Download

1 / 24

240 likes | 308 Views

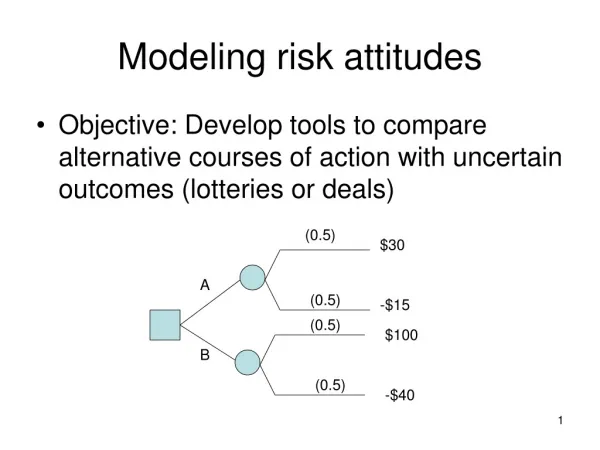

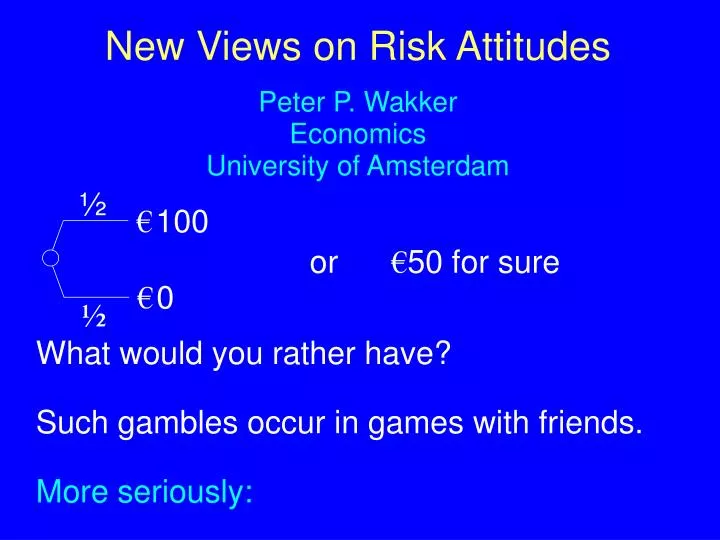

½. € 100. € 0. or € 50 for sure. ½. New Views on Risk Attitudes Peter P. Wakker Economics University of Amsterdam. What would you rather have? Such gambles occur in games with friends. More seriously:. 2. In public lotteries, casinos, and horse races. More seriously:

E N D

½ €100 €0 or €50 for sure ½ New Views on Risk Attitudes Peter P. WakkerEconomicsUniversity of Amsterdam What would you rather have? Such gambles occur in games with friends. More seriously:

2 In public lotteries, casinos, and horse races. More seriously: - Whether you can study medicine in theNetherlands; - In the US in the 1960s, whether youhad to serve in Vietnam (only for men …) Even more seriously: Investments, insurance, medical treatments, etc. etc. This lecture is on the history of risk-theory.

3 Two questions/lines-of-talk: • General modeling of risk attitude. • Is it determined by: • -sensitivity towards outcomes (utility); • -sensitivity towards chance (probability weighting)? • 2) Particular form of risk attitude. • Is risk-aversion • -universally valid (modulo noise); • - systematically violated?

½ €100 €0 ½ p1 x1 . . . . . . xn pn 4 Simplest way to evaluate risky prospects: Expected value ½100 + ½0 = 50 General: p1x1+ ... + pnxn

€50 ½ €100 €0 ½ 5 However, empirical observations: Risk aversion! Falsification of expected value. To explain it, “expected utility.”

p1 x1 . . . . . . xn pn 6 Expected utility is the classical economic risk theory. p1 x1 + ... + pn xn U( ) U( ) Departure from objectivity. U is subjective index of risk attitude. Bernoulli (1738).

p1x1+ ... + pnxn p1 U x1 . . . . . . € xn pn 7 Risk aversion in general: Theorem (Marshall 1890).Risk aversion holds if and only if utility U is concave. U is used as thesubjective index of risk attitude!

