SPN-E Company F 9099-SPN-F Company G 9099-SPN-G Company H 9099-SPN-H

The Concept of Strategy OUTLINE • The role of strategy in success • A framework for strategy analysis • The evolution of strategic management • Corporate strategy and business strategy • Strategy making: Design or process? • The role of strategy

What Makes a Successful Strategy? Successful Strategy EFFECTIVE IMPLEMENTATION Long-term, simple and agreed objectives Profound understanding of the competitive environment Objective appraisal of resources

What is Strategy? • Distinguishing strategy from tactics: • Strategy is the overall plan for deploying resources to establish a favorable position. • Tactic is a scheme for a specific maneuver. • (Plan versus strategy?) • Characteristics of strategic decisions: • Important. • Involve a significant commitment of resources. • Not easily reversible. • (Long term)

The Evolution of Strategic Management 1950s 1960s-early 70s Mid-70s-mid-80s Late 80s –1990s 2000s Budgetary Corporate Positioning Competitive Strategic planning & planning advantage innovation control Financial Planning Selecting Focusing on Reconciling control growth &- sectors/markets. sources of size with diversificationPositioning for competitive flexibility & leadership advantage agility Capital Forecasting. Industry analysis Resources & Cooperative budgeting. Corporate Segmentation capabilities. strategy. Financial planning. Experience curve Shareholder Complexity. planning Synergy Portfolio analysis value. Owning E-commerce. standards. — Knowledge Management— Coordination Corporate Diversification. Restructuring. Alliances & & control by planning depts. Global strategies. Reengineering. networks Budgeting created. Rise of Matrix structures Refocusing. Self -organiz systems corporate Outsourcing. ation & virtual planning organization DOMINANT THEME MAIN ISSUES KEY CONCEPTS& TOOLS MANAGE-MENT IMPLIC- ATIONS

The Basic FrameworkStrategy: the Link between the Firm and its Environment THE FIRM •Goals & Values •Resources & Capabilities •Structure & Systems THE INDUSTRY ENVIRONMENT • Competitors •Customers •Suppliers STRATEGY STRATEGY SWOT or WOTS-Up Analysis

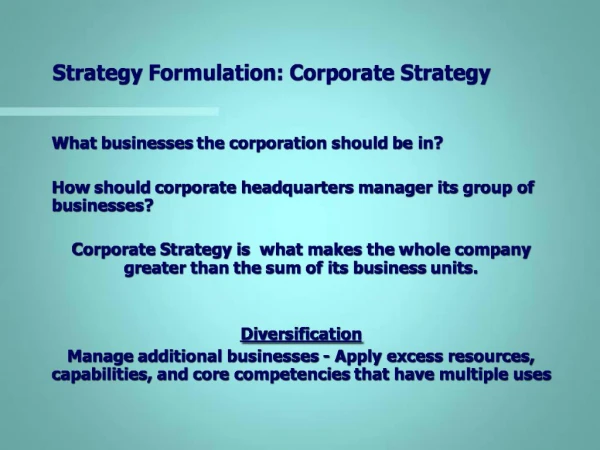

Sources of Superior Profitability INDUSTRY ATTRACTIVENESS Which businesses should we be in? CORPORATE STRATEGY RATE OF PROFIT ABOVE THE COMPETITIVE LEVEL How do we make money? COMPETITIVE ADVANTAGE How should we compete? BUSINESS STRATEGY

Strategy Making : Design or Process? Strategy as Design Strategy as Process Planning and rational choice Many decision makers responding to multitude of external and internal forces INTENDED STRATEGY EMERGENT STRATEGY REALIZED STRATEGY • Mintzberg’s Critique of Formal Strategic Planning: • The fallacy of prediction –the future is unknown • The fallacy of detachment -- impossible to divorce formulation from • implementation • The fallacy of formalization --inhibits flexibility, spontaneity, • intuition andlearning.

Strategy Making Processes within the Company: Multiple Roles of Strategy Strategy as Decision Support Improves the quality of decision making (Real-Time Strategic Thinking rather than Strategic Planning) Strategy as Coordination and Communication Creates consistency and unity (Focuses Resource Allocation and Rationale) Improves perform- ance by setting high aspirations Strategy as Target

The Role of Analysis • Strategy analysis improves decision processes, but doesn’t give answers. • Strategy analysis assists us to identify and understand the main issues. • Strategy analysis helps us to manage complexity (tells us what to focus on). • Strategy analysis can enhance flexibility and innovation by supporting learning.

Goals, Values and Performance OUTLINE • Strategy as a quest for value • What is profit? • The shareholder value approach • The shareholder value and strategy formulation • Mission and values

Strategy as a Quest for Profit • The stakeholder approach: The firm is a coalition of interest groups—it seeks to balance their different objectives • INDUCEMENT v. CONTRIBUTION • The shareholder approach: The firm exists to maximize the wealth of its owners (= max. present value of profits over the life of the firm) • For the purposes of strategy analysis we assume that the primary goal of the firm is profit maximization. • Rationale: • Boards of directors legally obliged to pursue shareholder interest • To replace assets firm must earn return on capital > cost of capital • (difficult when competition strong). • Firms that do not max. stock-market value will be acquired Hence: Strategy analysis is concerned with identifying and accessing the sources of profit available to the firm

