Download

1 / 17

190 likes | 566 Views

Understanding a payslip. Starter question. You are a supermarket team leader earning an annual salary of £15,000. How much do you take home each month? More than £1,250? Exactly £1,250? Less than £1,250?. National insurance (N.I.). What is this?. National Insurance.

E N D

Understanding a payslip Payslip Money Works: Level 2 Topic 4

Starter question • You are a supermarket team leader earning an annual salary of £15,000. • How much do you take home each month? • More than £1,250? • Exactly £1,250? • Less than £1,250? Payslip Money Works: Level 2 Topic 4

National insurance (N.I.) What is this? Payslip Money Works: Level 2 Topic 4

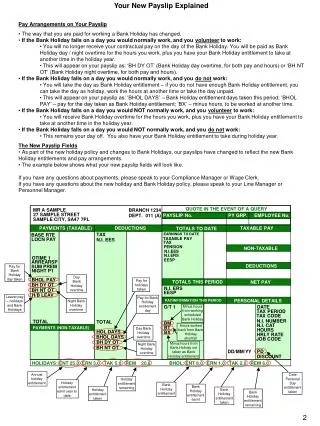

National Insurance • Everyone receives their National Insurance number just before their 16th birthday. It will stay with you for life. • Most people who work have to pay National Insurance Contributions, unless they are one of the groups who are exempt from the system. • National Insurance is paid at 11%* of your salary. • By paying National Insurance you are paying for benefits (including the jobseekers allowance, Incapacity benefit, a Widows Pension, and Maternity allowance) and the state retirement pension. Payslip Money Works: Level 2 Topic 4

Tax code What is this? Payslip Money Works: Level 2 Topic 4

Tax Code • Your Tax Code will show how much income you are allowed to earn before you start to pay tax. • It is the first 3 numbers of your tax allowance followed by a letter. Most people have the letter ‘L’ which indicates that they have the basic tax allowance. • So 647L means this person can earn £6,470* before they start to pay tax. Payslip Money Works: Level 2 Topic 4

bacs What is this? Payslip Money Works: Level 2 Topic 4

Bacs • BACS is the Bankers Automated Clearing System. • If you are paid by BACS it means your pay goes straight into your own bank account. • It means you do not have to carry large sums of money around on pay day. Payslip Money Works: Level 2 Topic 4

deductions What is this? Payslip Money Works: Level 2 Topic 4

Deductions • Both National Insurance and Tax are deducted from your pay. These are called compulsory deductions because you must pay them. • The tax that is taken off is called income tax. • Everyone is allowed to earn some money before they start to pay income tax; this is your tax allowance. For most people it is £6,470* per year (per annum). • Once your income goes above this allowance you will have approximately 20 pence of every pound you earn taken as income tax. • So when income tax is added to National Insurance you can expect to lose 30% of your income in deductions. Payslip Money Works: Level 2 Topic 4

Gross pay What is this? Payslip Money Works: Level 2 Topic 4

Gross Pay • The total income that you receive before any deductions are made is called your Gross Pay. • Gross pay will be bigger than Net Pay. Payslip Money Works: Level 2 Topic 4

Net pay What is this? Payslip Money Works: Level 2 Topic 4

Net Pay • This is the pay you have left after your deductions have been removed. • It is sometimes called your ‘take home’ pay. • All the deductions are made by the Tax offices, so you don’t have to do anything about it, except be honest about how much income you earn. • This system is called Pay As You Earn (PAYE). Payslip Money Works: Level 2 Topic 4

totals What is this? Payslip Money Works: Level 2 Topic 4

Total Deductions This sums up all the deductions from your pay so far in the tax year (April to March). If you were to leave the business who paid you, then you should receive a P45. This would contain: • Your leaving date • How much tax you have paid so far in this tax year • How much pay you had earned so far in this tax year. The tax year runs from April to March. So this payslip for August is month 5. At the end of the tax year your employer should give you a P60 which will tell you: • The total amount of tax you have paid in this tax year • The total amount of pay you have earned in this tax year. Payslip Money Works: Level 2 Topic 4

Total Deductions Some people will choose to have other payments deducted from their pay; these are called voluntary deductions. E.g. Most people contribute to a pension scheme (a different one to the state pension that you qualify for by paying National Insurance payments). These contributions are taken from your gross pay and invested to build up a pension fund for you. When you retire, this fund will be used to provide you with a retirement income (known as pension or annuity). Another type of voluntary deduction is when you choose to join a Trade Union and pay their fees every month from your payslip. Payslip Money Works: Level 2 Topic 4