Download

1 / 3

30 likes | 173 Views

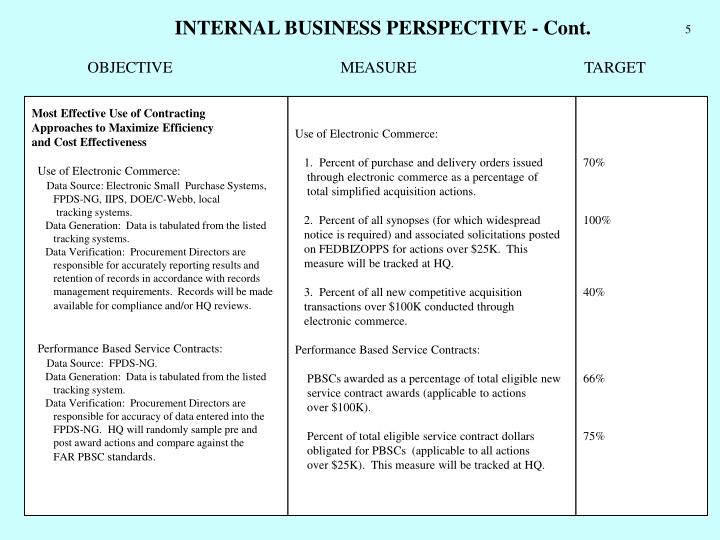

INTERNAL BUSINESS PERSPECTIVE - Cont. 5. OBJECTIVE MEASURE TARGET. Most Effective Use of Contracting Approaches to Maximize Efficiency and Cost Effectiveness Use of Electronic Commerce:

E N D

INTERNAL BUSINESS PERSPECTIVE - Cont. 5 OBJECTIVE MEASURE TARGET Most Effective Use of Contracting Approaches to Maximize Efficiency and Cost Effectiveness Use of Electronic Commerce: Data Source: Electronic Small Purchase Systems, FPDS-NG, IIPS, DOE/C-Webb, local tracking systems. Data Generation: Data is tabulated from the listed tracking systems. Data Verification: Procurement Directors are responsible for accurately reporting results and retention of records in accordance with records management requirements. Records will be made available forcompliance and/or HQ reviews. Performance Based Service Contracts: Data Source: FPDS-NG. Data Generation: Data is tabulated from the listed tracking system. Data Verification: Procurement Directors are responsible for accuracy of data entered into the FPDS-NG. HQ will randomly sample pre and post award actions and compare against the FAR PBSC standards. Use of Electronic Commerce: 1. Percent of purchase and delivery orders issued through electronic commerce as a percentage of total simplified acquisition actions. 2. Percent of all synopses (for which widespread notice is required) and associated solicitations posted on FEDBIZOPPS for actions over $25K. This measure will be tracked at HQ. 3. Percent of all new competitive acquisition transactions over $100K conducted through electronic commerce. Performance Based Service Contracts: PBSCs awarded as a percentage of total eligible new service contract awards (applicable to actions over $100K). Percent of total eligible service contract dollars obligated for PBSCs (applicable to all actions over $25K). This measure will be tracked at HQ. 70% 100% 40% 66% 75%

6 BALANCED SCORECARDPERFORMANCE MEASURES, PERFORMANCE TARGETS AND MANAGEMENT INITIATIVESINTERNAL BUSINESS PERSPECTIVE Procurement

ACTION PLAN/STATUS REPORT FOR BSC INITIATIVE- FY 2005 Balanced Scorecard Initiative:Title of initiative (in italics and bold text) Action Officer: Name of staffer (and office code) with responsibility for completion. Objective of the Initiative: No more than one paragraph that clarifies WHY we are doing this action and the intended RESULTS. Also, if appropriate, provide a description of the scope of the initiative in terms of the work to be done (e.g., will this be a major effort requiring establishment of a large work group? etc.). Approach: Briefly describe the plan, processes, and resources necessary to accomplish the objective. Due Date: List the FY quarter in which completion will occur. Planned Milestones: Identify the major processes, milestones, and list the scheduled start/completion dates. Attach any chart you may have developed that shows work flow/scheduling, etc. Current Status: Current status is to be up-dated by each Action Officer and submitted to the Office Director prior to each of the quarterly reviews of BSC status (Office Directors and Mr. Hopf). This information will be important, particularly if the planned milestones listed above are not on-track, or have not been met. Outcome: When the action is completed, provide a brief statement (one or two sentences) describing the finished product and its benefits. (Note: When the initiative is complete, and the Outcome section is filled-in, send a copy of this Action Plan/Status Report to Yolonda along with a copy of the “completion document” for the initiative (i.e., the report, Acquisition Letter, or other document that evidences completion of the initiative. If there is no “completion document,” then state this in the Outcome section). At the end of the year, this Action Plan/Status Report will then serve as the cover page for the “completion document” that becomes part of the BSC Initiatives Completion Book that Yolonda maintains for Mr. Hopf.) 7