8 Line (1) of this talk: the general modeling of risk attitude. Psychologists objected: U=sensitivity towards money ≠risk attitude.

p1 U(x1)+ ... + pn U(xn) w p1 x1 . . . . . . xn pn p 9 Intuition: risk attitude (also) in terms of processing of probabilities. w( ) w() 1 w(p) w(0) = 0, w(1) = 1, w is increasing. 0 p 0 1

utility 10 Lola Lopes (1987): “Risk attitude is more than the psychophysics of money.” Prob. weighting already considered in 1950s (Ward Edwards). Called subjective expected utility (unfortunate term). 'sargument intuitive, not theoretical. economists: Such argumentation is an error! Subj. exp. ut. theory never became “big.”

11 Line (2) of this talk: risk aversion. • Economic arguments for universal risk aversion: • diminishing marginal utility is intuitively plausible; • concave utility needed for existence of equilibria; • no concave U market for lotteries;

12 Marshall, A. (1920)Principles of Economics about risk-seeking individuals: ... since experience shows that they arelikely to engender a restless, feverishcharacter, unsuited for steady work as wellas for the higher and more solid pleasures of life.

U € 13 Problem: Public lotteries!?!? Friedman & Savage (1948):

14 Arrow (1971, p.90) (about lotteries) I will not dwell on this point extensively,emulating rather the preacher, who,expounding a subtle theological point to hiscongregation, frankly stated: Brethren, here there is a great difficulty; let us face it firmly and pass on. Psychologists: ?????

15 Back to line (1), the general modeling of risk attitude. End of seventies: renewed interest in probability weighting, a.o. because of violations of EU. A.o. by Handa (1978, J. of Pol. Econy), Kahneman & Tversky (1979, Econometrica, "prospect theory"). Prominent economic journals ... !

16 To Handa (1978), the JPE received some 10 comments! Of those, Fishburn (1978, JPE) was published. (Among non-published reactions, one by the unknown Australian John Quiggin.) Prospect theory is an exceptionally big succes; theoretically problematic.

17 Probability-weighting violates stochastic dominance! Amazing, that model could survive in the psychological literature for 30 years ...

18 Yet, "risk-attitude through probability weighting" is good intuition. Only, one should weight the "right“ probabilities. Not probability at: a specific outcome, but probability at: at least an outcome.

p1 x1 . . . . . . xn pn 19 Evaluation of lottery with x1… xn 0: w(p1)U(x1) + (w(p2+p1) - w(p1))*U(x2) + ... (w(pj+...+p1) - w(pj-1+...+p1))*U(xj) + ... (w(pn+...+p1) - w(pn-1+...+p1))*U(xn) Idea of Quiggin (1981), Rank-Dependent Utility.

20 Back to line 2, risk aversion. In the beginning, economists' views: Risk-aversion is universal. U concave and prob. weighting wsimilar. Impulses from empirical investigations by psychologists (Tversky and others).

21 Systematic risk-seeking for: Small chances at large gains Large chances at small losses Amazing, that “universal” risk aversion could survive in the economics literature for 30 years …

22 Synthesis: Tversky, A. & D. Kahneman (1992),“Advances in Prospect Theory: Cumulative Representation of Uncertainty," Journal of Risk and Uncertainty 5, 297-323.

23 Cumulative prospect theory: Risk-attitudes in terms of - utilities ánd - probability weighting (- ánd loss aversion). Risk-aversion prevailing,but, systematic deviations. Reference point ("framing"). Theory combines - descriptive force of prospect theory - theoretical force of econ. theories.

24 Summary: 1. Classical econs: Expected utility; Risk at- titude=U(€) (Bernoulli1738, Marshall1890). 2. s: risk attitude also = w(p) (Edwards, 1954). Took wrong p’s. 3. Econs: Take right ("cumulative“) p’s(Quiggin, 1981). Thought universal risk aversion; convex/cave. 4. s: diminishing sensitive iso risk aversion (Tversky & Kahneman, 1992); S-shaped. Synthesis: Cumulative prospect theory