Download

1 / 113

1.13k likes | 1.31k Views

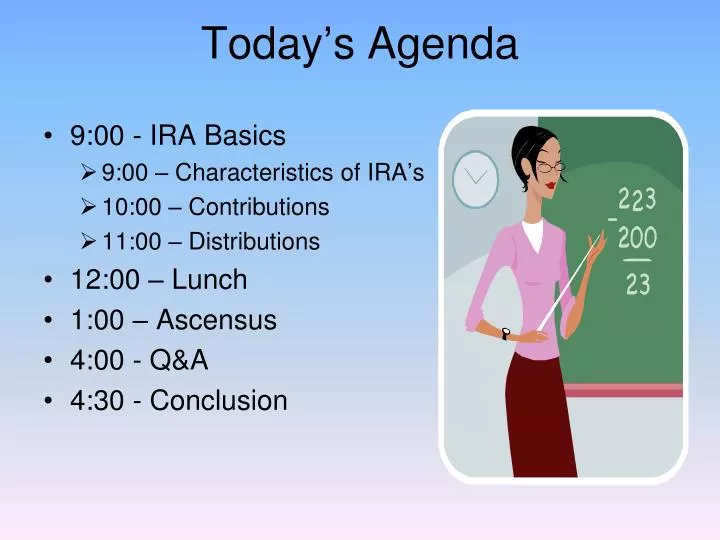

Today’s Agenda. 9:00 - IRA Basics 9:00 – Characteristics of IRA’s 10:00 – Contributions 11:00 – Distributions 12:00 – Lunch 1:00 – Ascensus 4:00 - Q&A 4:30 - Conclusion. IRA ACCOUNTS TRAINING. What is an IRA?.

E N D

Today’s Agenda • 9:00 - IRA Basics • 9:00 – Characteristics of IRA’s • 10:00 – Contributions • 11:00 – Distributions • 12:00 – Lunch • 1:00 – Ascensus • 4:00 - Q&A • 4:30 - Conclusion

What is an IRA? • An IRA is a special domestic trust, custodial account, or annuity contract established to hold assets for an individual’s retirement. • Two Varieties: • Individual Retirement Accounts (trusts and custodial) Completed at bank • Individual Retirement Annuities (contracts). Completed through an insurance company.

The IRA Plan CD CD SV IRA • The IRA is a single entity, or Plan, no matter how many types of investments are held by the IRA • One Individual Retirement Arrangement (IRA) • Many Investments/Accounts (Certificates or Savings)

IRA Facts • IRAs are Insured by NCUA separately from other accounts • Effective April 1, 2006, the NCUA raised the insured limit on IRAs to $250,000

DIFFERENT TYPES OF IRAS • Traditional • Roth • Educational

Establishing an IRA • CIP Completion • Documentation • Plan Agreement • Disclosure Statement • Financial Disclosure • Beneficiary Designation • Ancillary forms • Contribution form • Rollover Certification

Characteristics of Trad IRA’s • Tax Deduction for contribution • Tax Credit for contributions • Tax Deferred Earnings • Distributions are taxable

Advantages: Contributions may be tax deductible Earnings are tax deferred. Individual may receive a Tax credit (up to $2000) Disadvantages: Age restricted- Must be under age 70 ½ Must take Required Minimum Distributions Dividends taxable Traditional IRA’s

Traditional IRA Eligibility Requirements • MUST HAVE EARNED INCOME • Retirement, social security, dividend, or child support, rental income does not count • Must be under 70 ½ • Required Minimum Distributions are required at 70 ½, therefore they are no longer eligible to contribute to a Traditional IRA, even if they have earned income.

Contribution Limits • Lesser of annual contribution limit for tax year or 100% of earned income. • Reduced by Roth IRA Contributions for the year.

Characteristics of Roth IRA’s • No Tax Deduction • Tax Exempt Earnings • Tax Credit for contributions

Advantages Earnings potentially grow tax free No age restriction No Required Minimum Distributions Individual may receive a Tax credit (up to $2000) Disadvantages Contributions are not tax deductible Modified Adjusted Gross Income (MAGI) determines contribution eligibility Roth IRA’s

Roth IRA Eligibility Requirements • No Age requirement • MUST HAVE EARNED INCOME Retirement, social security, and dividend income does not qualify. • Member’s MAGI (Modified Adjusted Gross Income), determines eligibility to contribute, and amount they can contribute.

Married Filing Joint Ineligible to Contribute ^ $179,000 Phase Out $169,000 v Eligible to Contribute Single Ineligible to Contribute ^ $122,000 Phase Out $107,000 V Eligible to Contribute Eligible Roth IRA Contribution

Current Year Contribution • Made in, and for, the current year • 2010 annual limit is $5,000 • Qualified individuals ages 50 and over may contribute an additional $1,000 to their IRA for tax year 2006 and beyond • Can be regular or spousal

Previous Year Contributions • Contribution made in current tax year, to be credited for previous year tax return • Contribution made between Jan. 1st and Apr. 15th

Catch Up Contribution • Eligible the year they turn 50 • Extra $1000 over the normal contribution maximum, beginning in 2006 and beyond • Can also be Spousal

Spousal Contribution • Earning Spouse funds an IRA for the other Spouse who has little or no income • Joint Federal Tax Return must be filed • IRA is established for the non-compensated Spouse • Receiving Spouse must be under age 70 ½ (for Trad) no age restriction on Roth • Both IRA’s can not exceed $10,000.00 (unless contributing for Catch Up Contributions)

