Download

1 / 4

40 likes | 53 Views

This chapter explores the significance of an independence framework for auditors, outlines their legal responsibilities, and discusses the various types of common law liability for professional accountants. It also examines a case study to apply and integrate the chapter topics in a practical auditing scenario. Additionally, it highlights the record-setting damages and increased professional liability insurance premiums faced by accountants, emphasizing the potential monetary and criminal penalties for failure to perform services properly. The causes and frequency of lawsuits in auditing are also explored, along with the expectations gap between users and auditors.

E N D

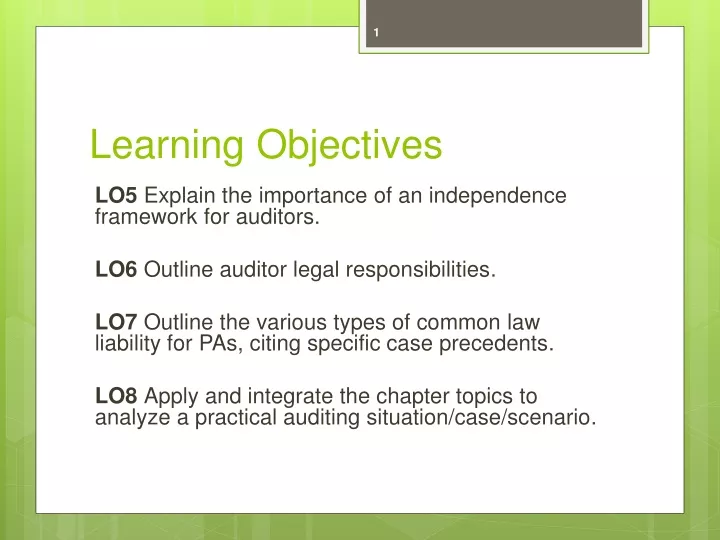

Learning Objectives LO5 Explain the importance of an independence framework for auditors. LO6 Outline auditor legal responsibilities. LO7 Outline the various types of common law liability for PAs, citing specific case precedents. LO8 Apply and integrate the chapter topics to analyze a practical auditing situation/case/scenario.

The Legal Environment Record-setting damages have been awarded and professional liability insurance premiums have increased dramatically. • Accountants are potentially liable for monetary damages and criminal penalties for failure to perform services properly. • Class action suits can result in large damages. • Lawyers take on these suits on a contingency fee basis. LO6

Lawsuit Causes and Frequency Based on a study of 129 cases, legal issues arise from: • 33% - Misinterpretation of accounting principles • 15% - Misinterpretation of auditing standards • 29% - Faulty implementation of auditing procedures • 13% - Client fraud • 7% - Fraud by the auditor LO6

Audit Responsibilities Users of audit reports expect auditors will detect fraud, theft, and illegal acts and report them publicly. • Auditors take responsibility for detecting material misstatements. • An expectation gap exists between the diligence users expect and the diligence auditors are able to accept. • This disparity leads to lawsuits, even when auditors have performed well. LO6