Download

1 / 72

720 likes | 737 Views

Explore the potential implications, market dynamics, and long-term sustainability of natural gas supplies through 2025. Discover actions to boost productivity and efficiency in North American gas markets for reliable energy supplies.

E N D

National Petroleum Council Natural Gas Study Federal Energy Regulatory Commission Natural Gas Markets Conference Balancing Natural Gas Policy: Fueling the Demands of a Growing Economy October 14, 2003

National Petroleum Council • Federally chartered, privately funded advisory committee • Sole purpose is to advise and make recommendations to the Secretary of Energy • Operates under the Federal Advisory Committee Act • Council comprised of ~175 members

“Examine the potential implications of new supplies, new technologies, new perceptions of risk, and other evolving market conditions that may affect the potential for natural gas demand, supplies, and delivery through 2025 ... provide insights on energy market dynamics, including price volatility and future fuel choice, and an outlook on the longer-term sustainability of natural gas supplies … advice on actions that can be taken by industry and Government to increase the productivity and efficiency of North American natural gas markets and to ensure adequate and reliable supplies of energy for consumers.” Spencer Abraham Secretary of Energy March 2002 The Study Could Not Be More Timely

Committee on Natural Gas Coordinating Subcommittee Supply Transmission & Distribution Demand Study Organization

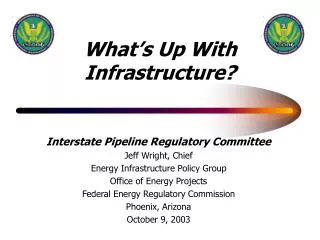

U.S. & CANADA TOTAL DEMAND CANADA SUPPLY U.S. SUPPLY $8 $6 GAS PRICE, $/MMBTU $4 $2 $0 Higher Prices Reflect a FundamentalShift in Supply & Demand 30 25 20 TCF 15 10 5 0 1985 1990 1995 2000

We Must Improve from the Status Quo The current policy direction — unaltered — will likely lead to difficult conditions in the natural gas market, but industries, government, and consumers will react. Therefore, this study assumes action beyond the status quo: Arctic pipelines built, substantial LNG imports, success in Lower-48 permitting, increased energy efficiency, fully-compliant coal and renewable generation.

Reactive Path Balanced Future The NPC Analyzed Two BaseScenarios Beyond the Status Quo Public policies remain in conflict, encouraging consumption while inhibiting supply … resulting in higher prices and volatility Public policies aligned: alternate fuels and new natural gas supply sources compete to ensure lowest consumer cost

Reactive Path Reactive Path Balanced Future Balanced Future Potential Price Range Annual Average Henry Hub Prices, $/MMBTU ($2002) $8.00 $7.00 $6.00 $5.00 $4.00 $3.00 $2.00 $1.00 $0.00 1995 2000 2005 2010 2015 2020 2025 2000 2005 2010 2015 2020 2025

The NPC Recommends Action in All These Areas Improve demand flexibility & efficiency Increase supply diversity Sustain and enhance infrastructure Promote efficient markets and Higher economic growth Higher employment Stronger industrial activity and and

Supply Task Group Approach • Conduct a comprehensive review of the North American resource base • Analyze historical production performance • Evaluate new supply sources (LNG, Arctic) • Consider effects of advancing technology and regulatory environment • Focus on production outlook

Supply Task Group Participants Subgroups LNG Shell John Hritcko BP ChevronTexaco ConocoPhillips DOE/FERC El Paso ExxonMobil KeySpan Sempra LNG Shell US GP Technology* ChevronTexaco Bob Howard Baker-Hughes BP/Shell - Workshop ChevronTexaco ConocoPhillips DOE El Paso ExxonMobil Gas Tech Institute Halliburton Landmark Marathon Arctic P/L ExxonMobil Robbie Schilhab BP Ken Konrad ConocoPhillips Joe Marushack Anadarko ChevronTexaco Imperial Task Group Leaders ExxonMobil Mark Sikkel Bill Strawbridge DOE Elena Melchert Members Alcorn Anadarko BP Burlington ChevronTexaco ConocoPhillips DOE El Paso ENSCO Marathon Ocean Energy Shell Resource* ExxonMobil Gerry Worthington Gary Stone Anadarko Bob Stancil Anadarko BP ChevronTexaco ConocoPhillips Devon El Paso EnCana ExxonMobil Kerr-McGee Marathon Nabors Parker Shell USGS/MMS/CGPC Envir/Reg/Access Burlington David Blackmon ARI BLM Burlington ChevronTexaco ConocoPhillips DOE ExxonMobil Forest Service Marathon MMS Shell *Additional participants from regional workshops