Transfer • Funds transferred between same type of IRAs, internally or externally • Check must be made payable to receiving Organization fbo member • No Reporting • No withholding • Unlimited # of transfers • Between like IRA’s Ex: BOA IRA to MCU IRA CD Sub 2 to CD sub 3

Rollover • Constructive receipt of assets • Reportable transaction (1099R and 5498) • Withholding applies (10%) • Penalties may apply • Irrevocable election in writing • Restrictions • Within 60 days • 12 month rule • RMD • May be Direct or Indirect

DIRECT We initiate the Rollover Ck is payable to MCU Fbo Member’s IRA INDIRECT Member initiated Rollover. We did not send for funds Ck is made payable to member Funds were previously w/d from an IRA, and are being re-invested within 60 days Types of Rollovers

Rollover from Retirement Plan to Traditional IRA’s • Can not transfer, must Rollover • Movement is not from like IRA’s. • Eligible plans include: • 401 (a) • 403 (a)(b) • 457(b) • Two Types of Rollovers: • Direct • Indirect

Conversion • Moving Funds from Traditional to Roth • Taxable, Reportable transaction • No IRS Penalty • Can be Direct or Indirect Pay taxes Roth IRA Traditional IRA Funds

Re-Characterization • Reverse a Conversion • Member has contributed to wrong type of IRA • Re-Characterization must also include the “Net Income Attributable” for the amount being Re-characterized • Completed by manager • Not subject to tax

How do I know if it is a Rollover, or a Transfer? Most Important question… What type of plan did the funds come from? If funds are from any other type of plan other than a Traditional or Roth IRA, it is ALWAYS a Rollover, regardless of how the check is made out. If funds come from a Traditional or Roth IRA, but the check is made payable to the Member, it is a Rollover. In order for it to be a transfer, the check MUST be made payable to MIDFLORIDA fbo the member. If the funds come from a Traditional or Roth IRA AND the check is made payable to MIDFLORIDA fbo the member’s IRA, it would be a Transfer.

Funds are from BOA Traditional IRA • Check is made payable to Member • Depositing to Traditional IRA here • Rollover or Transfer? • Rollover • Check is payable to Member

Check is from a 401K • Check is payable to MCU fbo the Member • Deposited to Traditional IRA here. • Transfer or Rollover? • Rollover • Funds are from a Qualified plan, not a Traditional IRA

Funds are from BOA Traditional IRA • Check is payable to MCU fbo Member • Depositing to Traditional IRA here • Transfer or Rollover? • Transfer • Check payable to MCU fbo Member Transfer between “like” IRAs

Member gives you a check from their personal account • They say the funds are from a previous Traditional IRA • Transfer or Rollover? • Rollover • If the Member says it is a rollover, then it is a rollover. Must be within 60 days of the day they received the funds.

Check is from a Roth IRA elsewhere • Made payable to MCU fbo the Member • Deposited to a Roth IRA here • Transfer or Rollover? • Transfer • Check payable to MCU fbo Member Transfer between “like” IRAs

Check is from a Thrift Savings Plan • Check is payable to MCU fbo Member • Deposited into a Traditional IRA • Transfer or Rollover? • Rollover • Funds are from a Qualified Plan, not a Traditional IRA

Member has a check from BOA • Check is made payable to the Member • Member says that it is a Transfer from their Traditional IRA at BOA • Transfer or Rollover? • Rollover • Check is payable to member. IRS regulations say this should be treated as a Rollover.

Member brings in a check payable to MCU fbo their Roth IRA • Wants to deposit into a New Roth IRA with MCU • Transfer or Rollover ? • Transfer • Check is payable to MCU fbo Member transfer between “like” IRAs

Funds are from a 401K • Check is payable to MCU fbo Member • Member wants to deposit to Roth IRA • Rollover or Transfer? • Neither! 401K funds can only be rolled to a Traditional IRA.

Distributions • Taxes • Early Withdrawal Penalty • MIDFLORIDA Penalty • Exceptions to Penalties • RMD’s

Taxation of DistributionsTraditional IRA’s Generally include in income except • Rollovers • Transfers • Re-Characterization • Removal of certain excess contributions • Revocations of regular IRA contributions • Pro rata portion of nondeductible contributions

Information about Federal Withholding and IRS Penalties • Do not confuse the 10% IRS early withdrawal penalty, with our Certificate early withdrawal penalty. • When Federal Withholding is elected, it only applies to Taxes, not Penalties • Withholding must be 10% or more, if elected • IRS penalties are remitted to the IRS when the account holder files their taxes

Federal Withholding Traditional- Total distribution amount is taxable on all withdrawals Roth- Taxes only apply to earnings on non-qualified distributions

IRS 10% Early Withdrawal Penalty Exceptions • Member is 59 ½ or older* • Death* • Permanently disabled* • Substantially equal periodic payments* • Medical Expenses • Health Insurance • First time Homebuyer expenses • Higher Education expenses • IRS levy • Return of non-deductible contributions • Qualified reservists distributions *Recommend acquiring proof of distribution reason

Code 0Direct Transfer • Used when transferring to a like IRA. • Make the check payable to the other institution FBO the member. This Distribution is: • Not Reportable • Not subject to 10%withholding

Code 1Early distribution, no known exception • Member is not 59 ½ • Un-reimbursed medical expenses • Medical Insurance • Higher Education • 1st time home buyer This distribution is: • Taxable • Subject to 10% IRS early withdrawal penalty