From Profit Maximization to Value Maximization • Profit maximization is an ambiguous goal • Total profit vs. Rate of profit • Over what time period? • What measure of profit? • Accounting profit versus economic profit (e.g. Economic Value Added: Post-tax operating profit lesscost of capital) Maximizing the value of the firm: Max. net present value of free cash flows: max. V = StCt (1 + r)t Where: V market value of the firm. Ct free cash flow in time t r weighted average cost of capital

The World’s Most Valuable Companies: Performance Under Different Profitability Measures

Shareholder Value Maximization and Strategy Choice The Value Maximizing Approach to Strategy Formulation: • Identify strategy alternatives • Estimate cash flows associated with each strategy • Estimate cost of capital for each strategy • Select the strategy which generates the highest NPV • Problems: • Estimating cash flows beyond 2-3 years is difficult • Value of firm depends on option value as well as DCF value • Implications for strategy analysis: • Some simple financial guidelines for value maximization • On existing assets—maximize after-tax rate of return • On new investment—seek rate of return > cost of capital • Utilize qualitative strategy analysis to evaluate future profit potential

Valuing Companies and Business Units If net cash flow growing at constant rate (g) V = C1 ( r - g ) With varying cash flows which can be forecasted for 4 years: V = C0 + C1 + C2 + C3 + VH (1 + r ) (1 + r )2 (1 + r )3 (1 + r )3 where: VH is the horizon value of the firm after 4 years

Real Options The right but not the obligation to buy an asset Black Scholes Formula used to value financial options There is hidden value in real (or strategic) options Flexibility to speed up or slow down projects Flexibility to abandon a project Flexibility to shutdown a project Flexibility to extend a project into new products or markets Flexibility to switch designs or plants In general, more uncertainty and more time before committing to a decision increases the value of an option Hence, strategists should seek explore options given time and uncertainty

Performance Diagnosis: Disaggregating Return on Capital Employed Past performance analysis (see Ford v. Toyota) COGS/Sales Margin (Return on Sales) Depreciation/Sales SGA expense/Sales ROCE Fixed asset turnover (Sales/PPE) Inventory Turnover (Sales/Inventories) Asset productivity (Sales/Capital Employed) Creditor Turnover (Sales/Receivables) Turnover of other items of working capital

Linking Value Drivers to Performance Targets Order Size Customer Mix Sales Targets Sales/Account Customer Churn Rate Margin cogs/ sales Deficit Rates Cost per Delivery Development Cost/Sales Maintenance cost Shareholder value creation ROCE New product development time Indirect/Direct Labor Inventory Turnover Customer Complaints Economic Profit Capital Turnover Downtime Capacity Utilization Accounts Payable Time Cash Turnover Accounts Receivable Time CEO Corporate/Divisional Functional Departments & Teams

Balanced Scorecard An attempt to link long-term (intangible) value drivers to financial measures An attempt to combat a tendency to short-termism by CEOs Four areas: Financial Customer Internal Learning & growth

Balanced Scorecard for Mobil N. American Marketing & Refining Strategic Objectives Strategic Measures F I N A N C I A L F1 Return on Capital Employed F2 Cash Flow F3 Profitability F4 Lowest Cost F5 Profitable Growth F6 Manage risk * ROCE * Cash Flow * Net Margin * Full cost per gallon delivered to customer * Volume growth rate Vs. industry * Risk index Financially Strong C O U M S E T R - C1 Continually delight the targeted consumer C2 Improve dealer/distributor profitability * Share of segment in key markets * Mystery shopper rating * Dealer/distributor margin on gasoline * Dealer/distributor survey Delight the Consumer Win-Win Relationship I N T E R N A L I1 Marketing 1. Innovative products and services 2. Dealer/distributor quality I2 Manufacturing 1. Lower manufacturing costs 2. Improve hardware and performance I3 Supply, Trading, Logistics 1. Reducing delivered cost 2. Trading organization 3. Inventory management I4 Improve health, safety, and environmental performance I5 Quality * Non-gasoline revenue and margin per square foot * Dealer/distributor acceptance rate of new programs * Dealer/distributor quality ratings * ROCE on refinery * Total expenses (per gallon) Vs. competition * Profitability index * Yield index Delivered cost per gallon .Vs. competitors * Trading margin * Inventory level compared to plan & to output rate * Number of incidents * Days away from work * Quality index Safe and Reliable Competitive Supplier Good Neighbor On Spec On time L E & A G R R N O I W N T G H L1 Organization Involvement L2 Core competencies and skills L3 Access to strategic information * Employee survey * Strategic competing (?) availability * Strategic information availability Motivated and Prepared

A Comprehensive Value Metrics Framework • Shareholder • Value • Measures: • Market value of the • firm • Market value added • (MVA) • Return to • shareholders • Intrinsic • Value • Measures: • Discounted cash • flows • Real option values • Financial • Indicators • Measures: • Return on Capital • Growth (of • revenues &operating • profits) • Economic profit (EVA) • Value • Drivers • Sources: • Market share • Scale economies • Innovation • Brands

The Paradox of Value The companies that are most successful in creating long term shareholder value are typically those that: • Have a mission—They give precedence to goals other than profitability and shareholder return; • Have strong, consistent, ethical values. • Examples: • “Visionary” companies studied by Collins & Porras, • e.g. Merck, Wal-Mart, Procter & Gamble, Disney, HP • Boeing — Focus pre-1996: “to build great planes,” weak • financial controls—yet high profitability • — Focus 1997-2003 : “creating shareholder • value”—Outcome: loss of market leadership, • declining profitability (Issue of Corporate Social Responsibility)