Supply History and Outlook Reactive Path Case

“Traditional North American producing areas will provide 75% of long-term U.S. gas needs, but will be unable to meet projected demand.” “Increased access to U.S. resources (excluding designated wilderness areas and national parks) could save consumers $300 billion in natural gas costs over the next 20 years.” “New, large-scale resources such as LNG and Arctic gas are available and could meet 20%-25% of demand, but are higher-cost, have longer lead times, and face major barriers to development.” Supply Findings

Supply Recommendations Increase access and reduce permitting impediments to development of Lower - 48 natural gas resources. Enact enabling legislation in 2003 for an Alaska gas pipeline Process LNG project permit applications within one year

Supply Development Roadmap • Resource Base • Historical Production Performance • Cost Estimates • Technology Commercial Resource and Production Outlook - Access - Arctic Gas - LNG

Resource Assessment Methodology • Objective to determine commercial resource through 2025 • Assessed components - Proved, Growth and New Fields • Assessed costs of finding, developing and operating • Developed commercial resource estimates by modeling supply/demand balance • Proved Reserves • Verified EIA reported data with decline curve analysis • Growth of Proved - (existing fields) • Extrapolation of historical recovery/well trends • New Fields (Undiscovered) • Based on statistical field size distribution and chance of success, by basin • Conventional and Nonconventional (tight gas, CBM, shale gas) • Study based on publicly available data (government & commercial) • Resource assessments from USGS, MMS, CGPC for Canada, and IHS for Mexico • Historical cost, production, field data from API, IHS, EEA, Nehring, etc • Industry workshops used to validate or adjust publicly available data

Resource Assessment * Total Technical Resource = 1969 TCF Undiscovered Technical Resource = 1366 TCF 300 Nonconventional Conventional 250 200 TCF 150 100 50 0 Alaska WCSB Mexico Rockies Gulf Coast Arctic Canada Gulf of Mexico Eastern Interior Eastern Canada * Current Technology

North America 3000 Lower - 48 Alaska Canada Mexico 2500 2000 1500 1000 500 0 1992 NPC 1999 NPC 2003 NPC Technical Resource Base Mean Assessment - 1999 Base, Advanced Technology (TCF) Lower - 48 • Lower - 48 technical resource of 1250 TCF is 210 TCF (14%) lower than 1999 Study • Reduced assessment for growth to proved reserves half of difference • Probabilistic uncertainty range - P10 = 135% Mean, P90 = 70% Mean

Production Performance Methodology • Analyzed the production performance of all gas wells drilled since 1990 • Quantified average well performance parameters for each producing basin • Expected recovery • Initial production rate • Decline rate • Evaluated rate of base production decline from existing wells • Analyzed the production response to increased drilling activity • Results used to establish future well performance expectations

Recovery per Gas Connection Rockies Coal Bed Methane 2.0 MMcf/d 1.8 1.0 1.6 EUR = 5 BCF Lower - 48 0.8 1.4 (Excluding Nonconventional and DW GOM) 0.6 1.2 Production Rate BCF per Gas Connection 1.0 0.4 Western Canada 1.4 BCF 0.8 0.2 1.0 BCF 0.6 0.5 BCF 0.4 0.0 0 12 24 36 48 60 72 84 0.2 Months 90-95 96-98 1999 2000 0.0 1990 1992 1994 1996 1998 2000 Production Performance - Recovery per Well Source: Base data from EEA GSR

Trends by Vintage - Initial Rate, Decline Rate, and EUR Trends by Vintage - Initial Rate, Decline Rate, and EUR Production Performance - Basin Trends Western Canada Sedimentary Basin Anadarko Basin

Lower - 48Wet Gas Production from Gas Wells, BCFD by Year of Production Start 60 50 40 30 20 10 0 1992 1994 1996 1998 2000 2002 Production Performance - Decline Trends Source: Base data from IHS

Monthly L-48 Dry Gas Production Production Performance Review – 2001 Drilling Response • Analysis of incremental drilling 2001 vs. 1999 • Average first year recovery declined 10-25% • - Decline greater for incremental wells • Calculated incremental production of 2.9 BCFD • - Compares to observed ~2.4 BCFD • - 1999 drilling program yielded ~ 6 BCFD Source: EEA GSR and Baker Hughes Incremental drilling: 2001 vs. 1999 What each well made: Buildup: Total 2.9 BCFD

