Download

1 / 25

250 likes | 265 Views

Explore the dynamics of the global economic environment for emerging market economies, focusing on issues of overheating, commodity price volatility, and the natural resource curse. Discover expert insights from the Jeffrey Frankel Annual Symposium on Capital Markets in Medellin, Colombia, and delve into strategies for sustainable growth and avoiding potential pitfalls. Learn about the Dutch Disease, macro policies of major emerging markets, and recommendations for managing commodity wealth ethically and effectively.

E N D

The Global Economic Environment for Emerging Market EconomiesAPPENDICESJeffrey Frankel Annual Symposium on Capital Markets Medellin, Colombia, May 3, 2012

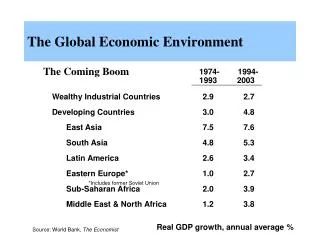

Appendix 1: Overheating in Emerging Markets • By 2011, two years of strong growth had returned some EM economies to a state of probable overheating. • The Question for 2012: • Is the current easing of growth a soft landing? • Or will it turn to a hard landing?

Credit growth has again been high in Turkey and some other EMs (incl. Colombia) World Economic Outlook, IMF, April 2012

Output in EMs is now above potential(excl. Eastern Europe).AdvancedEconomies are still far below potential output. World Economic Outlook, IMF, April 2012

Inflation in many EMs rose in 2010-11, but appears to be easing in 2012. World Economic Outlook, IMF, April 2012

Appendix 2: Dealing with Commodity Price Volatility • The Natural Resource Curse • The Dutch Disease

Many countries that are rich endowed with oil, minerals or fertile land have failed to grow more rapidly than those without. • Examples: • Oil producers in Africa & the Middle East have relatively little to show for their resources. • Meanwhile, East Asian economies achieved western-level standards of living despite being rocky islands (or peninsulas) with virtually no exportable natural resources. • Japan, Singapore, Hong Kong Korea & Taiwan, • followed by China.

Some developing countries have avoided the pitfalls of commodity wealth. E.g., Chile (copper) Botswana (diamonds) Some of their features are worth emulating. The last section of my survey paper explores policies & institutional innovations that might help avoid the natural resource curse and achieve natural resource blessings instead. 9

Are natural resources necessarily bad? Commodity wealth neednot necessarily lead to inferior economic or political development. Rather, it is a double-edged sword, with both benefits and dangers. It can be used for ill as easily as for good. The priority for any country should be on identifying ways to sidestep the pitfalls that have afflicted other mineral producers in the past, to find the path of success. No, of course not. 11

One channel of the NRC: Dutch Disease 5 side-effects of a commodity boom 1) A real appreciation in the currency 2) A rise in government spending 3) A rise in nontraded goods prices 4) A resultant shift of resources out of non-export-commodity traded goods 5) Sometimes a current account deficit. 12

The Dutch Disease: The 5 effects elaborated 1) A real appreciation in the currency taking the form of nominal currency appreciation if the exchange rate floats e.g., floating-rate oil exporters, Kazakhstan, Mexico, & Russia. or the form of money inflows & inflation if the exchange rate is fixed ; e.g. fixed-rate oil-exporters, UAE & Saudi Arabia. 2) A rise in government spending in response to increased availability of tax receipts or royalties. 13

The Dutch Disease: 5 side-effects of a commodity boom 3) An increase in nontraded goods prices (goods & services such as housing that are not internationally traded), relative to internationally traded goods,esp. manufactures. 4) A resultant shift of resources out of non-export-commodity traded goods pulled by the more attractive returns in the export commodity and in non-traded goods. 5) A current account deficit thereby incurring international debt that is hard to service when the boom ends. E.g. the end of the 1970s commodity boom. 14

Appendix 3 More graphs from IMF WEO, April2012. • Recent macro policies of major EM countries. • More on commodity prices.

Some EMs, such as Chile & China, ran budget surpluses before 2008, allowing fiscal easein response to the global recession World Economic Outlook, IMF, April 2012

Interest rates have come down since 2008 World Economic Outlook, IMF, April 2012

EMs continue to build up reserves,except that China, the biggest reserve holder of all, has recently stopped. World Economic Outlook, IMF, April 2012

Global imbalances have narrowedespecially China’s surplus World Economic Outlook, IMF, April 2012

Flight from risk dented EM capital flows,first due to the GFC, and then the euro crisis World Economic Outlook, IMF, April 2012

Oil & agric. prices rose sharply in 2011 World Economic Outlook, IMF, April 2012

When inventories are unusually low,the commodity price is unusually high World Economic Outlook, IMF, April 2012

7. Manage Commodity Funds transparently & professionally, like Botswana’s Pula Fund -- not subject to politics like Norway’s Pension Fund. 8. Invest in education, health, & roads. 9. Buyers: Publish What You Pay. Good governance institutions Recommendations for commodity producers,concluded