Download

1 / 15

150 likes | 275 Views

MYPD2. SACCI VIEWS AND RECOMMENDATIONS TO NERSA 21 January 2010 Peggy Drodskie Executive Advisor to the CEO. OVERVIEW. Introduction Fundamentals of Generation Macro-economic Impact – Inflation, GDP and Employment National Energy Policy Other Challenges Solutions Interim Actions

E N D

MYPD2 SACCI VIEWS AND RECOMMENDATIONS TO NERSA 21 January 2010 Peggy Drodskie Executive Advisor to the CEO

OVERVIEW • Introduction • Fundamentals of Generation • Macro-economic Impact – Inflation, GDP and Employment • National Energy Policy • Other Challenges • Solutions • Interim Actions • Stakeholder Summit

INTRODUCTION • SACCI constituents: • Chambers across South Africa • Uni-sectoral Associations • Corporates • Three pronged approach. • NERSA Issues Paper • Membership survey.

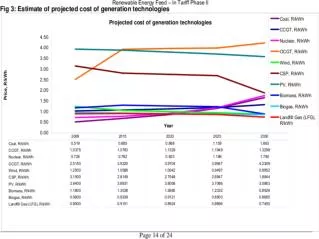

Fundamentals of Generation • Availability and cost of water and coal. • Environmental cost. • True cost comparisons of alternative energy sources. • Political cooperation in the region, particularly SADC.

MACRO-ECONOMIC IMPACT • Tariff increases since 2005 – 91% • Weighting in CPI – 1,87% • Assumptions: • Municipalities pass on full increase. • Reserve Bank does not increase interest rates too drastically.

IMPACT ON INFLATION • Inflation: Producers and retailers increase prices. • Inflation increase of about 0,3% - above 3% - 6% SARB target. • Reduced personal disposable income and household consumption spending. • Increased interest rates. • Lower employment.

IMPACT ON GDP • Assume about 15% of output is electricity intensive. • Some reduction in viability. • Reduced competitiveness. • Lower capital formation. • Will ease over time. • Loss to GDP over period: R200billion

IMPACT ON EMPLOYMENT Lower GDP results in • Failing companies and thus • Lower employment levels. • Approximately 500 000 job losses (In addition to 1 000 000 in 2009.)

NATIONAL ENERGY POLICY Prepare Eskom for competition: • Restructure Eskom into 2 companies – generation and transmission. • Place power stations into a number of companies to facilitate the introduction of competition. • Place power stations in private hands. • Not implemented.

OTHER CHALLENGES • South Africa’s competitive advantage lost. • Profit from current tariffs must not be applied to capex. • Appears to be little hope of increased borrowing. • Raising tariffs runs counter to poverty alleviation and job creation strategies.

SOLUTIONS • Return to National Energy Policy • Eskom to control transmission. • Generation to be open to private participation – PPPs, BOT schemes, IPPs. • Rationalise distribution industry. • Promulgate any necessary legislation and regulations.

SOLUTIONS Cont. • Introduce a charter based on recommendations in White Paper on Energy Policy. • Reintroduce Electricity Policy Council. • Ring fence tax revenue - low interest loan to Eskom. • Treasury to be responsible DSM. • New generation introduced at 80c/kWh

PROPOSALS FOR IMMEDIATE FUTURE (2010/2011) • Grant inflation related tariff increase for 2010/11. • Work through possibilities with all stakeholders in 2010. • Address local authority increases. • Postpone introduction of 2c/kWh environmental levy • Eliminate import duties on energy efficient consumables and equipment. • New generation introduced at 80c/kWh

STAKEHOLDER SUMMIT • All stakeholders. • Determine a way forward – medium and long term. • Ongoing process. • 02 February • All invited.