Cost Methodology • Methodology • Public and commercial databases used • Drilling and Completion • Lower 48 - API Joint Association Survey • GOM - MMS data • Canada - Petroleum Services Assoc. Canada • Facilities • Lower 48 - EIA Equipment and Operating costs • GOM - Wood Mackenzie • Canada - EEA database • Costs benchmarked to industry experience • Results • Overall drilling costs compare well to 1999 study • GOM costs higher for deeper reservoirs • Lower rig attrition assumed than 1999 study

Current NPC Study Water Depth Pleistocene / Miocene Texas Foldbelt Foldbelt Pliocene Deep ( Perdido) (Miss. Fan) Shelf 0 – 40 m 9000’ 11,500’ 25,000’ 40 – 200 m 9000’ 11,500’ 25,000’ 200 – 400 m 11,500’ 14,500’ 400 – 800 m 11,500’ 14,500’ 17,000’ 800 – 1600 m 11,500’ 14,500’/20,000’ 11,000’ 17,000’ > 1600 m 11,500’ 14,500’/20,000’ 11,000’ 17,000’ 5 1, 2 4 1, 2 3 3 1999 NPC STUDY Central/Western (1-4) Conventional Subsalt Water Depth 0 – 40 m 11,000’ 40 – 200 m 11,000’ 13,000’ 200 – 1000 m 13,500’ 15,500’ 1000 – 1500 m 13,250’ 1500 - 3000 m 15,000’ Gulf of Mexico Drilling Cost Development (4) (3) (3) (1) (2) 1000 – 3000 m 15,250’

1999 Study 2003 Study Deepwater GOM Development South Texas Gas Well Costs Cost Comparison 5.0 5 4.0 4 3.0 3 Well Cost, 2000$MM Total Development Cost, $MM 2.0 2 1.0 1 1999 Study 2003 Miocene Deep 0.0 0 0 - 5 5 - 10 10 - 15 >15 0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 Drilling Depth, Thousand Feet Reserves, MMBOE Cost Results

Coal Bed Methane Drilling Completion Subsurface Imaging Deepwater Infrastructure Natural Gas Hydrates Technology Improvement Process • Technology Subgroup determined impact new technologies will have on supply • Six workshops held with industry experts to gather insights on technology advancements and estimated impact • Technology improvement parameters developed for model input • Gas production 14% higher in 2025 as result of technology enhancements • Sensitivity cases analyzed to determine range of technology advancement

Technology Area % Annual Improvement % Overall Improvement % Annual Improvement % Overall Improvement % Annual Improvement % Overall Improvement Exploration Success 0.53% 14% 0.87% 24% 0.08% 2% Development Success 0.46% 11% 0.87% 24% 0.13% 3% Recovery per Well 0.87% 24% 1.49% 45% 0.23% 6% Drilling Cost -1.81% -37% -1.60% -33% -1.02% -23% Completion Cost -1.37% -29% 0.83% 23% -.034% -8% Initial Production 0.74% 20% 1.13% 32% 0.24% 6% Infrastructure Cost -1.18% -26% -1.73% -35% -0.63% -15% Operating Expense -1.00% -22% -1.52% -32% -0..44% -10% Technology Improvement Parameters Reactive Path High Advancement Low Advancement These numbers represent the average of the parameters

Modeling Methodology • Key inputs to model, by region and reservoir depth • Technical resource and field size distribution • Production performance parameters • Drilling, development, and operating costs • Technology improvement parameters • Model calculates costs to develop new supplies for each region • Model develops “lowest cost” supplies until demand is met • Model determines supply/demand equilibrium and resulting price • Price is established by cost of last increment of supply • Arctic gas and LNG imports were “fixed” model inputs • Model determines commercial resource available for development

Lower - 48 Resource Base - (TCF) Technical Commercial Commercial Resource • Commercial resource determined from • econometric modeling • 760 TCF commercial at $4.00/mmbtu, • 60% of technical resource • Supply curves developed for resource • type and region

Lower - 48 Supply Curve - Resource Type Lower - 48 Supply Curve - Regions 100% 100% 80% 80% 60% 60% % Unproven Reserves % Unproven Reserves Rockies GOM 40% 40% Eastern Interior Total Gas Gulf Coast Midcontinent 20% 20% Growth New Fields Nonconventional Total Gas 0% 0% $2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 $2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 Supply Curves

Gas Production by Resource Type Gas Production by Region 30 30 25 25 Canada - West Nonconventional Canada - East 20 20 Eastern Interior Rockies 15 TCF/Year 15 TCF/Year GOM - Slope Conventional 10 10 GOM - Shelf Gulf Coast Onshore 5 5 Mid Cont / Permian Other Associated 0 0 2000 2005 2010 2015 2020 2025 2000 2005 2010 2015 2020 2025 Production Outlook, Lower-48 and Non-Arctic Canada Reactive Path Case • Mature regions declining • Production growth from new offshore areas • and nonconventional regions • Conventional production declining • Nonconventional increase maintains • overall production level

