Download

1 / 31

310 likes | 487 Views

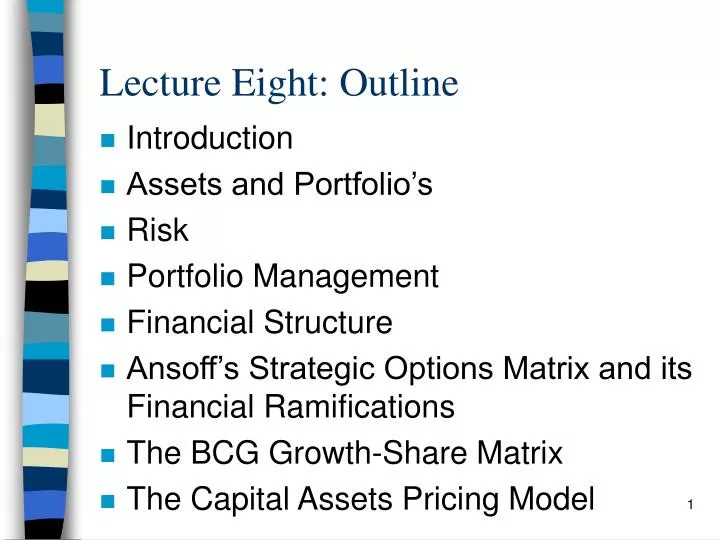

Lecture Eight: Outline. Introduction Assets and Portfolio’s Risk Portfolio Management Financial Structure Ansoff’s Strategic Options Matrix and its Financial Ramifications The BCG Growth-Share Matrix The Capital Assets Pricing Model . Introduction.

E N D

Lecture Eight: Outline • Introduction • Assets and Portfolio’s • Risk • Portfolio Management • Financial Structure • Ansoff’s Strategic Options Matrix and its Financial Ramifications • The BCG Growth-Share Matrix • The Capital Assets Pricing Model

Introduction • Brailsford and Heany (1998) assert that the ultimate goal for an investor is to maximise realised returns for a given level of risk.

Introduction (cont’d) • As Renton (1998) contends, higher levels of risk usually come with higher levels of potential returns, whereas lower levels of risk usually come with lower levels of return. We can apply these financial principles to the value chain.

Assets and Portfolios • Brailsford et al (1998) defines a portfolio as a collection of assets with different risk / return profiles that are pooled together to diversify away risk, while maximising potential returns.

Assets and Portfolios (cont’d) • Elton and Gruber (1987) assert that when two assets have their good and poor returns at opposite times, an investor can always find some combination of these assets that yields the same return under all market conditions

Risk • Farrel (1983) defines risk as the uncertainty that may be associated with earning a return. He continues by asserting that the riskiness of a security will depend on how it blends with the existing securities and contributes to the overall risk of a portfolio.

Risk (cont’d) • Farrel (1983) believes that a number of different sources of risk exist.

Risk (cont’d) • These include: • Interest rate risk • Purchasing power (inflation) risk • Business risk • Financial risk; and, • Systematic risk

Risk (cont’d) • While these types of risk are particularly appropriate to finance-orientated areas of the business, Czinkota and Ronkainen (1998) believe that a number of other types of risk exist.

Risk (cont’d) These include: • Political risk • Technological risk • Social risk • Operating risk; and, • Information risk

Risk (cont’d) • Walters (2002) shows that: “purchasing activities are often required to overcome barriers and these may be practically based or influenced, or be psychological in their nature.

Risk (cont’d) • Assael (1995) suggests manufacturers can overcome that value barrier in two ways.

Risk (cont’d) • The first uses technology to reduce the price.

Risk (cont’d) • The second is to communicate value attributes (to potential consumers) that they have not been made aware of or have not identified for themselves.

Risk (cont’d) • Assael is suggesting the use of process technology to reduce costs and then price but product technology may have the effect of reducing in-use costs.

Portfolio Management • Farrel (1983) believes that portfolio management can be generally described as consisting of three major activities.

Portfolio Management (cont’d) • Asset allocation

Portfolio Management (cont’d) • Weighting shifts across major asset classes; and,

Portfolio Management (cont’d) • Security selection within asset classes

Portfolio Management (cont’d) • With this in mind, the management of a business can gain a great deal from the application of these principles in the running of their organisation.

Financial Structure (cont’d) • The total return of a portfolio is equal to the return of the sum of its parts.

The BCG Growth-Share Matrix • This matrix involves classifying products as ‘stars’, ‘cash cows’, ‘question marks’ or ‘dogs’. Buttery et al (1998) explains the meaning of each classification.

The BCG Growth-Share Matrix (cont’d) • Stars enjoy high growth and high market share. They need considerable amounts of cash to maintain their position. Eventually the growth slows, and they become cash cows.

The BCG Growth-Share Matrix (cont’d) • Cash cows have high market share but low growth. They generate the cash needed to support other business ventures.

The BCG Growth-Share Matrix (cont’d) • Question marks have high growth but low market share. Management faces the alternative of either investing in them in the hope of turning them into stars or divesting them.

The BCG Growth-Share Matrix (cont’d) • Dogs have low growth and low market share. A decision needs to be made whether to maintain the dog for strategic reasons or to divest it.

The Capital Assets Pricing Model The CAPM (Brailsford et al) assumes that investors are risk-averse.The CAPM involves displaying a combination of risk/return alternatives.The Securities Market Line (sml) shows a linear relationship between risk and return, while accounting for market risk and a ‘risk free’ rate of return.The investor can specify the level of risk they are willing to bear - any investments that fall above the SML are performing better than the market, any investment falling below the SML is performing worse than the market.The managers goal is to have all investments on the SML or above it. This doesn’t usually happen.

Discussion Questions • What kinds of risk do value chain managers have to deal with? Out of each of these types of risk, which one do you believe is the most poignant? Why? • Draw a table with the names of each of these models in the left hand column, and outline the advantages and disadvantages of each model in your opinion.

Discussion Questions (cont’d) • Using three of the above models, how can value chain managers design and develop an inter-organisational value strategy?