Supply at Constant Price - $/MMBTU ($2002) Production by Resource Category 30 30 25 25 Undiscovered Future Nonconventional 20 20 Drilling Required Undiscovered 15 15 Tcf/Year Conventional TCF/Year 10 10 $5 Fixed Price Growth $4 Fixed Price Proved 5 5 $3 Fixed Price 0 0 2000 2005 2010 2015 2020 2025 2000 2005 2010 2015 2020 2025 Production Outlook, Lower-48 and Non-Arctic Canada Reactive Path Case • Proved reserves from existing wells declining • at 25-30% per year • New wells required to develop non-proved • resource • All segments critical to outlook • Production declines in $3 price environment • Maintaining production levels requires $5+ • outlook for Reactive Path case

North America Exploration and Gas Well Activity Level Production CAPEX 25,000 80 20,000 US L48 70 60 15,000 Canada Gas Wells 50 Canada 10,000 40 $ Billions (2002$) 30 5,000 United States 20 10 0 0 1990 1995 2000 2005 2010 2015 2020 2025 1990 1995 2000 2005 2010 2015 2020 2025 Drilling and Capital Outlook Reactive Path Case

Lower - 48 Production Outlooks NPC 2003 and EIA 2003 Comparison - Onshore Recovery Activity Resource 25 500 1.80 14,000 450 1.60 12,000 20 400 1.40 10,000 350 1.20 300 15 8,000 1.00 TCF/yr BCF / Well TCF Wells / Yr. 250 0.80 6,000 200 10 0.60 NPC 1999 ($2.50 - $3.50) 150 4,000 0.40 EIA 2003 Energy Outlook ($3.00 - $3.50) 100 2,000 5 0.20 50 NPC 2003 - Reactive Path ($5.00 - $7.00) 0.00 0 0 Conv. Non - conv. Conv. Non - conv. EIA 2003 EIA 2003 Conv. Non - conv. EIA 2003 0 NPC 2003 NPC 2003 NPC 2003 2000 2005 2010 2015 2020 2025 Lower - 48 Production Comparison Reactive Path Case • NPC 2003 vs EIA 2003 • Offshore outlooks similar • EIA higher onshore outlook • Higher resource • Higher non-conventional recovery • Different activity mix • NPC 2003 vs NPC 1999 • Outlook lower for all regions except Rockies; • especially GOM • Technical resource • Production performance parameters • Technology improvement factors

Access Evaluation • Objectives • Clearly articulate complexity of the regulatory/environmental issues • Quantify the impact on access to and recovery of natural gas resources • Recommend actions supportive of environmentally sound development activities • Approach • Expand on 1999 NPC study work; assess “conditions of approval” • - Compile habitat maps for major basins • - Estimate cost and timing impacts of regulatory process; quantify statistically • Recommend specific improvements

Quantification Process Quantify requirements if Raptor Habitat species / actions are present; cost, time Conduct analysis to determine Within study delays, and probability Calculate cost and time delays for 1000 potential wells. boundaries, of percent of map the areas · surveys study area. having species · mitigation or actions of · studies, EA, EIS interest · no surface access Develop curves for cost and for delay. Quantify requirements if Winter Range species / actions are species / actions are $k present; cost, time present; cost, time Calculate delays, and probability delays, and probability percent of of of study area. · · surveys surveys · · mitigation mitigation · · studies, EA, EIS studies, EIS · · no surface access no surface access Well 1 2 3 4 5 6 … 1000 T & E Species Quantify requirements if Quantify requirements if species / actions are species / actions are Calculate present; cost, time present; cost, time percent of delays, and probability delays, and probability study area. of of · · surveys surveys · · mitigation mitigation Determine access inputs to model. · · studies, EA, EIS studies, EIS · · · no surface access per well range of costs and average no surface access · per well range of delays and average · legislative/administrative withdrawn area · effective area inaccessible due to regulation Etc. ( Approx 60 maps) Access Evaluation Process

Green River Basin - Big Game Crucial Ranges Wyoming Basin Outline Green River, Wyoming Colorado Utah

Green River Basin - Grizzly Bear, Canadian Lynx, Grey Wolf Grizzly Bear Gray Wolf Canadian Lynx Wyoming Basin Outline Green River, Wyoming Colorado Utah